TL;DR:

- Finnish accounting laws require strict compliance with national and EU standards for all businesses.

- Smaller businesses mostly use FAS, while IFRS applies to listed companies and large entities.

- Outsourcing accounting enhances compliance, accuracy, and management focus on business growth.

Finnish accounting involves far more than filing tax returns once a year. Finnish accounting law is governed by strict legislation, national standards, and EU regulations that apply to every business, regardless of size. For small and medium-sized business owners, getting this wrong carries real consequences: regulatory penalties, missed deadlines, and damaged creditor relationships. This guide covers the key regulations, financial reporting obligations, accounting standards, VAT and tax compliance, audit requirements, and the practical benefits of outsourcing. Whether you run a sole trader operation or a growing limited company, understanding these rules is essential for long-term stability.

Table of Contents

- Finnish accounting regulations and standards

- Preparing financial statements and reporting obligations

- Accounting standards: Finnish (FAS) vs international (IFRS)

- Tax compliance, VAT, and audit requirements in Finland

- Outsourcing accounting and practical improvements for SMEs

- Why accounting in Finland demands more than bookkeeping: vital lessons for SMEs

- Expert Finnish accounting support: a smart next step

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Understand Finnish standards | Accounting in Finland relies on strict legal regulations and standards, especially FAS for SMEs. |

| Comply with reporting deadlines | Produce and file financial statements within four months of financial year end to meet legal requirements. |

| VAT and audits matter | SMEs must register for VAT if turnover exceeds €20,000; audit requirements are mandatory unless exempt. |

| Outsourcing boosts quality | Using expert accounting services can enhance financial reporting and reduce compliance risk. |

| Treat accounting strategically | Strategic, proactive accounting delivers business growth and protects against costly errors. |

Finnish accounting regulations and standards

Every business operating in Finland must maintain proper accounts. This is not optional. Responsibility for compliance rests firmly with management, and ignorance of the rules is not a valid defence. Finnish accounting is governed by the Finnish Accounting Act (No. 1620/2015), Finnish Accounting Standards (FAS), and EU regulations. Together, these form the legal backbone that every business must work within.

The Accounting Act sets out the minimum requirements for record-keeping, financial reporting, and the retention of documents. FAS provides the detailed technical standards that guide how transactions are recorded and reported. EU regulations add another layer, particularly for businesses with cross-border activities or those operating in regulated industries. If you want a practical starting point, our SME bookkeeping guide walks through the core obligations in plain language.

The rules do vary depending on your business size and structure. Micro-businesses face lighter requirements than medium-sized companies, and listed entities face the most demanding standards of all. Here are the core compliance obligations every Finnish SME should be aware of:

- Maintain a double-entry bookkeeping system

- Record all transactions promptly and accurately

- Prepare annual financial statements

- Retain accounting records for at least six years

- File tax returns and VAT reports on time

- Ensure the chart of accounts aligns with FAS requirements

The table below summarises how requirements differ by business size:

| Business type | Double-entry bookkeeping | Financial statements | Audit required | Public disclosure |

|---|---|---|---|---|

| Sole trader (micro) | Simplified allowed | Optional in some cases | Usually exempt | No |

| Small limited company | Required | Required | Conditional | Yes |

| Medium-sized company | Required | Required | Required | Yes |

| Listed entity | Required | Required (IFRS) | Required | Yes |

Understanding which category applies to your business is the first step. If you are unsure about which accounting methods apply to your situation, it is worth reviewing the options carefully before your next financial year begins.

Preparing financial statements and reporting obligations

Once you understand the legal framework, the next practical challenge is producing accurate financial statements on time. Finnish law requires that financial statements include a profit and loss account, a balance sheet, and explanatory notes. These documents must be submitted within four months of the financial year end and made publicly available through the Trade Register.

Not every business faces the same level of obligation. The mandatory disclosure rules apply when at least two of the following thresholds are exceeded: balance sheet total over €350,000, annual turnover over €700,000, or an average of more than ten employees. Smaller businesses below these thresholds have lighter obligations, but they are still required to maintain proper records.

Here is a straightforward process for producing compliant financial statements:

- Reconcile all bank accounts and ledgers at year end

- Review accounts receivable and payable for accuracy

- Calculate depreciation on fixed assets

- Prepare the profit and loss account

- Compile the balance sheet with all assets and liabilities

- Write the notes to the accounts, covering accounting policies and material items

- Submit to the Trade Register within the four-month deadline

Good [bookkeeping practices](https://blog.finovate.fi/blog/bookkeeping-best practices finnish small businesses) throughout the year make this process significantly easier. Businesses that update their records monthly rather than scrambling at year end consistently produce more accurate statements.

Pro Tip: Start preparing your financial statements at least six weeks before the deadline. This gives you time to identify errors, gather missing documents, and avoid the costly mistakes that come from rushing.

If you want to reduce the time spent on year-end preparation, consider reviewing your bookkeeping workflow now. Small improvements made during the year pay dividends when reporting season arrives.

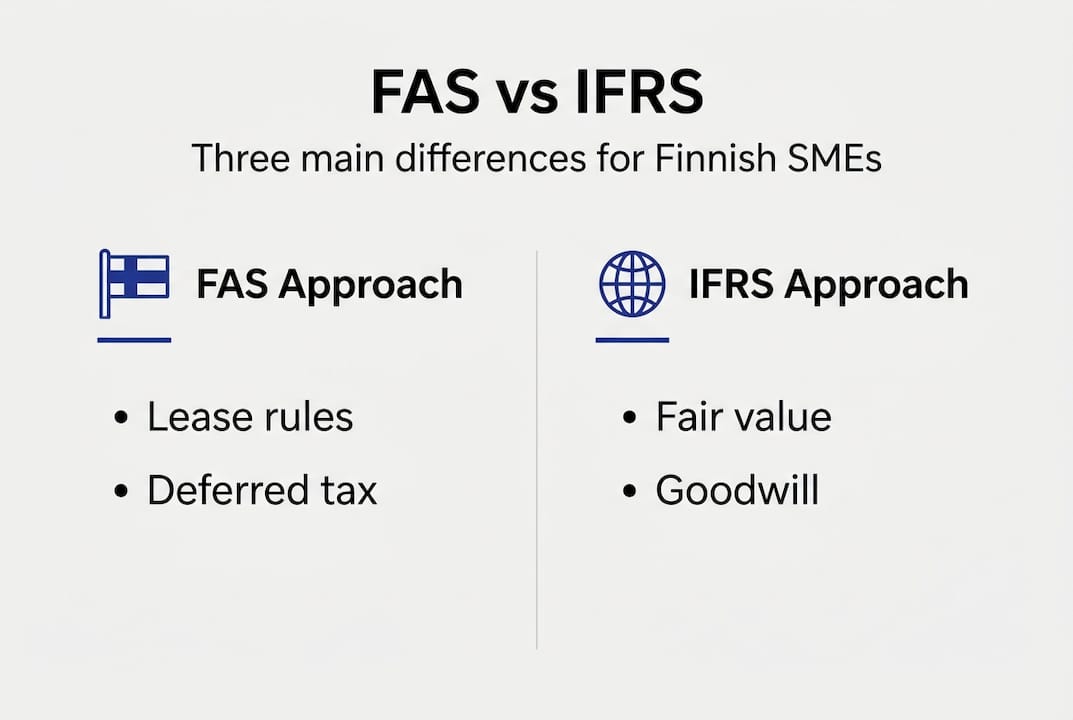

Accounting standards: Finnish (FAS) vs international (IFRS)

Two main sets of accounting standards apply in Finland: Finnish Accounting Standards (FAS) and International Financial Reporting Standards (IFRS). Knowing which one applies to your business matters because they produce meaningfully different financial statements.

Finnish SMEs typically use FAS, which is a prudent, creditor-focused framework. It is designed to be straightforward and conservative, prioritising reliable information for lenders and suppliers over market-based valuations. IFRS, by contrast, is mandatory for listed companies and public interest entities. It is more complex, uses fair value accounting more extensively, and requires significantly more disclosure.

The key differences between FAS and IFRS centre on three main areas: lease accounting, deferred tax treatment, and goodwill. Under FAS, lease payments are typically expensed as incurred. Under IFRS, most leases must be recognised on the balance sheet as both an asset and a liability. This can significantly change how a business looks to external stakeholders.

| Area | FAS approach | IFRS approach |

|---|---|---|

| Lease accounting | Expensed as incurred | On-balance sheet (right-of-use asset) |

| Deferred tax | Limited recognition | Full recognition required |

| Goodwill | Amortised over useful life | Annual impairment test |

| Fair value | Rarely used | Widely applied |

| Disclosure requirements | Moderate | Extensive |

For most Finnish SMEs, FAS is entirely sufficient. Here are the typical scenarios where FAS works well:

- You operate as a private limited company (Oy) without listed shares

- Your investors and lenders are Finnish and familiar with FAS

- You do not have complex cross-border transactions requiring IFRS alignment

- Your business does not hold significant lease portfolios or intangible assets

"The choice between FAS and IFRS is not just a technical one. It reflects how transparent and comparable you need your financial statements to be, and for whom."

For light entrepreneurs and sole traders with non-calendar financial years, special rules may apply. Reviewing your accounting method options with a qualified professional ensures you apply the right standard from the outset.

Tax compliance, VAT, and audit requirements in Finland

Tax compliance is where accounting directly affects your cash flow and legal standing. In Finland, VAT registration is mandatory once your annual turnover exceeds €20,000. The standard VAT rate is 25.5%, with reduced rates of 14% for food and restaurant services and 10% for books, medicines, and passenger transport. Corporate income tax is set at 20% for all Finnish companies, calculated directly from your accounting records.

Here are the key steps for VAT registration and ongoing tax filing:

- Check whether your turnover exceeds or is approaching €20,000

- Register for VAT through MyTax (OmaVero) before the threshold is reached

- Set up your accounting system to record VAT on each transaction

- Submit VAT returns monthly, quarterly, or annually depending on your turnover

- Pay VAT liabilities by the due date to avoid interest charges

- File your corporate income tax return based on your annual financial statements

Pro Tip: Use digital accounting software that integrates directly with the Finnish Tax Administration's electronic reporting system. This reduces manual errors and ensures your filings are submitted on time.

Audit requirements in Finland are generally mandatory for companies that exceed certain size thresholds. However, there is an ongoing debate about audit requirements for micro-companies, with proposals to replace full audits with lighter review engagements. This proposal has attracted quality concerns from the profession, and no final decision has been reached as of 2026. Until the rules change, assume standard audit obligations apply unless your company clearly qualifies for an exemption.

| Item | Threshold or rate | Notes |

|---|---|---|

| VAT registration | €20,000 turnover | Mandatory above this level |

| Standard VAT rate | 25.5% | Most goods and services |

| Reduced VAT rate | 14% | Food, restaurants |

| Reduced VAT rate | 10% | Books, medicines, transport |

| Corporate income tax | 20% | All Finnish companies |

| Audit exemption | Small company criteria | Subject to ongoing review |

For a full overview of your obligations, our guide on tax compliance essentials covers the practical steps in detail. You can also explore how digital accounting tools can simplify your reporting process considerably.

Outsourcing accounting and practical improvements for SMEs

Many Finnish SMEs manage accounting in-house to save money. In practice, this often costs more than it saves. Research shows that outsourcing accounting measurably improves financial reporting quality for small firms, particularly in the accuracy of accruals and the timeliness of submissions. Businesses that outsource consistently show stronger compliance records and fewer regulatory penalties.

Here is how outsourcing accounting services directly benefits your business:

- Reduces the risk of errors in VAT returns and tax filings

- Ensures financial statements meet FAS requirements and deadlines

- Frees up management time for business development and operations

- Provides access to professional expertise without the cost of a full-time hire

- Improves the quality of financial data used for business decisions

- Keeps your business current with changes in Finnish tax law and reporting standards

Pro Tip: When selecting an accounting provider, prioritise firms with specific experience in Finnish SME legislation and electronic reporting. General accounting knowledge is not enough. You need someone who understands the nuances of Finnish VAT rules, FAS requirements, and the Tax Administration's digital systems.

Common pitfalls when outsourcing include inadequate handover of existing records, unclear service scope agreements, and poor communication about deadlines. Address these before signing any contract. A clear service level agreement that specifies deliverables, timelines, and responsibilities protects both parties.

If you are considering making the move, our articles on hiring a Finnish accountant and choosing the right accounting services provide practical guidance on what to look for. You can also read about the benefits of outsourcing bookkeeping and how accounting firms drive real business growth for Finnish SMEs.

Why accounting in Finland demands more than bookkeeping: vital lessons for SMEs

After working with Finnish SMEs across a range of industries, one pattern stands out clearly. Most business owners treat accounting as a back-office function. They deal with it when they must and delegate it to whoever is available. This reactive approach is where problems begin.

The businesses that grow steadily and avoid regulatory trouble treat accounting differently. They use their financial data to make decisions. They review management accounts regularly, not just at year end. They understand their VAT position before the return is due, not after. This is not about being an accounting expert. It is about recognising that your financial records are a live picture of your business health.

"Forward-thinking SMEs treat accounting as a strategic function. Reactive ones treat it as an annual obligation. The difference shows in their growth trajectories."

Our experience shows that real business growth comes from combining professional accounting support with active engagement from management. You do not need to understand every accounting standard. You do need to ask the right questions and act on the answers.

Expert Finnish accounting support: a smart next step

Navigating Finnish accounting regulations, VAT obligations, and financial reporting requirements takes time and expertise that most SME owners simply do not have to spare. That is where professional support makes a measurable difference.

At Finovate, we provide expert accounting support tailored to Finnish businesses of all sizes. From bookkeeping and VAT registration to financial statement preparation and tax planning, we handle the compliance burden so you can focus on growth. Light entrepreneurs can take advantage of our invoicing service pro or our flexible monthly invoicing option. Get in touch with us today to find out how we can support your business.

Frequently asked questions

Which accounting standards should Finnish SMEs use?

Finnish SMEs should apply Finnish Accounting Standards (FAS) in most cases. IFRS is mandatory only for listed companies and public interest entities.

When is VAT registration required for small businesses in Finland?

VAT registration becomes mandatory once your annual turnover exceeds €20,000. Different VAT rates apply depending on the type of goods or services you provide.

What are the key differences between FAS and IFRS for SMEs?

FAS is creditor-focused and conservative, while IFRS applies fair value more broadly and treats leases and goodwill differently, with more extensive disclosure requirements.

Is outsourcing accounting services beneficial for Finnish SMEs?

Yes. Empirical research confirms that outsourcing accounting improves financial reporting quality and reduces regulatory risk for small businesses.

Do all SMEs need an audit or are there exemptions?

Audits are generally required above certain size thresholds, but small companies may qualify for exemptions. Proposals to allow micro-company reviews instead of full audits are still being debated as of 2026.