TL;DR:

- Finnish SMEs must choose between single-entry and double-entry bookkeeping based on turnover and structure.

- Building a reliable workflow involves capturing, categorizing, reconciling, and reviewing transactions regularly.

- Effective process design is crucial for accurate reporting, enabling better financial decisions and growth.

Disorganised bookkeeping costs Finnish SMEs far more than time. Missed VAT deadlines, inaccurate financial reports, and muddled expense records can trigger penalties, cloud your decision-making, and stall growth. Many business owners and financial managers spend hours each month wrestling with manual processes that could be streamlined with the right framework. This guide walks you through the legal requirements, preparation steps, and a practical workflow to improve your bookkeeping from the ground up. Whether you run a sole proprietorship or a growing limited company, you will leave with a clear, actionable plan tailored to Finland's regulatory environment.

Table of Contents

- Understanding Finnish bookkeeping requirements for SMEs

- Preparing your SME for improved bookkeeping workflow

- Step-by-step workflow for SME bookkeeping in Finland

- Verifying, troubleshooting, and optimising your bookkeeping workflow

- Editorial perspective: why SME bookkeeping workflow needs more than compliance

- Efficient bookkeeping solutions for Finnish SMEs

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Know bookkeeping thresholds | Identify if single-entry or double-entry applies for your SME to stay compliant and efficient. |

| Prepare before you start | Gather software, tools, and documents up front to avoid workflow disruptions. |

| Follow a proven workflow | Sequential steps tailored for Finnish SMEs will boost clarity and financial accuracy. |

| Automate and verify regularly | Leverage digital tools, but audit your workflow often to catch mistakes and achieve continuous improvement. |

Understanding Finnish bookkeeping requirements for SMEs

Before you can optimise anything, you need to understand what Finnish law actually requires of you. The rules differ significantly depending on your business structure, turnover, and operational complexity. Getting this wrong from the start creates compliance risks that are difficult and costly to unwind later.

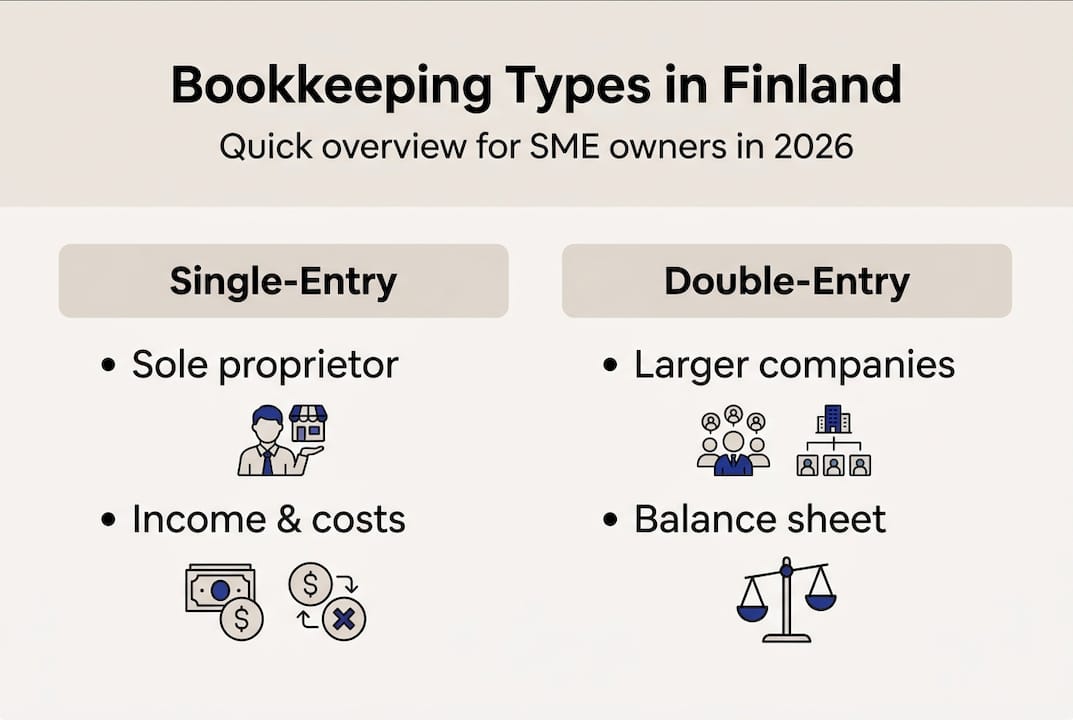

Finland recognises two primary bookkeeping systems. Single-entry bookkeeping records only income and expenses, much like a personal cash ledger. Double-entry bookkeeping records every transaction as both a debit and a credit, providing a full picture of assets, liabilities, and equity. The bookkeeping basics Finland guide explains these distinctions clearly for SME owners starting out.

Which system applies to your business?

The following table summarises the key thresholds and obligations:

| Business type | Turnover threshold | Employees | Bookkeeping system required |

|---|---|---|---|

| Sole proprietor | Below €200,000 | None | Single-entry permitted |

| Sole proprietor | Above €200,000 | Any | Double-entry required |

| Limited company (Oy) | Any | Any | Double-entry always required |

| Partnership (Ay/Ky) | Any | Any | Double-entry always required |

According to Finnish SME requirements, sole proprietors meeting all three conditions (turnover below €200,000, no employees, and only domestic sales) may use single-entry bookkeeping. All other entities must use double-entry.

Key compliance obligations for Finnish SMEs include:

- Financial year: Typically the calendar year (1 January to 31 December), though some entities may use a non-calendar financial year of exactly 12 months.

- Retention period: Bookkeeping records must be retained for at least six years after the end of the financial year.

- VAT reporting: Depending on turnover, VAT returns may be filed monthly, quarterly, or annually.

- Income tax returns: Filed annually, with deadlines set by the Finnish Tax Administration (Vero).

Pro Tip: If your turnover is approaching €180,000, plan now for the transition to double-entry bookkeeping. Switching mid-year is disruptive. Build the infrastructure before you cross the threshold, not after.

The bookkeeping compliance guide provides a structured checklist to confirm you are meeting all mandatory obligations throughout the year.

Preparing your SME for improved bookkeeping workflow

Understanding the rules is one thing. Building a workflow that consistently meets them is another. Preparation is where most SMEs either set themselves up for success or unknowingly create future problems.

Start by assessing your current setup against this checklist:

- Accounting software: Are you using a Finnish-compliant platform such as Procountor, Netvisor, or Visma Fivaldi? Cloud-based tools reduce manual entry and support automated bank feeds.

- Document management: Do you have a reliable system for capturing and storing receipts, invoices, and bank statements digitally?

- Chart of accounts: Is your chart of accounts aligned with Finnish accounting standards and your specific business activities?

- Bank account separation: Are your business and personal finances fully separated? Mixing them is one of the most common and costly mistakes.

- Access controls: Who in your team has access to financial records, and are those permissions appropriate?

Research on automation maturity in Finnish SMEs identifies four maturity levels: manual, partially automated, mostly automated, and fully intelligent. Most small businesses sit at level one or two, meaning significant efficiency gains are available without major investment.

The table below maps common business models to recommended workflow approaches:

| Business model | Recommended approach | Priority tools |

|---|---|---|

| Freelancer or sole trader | Single-entry, quarterly review | Simple invoicing software |

| Service-based SME (under 10 staff) | Double-entry, monthly close | Cloud accounting platform |

| Product-based SME | Double-entry, automated stock sync | ERP-integrated accounting |

| Light entrepreneur | Invoicing service, outsourced books | Specialist invoicing platform |

To automate bookkeeping effectively, you need sound process design first. Software cannot fix a broken workflow; it only speeds it up. Review your bookkeeping best practices before selecting or upgrading any tool.

A well-designed bookkeeping website or client portal can also support transparency and document sharing between your business and your accountant, reducing back-and-forth and improving response times.

Step-by-step workflow for SME bookkeeping in Finland

With your preparation complete, you can now build a repeatable, reliable bookkeeping workflow. The steps below apply to both single-entry and double-entry systems, with notes where the approach differs.

Step 1: Capture all transactions promptly Record every income and expense as it occurs. Use your accounting software's mobile app to photograph receipts immediately. Delayed entry is the single biggest source of errors and omissions.

Step 2: Categorise transactions correctly Assign each transaction to the correct account in your chart of accounts. Misclassification distorts your profit and loss report and can cause issues during tax filing. For double-entry systems, ensure each entry has a corresponding debit and credit.

Step 3: Reconcile your bank accounts monthly Compare your accounting records against your bank statements every month without exception. Reconciliation catches errors, duplicate entries, and fraud early. For step-by-step bookkeeping guidance specific to Finnish businesses, refer to our detailed process guide.

Step 4: Manage VAT reporting on schedule Calculate and submit VAT returns according to your assigned reporting period. Late or incorrect VAT submissions attract penalties from Vero. Set calendar reminders at least one week before each deadline.

Step 5: Prepare period-end reports At the end of each month or quarter, generate your profit and loss statement and balance sheet. These reports tell you whether your business is financially healthy and support informed decisions.

Step 6: Close the financial year accurately For single-entry cash basis taxpayers, the financial year follows the calendar year. For double-entry entities, the financial year may be flexible, but must be exactly 12 months. Year-end closing includes accruals adjustments, depreciation entries, and preparation of financial statements.

Pro Tip: Automate your bank feed connection so transactions import daily. This alone reduces manual data entry by up to 60% and keeps your records current.

Common pitfall: Many SMEs skip the monthly reconciliation step when busy, then face hours of correction work at year-end. Treat reconciliation as non-negotiable, not optional.

If errors do occur, address them immediately. The guide on how to fix bookkeeping errors outlines correction methods that keep your records compliant.

Verifying, troubleshooting, and optimising your bookkeeping workflow

Building a workflow is not a one-time task. Verification and ongoing optimisation are what separate businesses with genuine financial clarity from those that merely stay compliant.

Verification steps to perform regularly:

- Monthly bank reconciliation: Already covered in the workflow, but worth reinforcing as your primary accuracy check.

- VAT reconciliation: Cross-check your VAT return figures against your sales and purchase ledgers before submission.

- Payroll reconciliation: If you have employees, confirm that payroll costs in your books match actual payments and pension contributions.

- Aged receivables review: Check outstanding invoices monthly. Unpaid invoices affect cash flow and may need to be written off if unrecoverable.

- Expense audit: Quarterly, review your expense categories for any misclassifications or unusual items.

Troubleshooting common issues:

- Unexplained bank differences: Usually caused by timing differences, duplicate entries, or unrecorded bank charges. Trace each item systematically.

- VAT discrepancies: Often result from incorrect tax codes on invoices. Review your software's tax code settings against current Finnish VAT rates.

- Missing receipts: Establish a clear policy for expense submission deadlines and use digital receipt capture tools to prevent gaps.

The automation maturity model for Finnish SMEs shows that businesses at higher automation levels spend significantly less time on manual corrections and report greater confidence in their financial data.

Pro Tip: Schedule a 30-minute workflow review every quarter. Ask three questions: What took the most time? What caused the most errors? What can be automated or outsourced? This structured approach surfaces improvements you would otherwise miss.

For businesses ready to move beyond basic compliance, digital accounting efficiency strategies can significantly reduce administrative burden. If internal capacity is limited, it may be worth considering whether to outsource bookkeeping to a specialist firm.

Editorial perspective: why SME bookkeeping workflow needs more than compliance

Most articles on bookkeeping stop at compliance. Meet the deadline, file the return, keep the records. That is necessary, but it is not sufficient.

In our experience working with Finnish SMEs, the businesses that grow with confidence are those that use their bookkeeping data actively. They spot cash flow gaps before they become crises. They identify which services or products are genuinely profitable. They make pricing decisions based on real numbers, not instinct.

The uncomfortable truth is that software alone does not create this clarity. We have seen businesses invest in sophisticated accounting platforms and still produce unreliable reports, because the underlying process design was flawed. Automation amplifies whatever workflow you already have, good or bad.

Workflow quality is a strategic asset. A well-designed bookkeeping process gives you the financial visibility to act quickly when opportunities or risks emerge. That agility is worth far more than the time saved on data entry.

If you are reviewing your accounting services Finland options, prioritise partners who focus on process design alongside technology, not just software implementation.

Efficient bookkeeping solutions for Finnish SMEs

Applying this workflow consistently takes time and expertise. If you would rather focus on running your business, we are here to help.

At Finovate, we provide tailored bookkeeping and accounting services designed specifically for Finnish SMEs. Whether you need support with a monthly invoicing service, a fully managed Invoicing Service Pro, or accounting for light entrepreneurs, we have a solution that fits your business model. Our team handles compliance, reconciliations, and reporting so you can focus on growth. Explore our full range of Finovate accounting solutions and take the next step towards genuine financial clarity.

Frequently asked questions

What bookkeeping system is required for very small Finnish SMEs?

Sole proprietors with turnover below €200,000, no employees, and only domestic sales can use single-entry bookkeeping. If any of these conditions change, double-entry becomes mandatory.

Can I automate SME bookkeeping tasks in Finland?

Yes, digital tools can streamline invoicing, reconciliations, and reporting, but the automation maturity model shows that sound process design must come first for automation to deliver reliable results.

How often should I review my SME bookkeeping workflow?

Review your workflow quarterly or after any significant business change. The financial year calendar provides natural review points aligned with reporting obligations.

Recommended

- Why automate bookkeeping: boost efficiency and cut costs

- Digital accounting for Finnish SMEs: boost efficiency in 2026

- Finnish SME bookkeeping guide: compliance and success

- Bookkeeping best practices for Finnish small businesses

- Websites for Bookkeepers — Custom Bookkeeping Website Design | SiteForCPA