Bookkeeping is one of those responsibilities that many small business owners in Finland treat as an afterthought, until a tax deadline looms or an audit notice arrives. The reality is that accurate, well-organised accounts are not just a legal requirement; they are the foundation of every sound business decision you make. Whether you are a sole trader or running a limited company, understanding your bookkeeping obligations protects you from penalties and gives you a clear picture of your financial health. This guide walks you through everything you need to know, from legal requirements and essential tools to VAT compliance and ongoing improvement.

Table of Contents

- Understanding bookkeeping obligations in Finland

- Preparing your bookkeeping system: Tools and documents

- Step-by-step guide: Setting up and maintaining your accounts

- VAT, income tax, and compliance: Avoiding pitfalls

- Verifying your bookkeeping: Audits, adjustments and ongoing improvement

- Our perspective: What most guides miss about Finnish bookkeeping success

- Finovate: Bookkeeping solutions for Finnish SMEs

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Legal bookkeeping duty | Every Finnish business, regardless of size, must maintain accurate accounts to stay compliant. |

| Choose the right method | Double-entry bookkeeping is mandatory if your business exceeds key thresholds, while single-entry may suffice for smaller operations. |

| Essential documentation | Always collect and store receipts, invoices, and equity records—for audits and reliable tax reporting. |

| VAT and tax compliance | Regular VAT and income tax filings depend on your turnover and proper bookkeeping is the foundation. |

| Continuous verification | Review your accounts and seek professional support to avoid compliance errors and improve financial management. |

Understanding bookkeeping obligations in Finland

Every business operating in Finland must maintain accounts, and management carries direct responsibility for ensuring this is done correctly. This is not optional. The Finnish bookkeeping rules make clear that all businesses must keep accounts, with management held personally accountable for compliance. Understanding the bookkeeping basics in Finland is the first step towards building a resilient financial system.

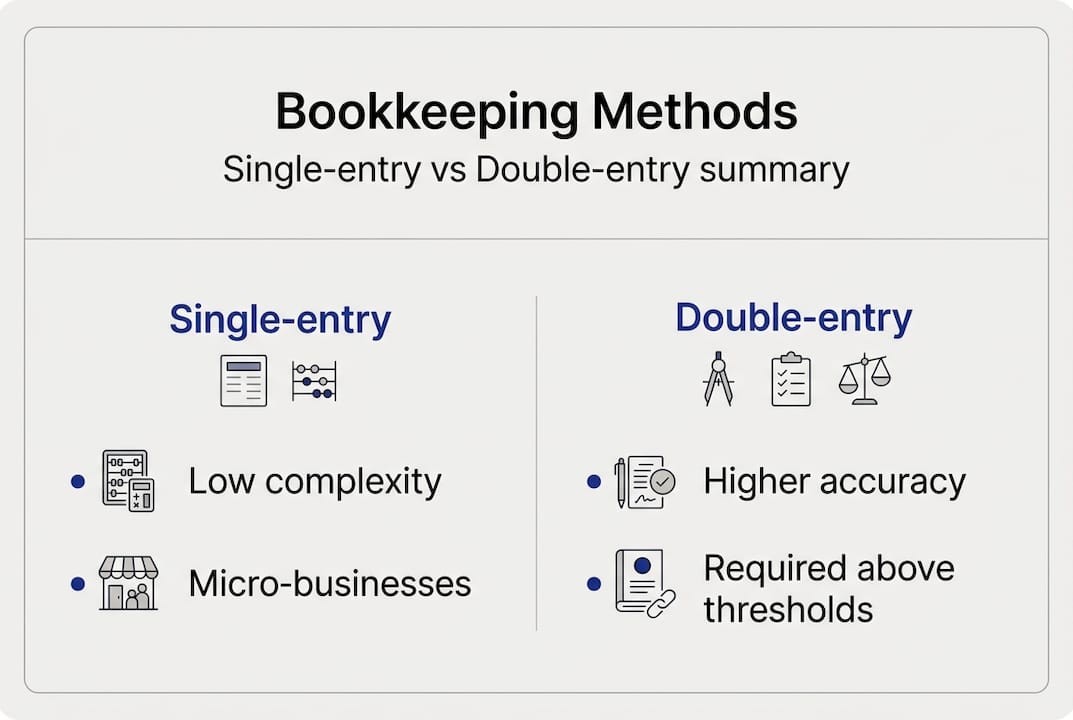

The two main bookkeeping methods are single-entry and double-entry. Single-entry is simpler and permitted for very small businesses that remain below certain thresholds. Double-entry records every transaction in two accounts simultaneously, providing a more complete picture of your finances. Double-entry bookkeeping is mandatory if your business exceeds two of the following three thresholds:

- Balance sheet total exceeds €100,000

- Annual turnover exceeds €200,000

- Average number of employees exceeds three

| Feature | Single-entry | Double-entry |

|---|---|---|

| Complexity | Low | Moderate to high |

| Required for | Micro businesses below thresholds | Businesses exceeding two thresholds |

| Financial insight | Limited | Detailed |

| Audit readiness | Basic | Strong |

Financial statements become mandatory once your business exceeds these thresholds. These statements must include a balance sheet, an income statement, and notes to the accounts. Reviewing the best practices for Finnish businesses can help you decide which method suits your situation and how to plan ahead. Many SMEs benefit from adopting double-entry from the outset, even when not legally required, because it supports better decision-making and smoother transitions as the business grows. Consulting accounting services early can prevent costly structural mistakes later.

Preparing your bookkeeping system: Tools and documents

Once you have grasped your bookkeeping obligations, the next step is assembling the right tools and documentation. A reliable bookkeeping system rests on three pillars: the right software, proper documentation habits, and a clear process for organising records.

For software, most Finnish SMEs use cloud-based accounting platforms that integrate with bank feeds and generate VAT reports automatically. These tools reduce manual errors and save significant time. Alongside your software, you must use MyTax, the Finnish Tax Administration's official online system, for filing tax returns and managing your business tax obligations. The MyTax filing instructions confirm that you must collect dated and numbered receipts, file returns through MyTax, and track equity carefully if you are self-employed.

Here is a summary of the key documents every Finnish SME should maintain:

| Document type | Purpose | Retention period |

|---|---|---|

| Sales invoices | Proof of income | 6 years |

| Purchase receipts | Expense verification | 6 years |

| Bank statements | Transaction reconciliation | 6 years |

| Equity records | Private use and capital tracking | 6 years |

| Payroll records | Employee tax compliance | 10 years |

Organising these documents consistently makes audits far less stressful and speeds up your annual tax return. A practical step-by-step bookkeeping guide can help you build this habit from day one. You should also explore automated bookkeeping tools that reduce manual data entry and flag discrepancies automatically.

Pro Tip: Even if you handle day-to-day bookkeeping yourself, scheduling a quarterly review with a professional accountant can catch errors before they become compliance problems. Review tax tips for Finnish entrepreneurs to stay ahead of common pitfalls.

Step-by-step guide: Setting up and maintaining your accounts

With tools in hand, it is time to tackle the core bookkeeping workflow for Finnish SMEs. Following a structured process from the start prevents gaps and keeps your records audit-ready throughout the year.

- Choose your bookkeeping method. Decide between single-entry and double-entry based on your current thresholds. Review accounting methods in Finland to understand the practical differences and choose accordingly.

- Define your financial year. The financial year is usually 12 months, though your first financial year can extend up to 18 months. Plan your year-end carefully, as financial statements must be prepared within four months of year-end if thresholds are exceeded.

- Record every transaction promptly. Each entry must include a date, a sequential reference number, and a clear category. Delays in recording create reconciliation problems and increase audit risk.

- Track assets, equity, and private use separately. If you use business assets for personal purposes, this must be recorded accurately. Mixing these creates compliance issues and distorts your financial picture.

- Reconcile your accounts monthly. Compare your bookkeeping records against bank statements every month. This catches errors early and keeps your records clean.

- File returns and statements through MyTax. Use the Finnish financial year rules to confirm your filing deadlines and submit all required returns on time.

Pro Tip: If you are a freelancer or self-employed, the rules around equity and private asset use can be particularly complex. Reading about freelancer accounting in Finland will help you avoid the most common structural errors.

Key statistic: Financial statements must be completed within four months of the financial year-end for businesses that exceed the statutory thresholds. Missing this deadline can trigger penalties and tax investigations.

VAT, income tax, and compliance: Avoiding pitfalls

Accurate bookkeeping underpins VAT and income tax compliance. Here is what Finnish SMEs need to know to stay on top of obligations.

VAT registration becomes mandatory once your annual turnover exceeds €20,000. Finland's corporate income tax rate is 20%, and your tax liability is calculated directly from your accounting records. This means inaccurate bookkeeping does not just create administrative headaches; it can result in incorrect tax assessments. Reviewing tax compliance for Finnish SMEs will help you understand how your records feed into your tax obligations.

The Finnish tax handbook is explicit: you must separate business and personal finances at all times. This is one of the most common mistakes we see among small business owners, and it is one of the most damaging.

Common compliance pitfalls to avoid:

- Failing to register for VAT when turnover crosses €20,000

- Missing VAT filing deadlines based on your turnover band

- Mixing personal and business transactions in the same account

- Failing to keep receipts for all business expenses

- Incorrectly categorising private asset use

"Taxes are based on your accounting records. Inaccurate records lead to inaccurate tax returns, which can trigger audits and penalties."

Pro Tip: Set up a dedicated business bank account from day one. This single step eliminates the most common source of bookkeeping errors and makes VAT reconciliation straightforward.

Verifying your bookkeeping: Audits, adjustments and ongoing improvement

Ongoing checks and periodic reviews ensure your accounts remain accurate and robust. Here is how to verify your bookkeeping and continuously improve.

Statutory audits are triggered when your business exceeds certain size thresholds. The Finnish audit benchmarks define the distinction between micro, small, and medium businesses, and exceeding these thresholds triggers audit requirements and mandatory financial statements. Knowing where you stand helps you plan ahead.

- Conduct a monthly reconciliation. Compare your bookkeeping records to bank statements and identify any discrepancies immediately.

- Review your chart of accounts annually. As your business evolves, your account categories may need updating to reflect new income streams or expense types.

- Correct errors promptly. If you discover a mistake, record a correcting entry with a clear reference to the original transaction. Never delete or overwrite past entries.

- Engage an accounting firm for periodic reviews. An external review by a professional catches systemic issues that internal checks often miss.

| Action | Frequency | Benefit |

|---|---|---|

| Bank reconciliation | Monthly | Catches errors early |

| Account category review | Annually | Keeps records relevant |

| Professional audit review | Annually or as needed | Ensures compliance |

| Error correction log | As needed | Maintains audit trail |

Consider outsourcing bookkeeping if internal resources are stretched. Professional support is not just about compliance; it frees you to focus on growing your business while experts manage the detail.

Our perspective: What most guides miss about Finnish bookkeeping success

Most bookkeeping guides focus on the mechanics: which method to use, which forms to file, which deadlines to meet. These matter, but they miss the deeper issue. The businesses that struggle most with bookkeeping are not those that lack knowledge. They are the ones that treat bookkeeping as a reactive task rather than a proactive discipline.

We have worked with many Finnish SMEs that adopted double-entry bookkeeping from day one, even when single-entry was legally sufficient. The financial insights from double-entry far outweigh the additional effort, particularly when seeking financing or navigating a tax review. Early mistakes with private asset tracking are another area where we see significant, avoidable costs. Many micro-entrepreneurs underestimate how carefully this must be recorded.

Our strongest advice: engage professional support early. Reviewing your options for choosing accounting services before problems arise is far less costly than correcting errors after the fact. Continuous, active review matters more than simply ticking compliance boxes once a year.

Finovate: Bookkeeping solutions for Finnish SMEs

If this guide has highlighted gaps in your current bookkeeping setup, we are here to help you close them. At Finovate, we provide tailored bookkeeping, payroll, and tax services designed specifically for Finnish SMEs and entrepreneurs.

Our team ensures your accounts remain compliant, your deadlines are met, and your financial records give you the clarity to make confident business decisions. Whether you need a straightforward monthly invoicing service or a more structured solution like our Invoicing Service Pro, we have options to fit your needs. Visit Finovate today to explore how we can support your business with expert, reliable financial management.

Frequently asked questions

Do I need double-entry bookkeeping as a sole trader in Finland?

You must use double-entry bookkeeping if your business exceeds two of these thresholds: €100,000 balance sheet, €200,000 turnover, or three employees. Below these thresholds, single-entry is permitted, but accruals must still be adjusted for tax purposes.

How often do I file VAT returns as a Finnish SME?

The frequency depends on your annual turnover: monthly if turnover exceeds €100,000, quarterly between €30,000 and €100,000, and annually below €30,000.

What happens if I miss bookkeeping deadlines?

Missing deadlines can trigger audits, penalties, and tax investigations. Financial statements are required within four months of year-end if your business exceeds the statutory thresholds.

Can I use MyTax to file all business returns in Finland?

Yes, MyTax is the official platform for filing returns, making payments, and managing all business tax obligations in Finland.

Should I separate business and personal finances?

Yes, separating these finances is a compliance requirement and simplifies both auditing and tax reporting significantly.