Bookkeeping is not optional in Finland. Every business, from a sole trader to a limited company, is legally required to maintain accounts, and management bears direct responsibility for accuracy. Get it wrong and you risk missed tax savings, penalty charges, or a stressful audit. Get it right and your books become a genuine decision-making tool. This guide walks you through every stage of the process, from choosing the right system to filing your returns with confidence.

Table of Contents

- What is bookkeeping and why does it matter?

- Choosing your bookkeeping system: single-entry or double-entry

- Preparing for efficient bookkeeping: tools, records and setup

- The step-by-step Finnish bookkeeping process

- Common mistakes and how to avoid them

- Reviewing your books: accuracy, benchmarks and when to seek help

- Professional bookkeeping and accounting services in Finland

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Legal requirement | Every Finnish business must keep accurate accounts and submit returns to stay compliant. |

| Choose the right system | Single-entry is allowed for many sole traders, but double-entry is often better for business growth. |

| Stepwise workflow | Following a clear process minimises mistakes and simplifies tax filing and reporting. |

| Watch for pitfalls | Common errors include missing documents and VAT returns—early detection averts bigger issues. |

| Get expert support | Professional services can save time, reduce risk, and provide strategic insights for your business. |

What is bookkeeping and why does it matter?

Bookkeeping is the systematic recording of every financial transaction your business makes. In Finland, it forms the legal foundation for calculating both VAT on sales revenue and income tax on your adjusted result. Put simply, your tax bill is only as accurate as your books.

Management is responsible for ensuring accounts are kept correctly, even if the day-to-day work is delegated to a bookkeeper or accountant. This means you cannot simply hand over a shoebox of receipts and assume everything will be fine. Understanding the basics protects you.

Here are the core bookkeeping terms you will encounter:

- Revenue: Money received from sales or services

- Expense: Costs incurred to run the business

- Balance sheet: A snapshot of assets, liabilities, and equity at a given date

- Profit and loss statement: A summary of income and expenses over a period

- Reconciliation: Matching your records against your bank statement

Accurate books also open doors. They help you spot cash flow problems early, support loan applications, and inform pricing decisions. For practical guidance on reducing your tax burden legally, see these tax tips for Finnish entrepreneurs.

| Term | What it means |

|---|---|

| Debit | An entry recording money coming in or an asset increasing |

| Credit | An entry recording money going out or a liability increasing |

| Ledger | The master record of all financial transactions |

| Accruals basis | Recording income/expenses when earned or incurred, not when paid |

| Payment basis | Recording only when cash actually changes hands |

Now that we have established the critical importance of bookkeeping for Finnish businesses, let us clarify the bookkeeping systems available to you.

Choosing your bookkeeping system: single-entry or double-entry

Finland recognises two main bookkeeping methods, and the rules on which one you must use are clear.

Double-entry bookkeeping is mandatory for all companies and corporations. It is also required for self-employed individuals and business operators who meet two of the following three thresholds: a balance sheet exceeding €100,000, turnover exceeding €200,000, or an average of more than three employees. Single-entry bookkeeping, recorded on a payment basis, is only permitted for sole traders who fall below these thresholds and must use a calendar year as their financial year.

| Feature | Single-entry | Double-entry |

|---|---|---|

| Who can use it | Sole traders below thresholds | All companies; larger sole traders |

| Complexity | Lower | Higher |

| Planning power | Limited | Strong |

| Tax compliance | Adjusted to accruals for tax | Direct accruals basis |

| Financial statements | Simplified | Full balance sheet required |

For most SMEs, double-entry is the only legal option. But even sole traders who qualify for single-entry often choose double-entry voluntarily. Why? Because it gives you a full picture of your business health, supports budgeting, and makes scaling far simpler. Review the company accounting requirements for your specific business structure before deciding.

Pro Tip: If you plan to grow, apply for a loan, or bring in investors within the next few years, start with double-entry bookkeeping now. Switching systems mid-stream is time-consuming and disruptive.

With your bookkeeping system chosen, you can lay the groundwork for a smooth and compliant workflow.

Preparing for efficient bookkeeping: tools, records and setup

Before you record a single transaction, you need the right infrastructure in place. This is where many Finnish business owners lose time later, because they skip the setup stage.

Start by gathering the essential tools:

- Accounting software (cloud-based options integrate directly with Finnish banking and tax systems)

- A dedicated business bank account, separate from personal finances

- A secure folder system, physical or digital, for storing documents

- A spreadsheet or ledger template if you are using manual methods

The step-by-step bookkeeping process starts with collecting and storing all receipts and documents, each dated and numbered. This is not just good practice; it is a legal requirement. Documents must be kept for at least six years after the end of the financial year.

Here is a simple schedule to keep your records current:

| Frequency | Task |

|---|---|

| Daily | Collect and store receipts; record sales |

| Weekly | Categorise expenses; check outstanding invoices |

| Monthly | Reconcile bank statements; review VAT position |

| Quarterly | Review profit and loss; check tax prepayments |

| Annually | Prepare financial statements; file tax returns |

Clear document labelling matters more than most owners realise. Number every invoice sequentially, note the business purpose on receipts, and store digital copies as backups. Explore Finnish accounting software options that automate much of this categorisation for you.

With your tools and records in place, you are ready to begin the actual bookkeeping routine.

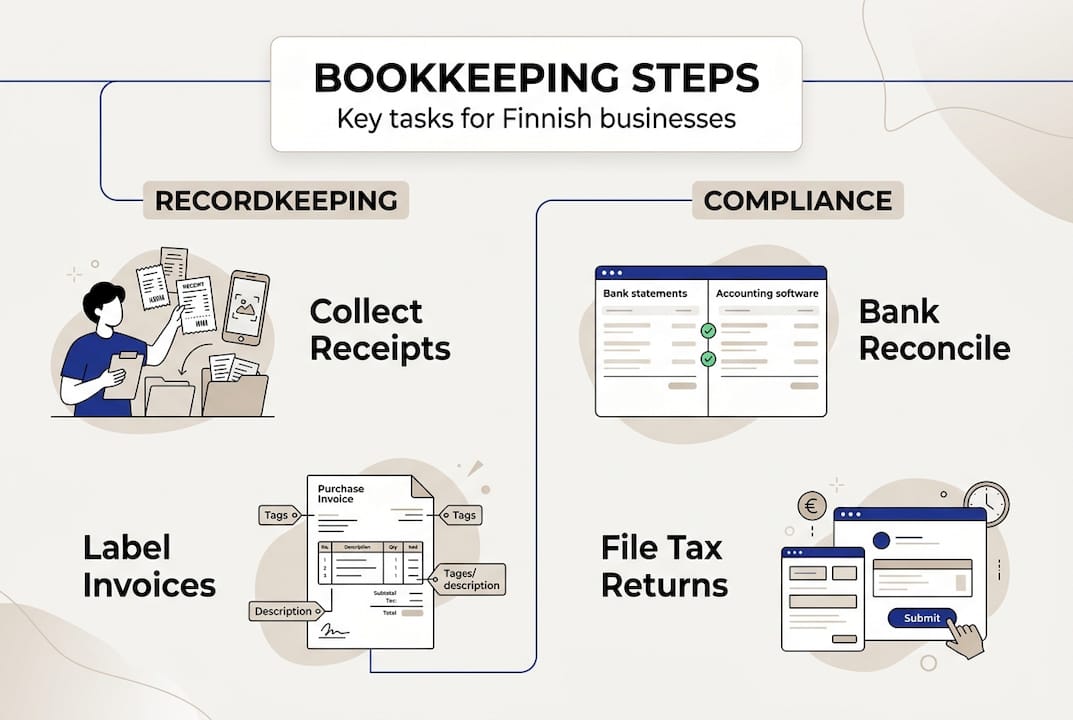

The step-by-step Finnish bookkeeping process

Following a consistent process is what separates businesses that sail through audits from those that scramble at year-end. Here is the full workflow.

- Store all receipts and documents by date and reference number as soon as they arrive. Do not let them accumulate.

- Record every transaction in your chosen system promptly. For double-entry, every debit must have a corresponding credit.

- Reconcile your bank statements monthly. Match each transaction in your records to your bank statement line by line.

- Prepare your financial statements, including a profit and loss statement and balance sheet, within four months of your financial year end.

- File your tax returns accurately and on time using MyTax or compatible accounting software. The standard deadline for self-employed individuals is 1 April.

The full bookkeeping workflow covers recording, reconciliation, statement preparation, and tax filing. Missing any stage creates gaps that compound over time.

Pro Tip: Set a recurring calendar reminder for the 10th of each month to complete your previous month's reconciliation. Staying one month behind is manageable; six months behind is a crisis.

One important compliance point: financial statements are public for companies registered in the Trade Register. This means your balance sheet and profit and loss figures are visible to suppliers, customers, and competitors. Accuracy is not just a legal matter; it is a reputational one.

For businesses operating as light entrepreneurs, the legal bookkeeping steps differ slightly from those for limited companies. If you are unsure which rules apply to you, professional accounting services can clarify your obligations quickly. You can also review profit and loss statement requirements for limited companies specifically.

Even with a clear workflow, it is easy to trip up on technical details. Let us explore the most common pitfalls.

Common mistakes and how to avoid them

Most bookkeeping errors are not caused by dishonesty. They come from confusion, rushed entries, or simply not knowing the rules. Here are the mistakes we see most often.

- Missing or incomplete receipts: Without documentation, expenses cannot be deducted. Photograph receipts immediately.

- Incorrect VAT rates: The standard VAT rate is 25.5%, with reduced rates of 13.5% and 10% for specific goods and services. Applying the wrong rate creates a liability.

- Skipping VAT returns: You must file VAT returns even during periods of no activity. Missed filings attract automatic penalties.

- Mixing personal and business finances: This is the single most common problem for sole traders. A dedicated business account eliminates most of the confusion.

- Misclassifying withdrawals: Negative equity from withdrawals requires loans to be recorded as income. Getting this wrong distorts your tax position significantly.

Other edge cases that catch business owners off guard include the private use of business assets, which must be recorded as income, and the division of income between spouses when both work in the business. Review the taxation nuances for self-employed individuals if either situation applies to you.

Pro Tip: If you discover an error, correct it promptly with a dated adjustment entry. Do not delete the original record. Transparent corrections are viewed far more favourably by tax authorities than unexplained discrepancies.

For a broader look at avoiding costly errors, the common tax mistakes guide covers the most frequent filing problems Finnish entrepreneurs face.

Taking these precautions will set you up for success. Now let us look at how to verify your work and know when to ask for help.

Reviewing your books: accuracy, benchmarks and when to seek help

Completing your books is one thing. Knowing they are correct is another. A structured review process catches errors before they become problems.

Use this checklist before closing each period:

- All bank transactions are matched and reconciled

- VAT figures match your sales and purchase records

- Outstanding invoices are accounted for

- Payroll entries match payslips and pension contributions

- Depreciation has been applied to fixed assets

Beyond compliance, your books should tell you something useful. Double-entry bookkeeping supports planning and budgeting in ways that single-entry simply cannot. Track your current ratio (current assets divided by current liabilities) to monitor short-term financial health, and watch your net profit margin against industry norms.

Knowing when to bring in a professional is equally important. There are approximately 468 bookkeeping services in Finland, with 90% operating as single-owner firms and the highest concentration in Uusimaa. Choice is not the problem; finding the right fit is. Look for a provider who understands your industry, communicates clearly, and uses software compatible with your own systems.

Signs you need professional help include: your business is growing rapidly, you have employees, you are dealing with cross-border VAT, or you simply do not have time to stay current. Tracking key financial ratios regularly will also tell you when your numbers need a professional eye.

Professional bookkeeping and accounting services in Finland

Managing your own books is achievable, but there comes a point where professional support pays for itself many times over. Errors in VAT filings, missed deductions, or misclassified transactions can cost far more than an accountant's fee.

At Finovate, we provide accounting and bookkeeping expertise tailored to Finnish SMEs, from sole traders to limited companies. Whether you need help with monthly reporting, VAT compliance, or payroll, our services are designed to keep you compliant and give you clear visibility over your finances. Our invoicing and monthly reporting service is particularly popular with light entrepreneurs and growing businesses that need reliable, regular support without the overhead of a full-time accountant. Explore our full-service accounting support to find the right option for your business.

Frequently asked questions

Do all small businesses in Finland need to do bookkeeping?

Yes. All Finnish businesses must keep accounts, regardless of size, and management bears direct legal responsibility for accuracy.

What are the main differences between single-entry and double-entry bookkeeping?

Single-entry tracks cash in and out only, while double-entry is mandatory for companies and records both the source and use of every transaction, giving a fuller financial picture.

How often must I reconcile bank statements and file tax returns?

Reconcile monthly. Financial statements must be prepared within four months of your financial year end, and most tax returns are due by 1 April for self-employed individuals.

What VAT rates apply to most Finnish SMEs?

The standard VAT rate is 25.5%, with reduced rates of 13.5% and 10% for certain goods and services. Businesses with turnover below €20,000 may qualify for a small business exemption.

Is it better to use an accountant or handle bookkeeping yourself in Finland?

DIY bookkeeping is possible for straightforward businesses, but most experts recommend professional support to ensure compliance and identify tax planning opportunities that owners often miss.

Recommended

- Essential Tax Tips for Finnish Entrepreneurs | Finovate Accounting Services

- Blog Posts | Finovate Accounting Services

- Accounting for delivery partners (Finland)

- Products | Finovate Accounting Services

- Bookkeeping best practices 2026 for Birmingham SMEs

- How to Read Financial Statements: Easy Guide for 2025 - Ready Accounting