TL;DR:

- Finnish entrepreneurs must maintain accurate and organized financial records to ensure legal compliance and proper tax reporting. Implementing a double-entry bookkeeping system and consistently reconciling accounts help prevent errors and streamline tax season. Regular habits like weekly review and secure document storage are essential for long-term financial health and compliance.

Even the most diligent Finnish entrepreneurs can find their finances tangled when business and personal money blend together, or when receipts vanish just before tax season. This is a common and costly problem. Poorly organised accounts lead to inaccurate VAT filings, missed deductions, and unnecessary stress when Vero, the Finnish Tax Administration, comes calling. This guide walks you through practical, evidence-based steps to structure your business finances in line with Finnish requirements, so that tax time feels manageable rather than overwhelming.

Table of Contents

- Why structured finances matter for Finnish businesses

- Getting started: Setting up your bookkeeping system

- The practical workflow: Step-by-step finance organisation

- Common pitfalls and expert solutions

- Verifying your records and preparing for taxes

- A fresh perspective: What most guides miss about Finnish business finance

- Take your business finances to the next level

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Keep business and personal finances separate | Mixing accounts leads to tax confusion and risks compliance in Finland. |

| Choose the right bookkeeping system | Most Finnish companies require double-entry accrual systems for accurate accounting and taxation. |

| Organise and store every document | Properly dated and numbered receipts are crucial for audits and tax returns. |

| Verify and prepare before tax time | Regular checks of your accounts and documents prevent year-end stress and errors. |

| Expert help ensures compliance | Using accountants or professional services increases accuracy and lets you focus on running your business. |

Why structured finances matter for Finnish businesses

Organising your business finances is not simply a matter of good practice. In Finland, it is a legal obligation with real consequences if you get it wrong. The Finnish Tax Administration is clear: taxes are based on the books, meaning your income tax and VAT obligations are calculated directly from your official accounting records. If those records are incomplete or inaccurate, your tax liability may be miscalculated, and penalties can follow.

There are four core reasons why structured finances matter for Finnish business owners:

- Legal compliance: Finnish law requires businesses to maintain proper bookkeeping. Failure to do so can result in fines or, in serious cases, criminal liability.

- Accurate tax and VAT reporting: VAT is based on your sales revenue, and income tax is paid on the result shown by your accounts after statutory adjustments. Errors in your books translate directly into errors on your tax returns.

- Personal financial protection: Proper Finnish bookkeeping best practices ensure that your company's finances are kept separate from your personal assets, income, and expenses. This separation protects you personally if the business faces financial difficulties.

- Better business decisions: Clean, up-to-date accounts give you a clear picture of profitability, cash flow, and growth potential. Banks and investors also expect well-organised records before extending credit or funding.

"In Finland, separating and organising your bookkeeping is essential because taxes are based on the accounts, and business accounting separates the company's and entrepreneur's personal finances." — Finnish Tax Administration (Vero)

Understanding bookkeeping basics early in your business journey prevents expensive corrections later. The sooner you establish a solid structure, the more confident you will feel at every stage of your business.

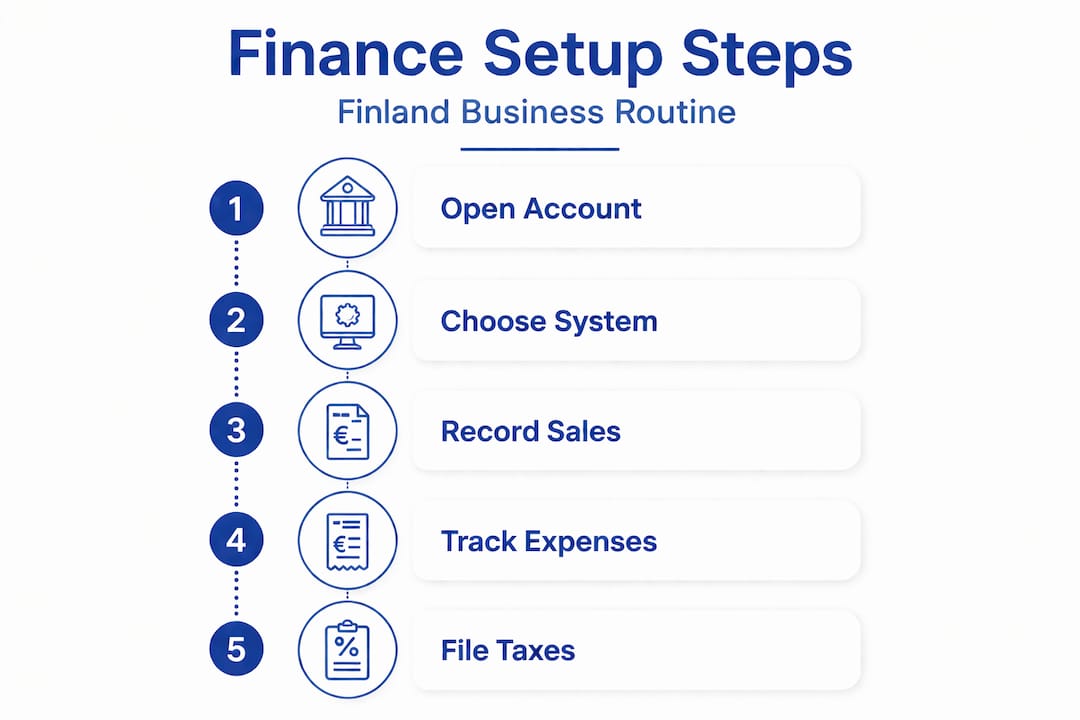

Getting started: Setting up your bookkeeping system

Once you understand why structure matters, the next step is choosing and implementing a bookkeeping system that fits both your legal obligations and your day-to-day needs.

In Finland, double-entry bookkeeping on an accruals basis is mandatory for companies and corporations. Single-entry bookkeeping is permitted in limited cases, typically for self-employed individuals operating under a business name (toiminimi), but even then, you must adjust your records on an accruals basis for taxation purposes. This means that even if you track income when it arrives in your bank account, you will need to make adjustments to reflect when revenue was actually earned and when costs were actually incurred.

Choosing the right system from the start saves significant time and effort. Here is a comparison of the main tools available to Finnish entrepreneurs:

| Tool type | Best for | Key benefits | Limitations |

|---|---|---|---|

| Accounting software (e.g., Procountor, Netvisor) | SMEs and growing businesses | Automated VAT, real-time reports | Monthly subscription cost |

| Cloud storage (e.g., Google Drive, OneDrive) | All business sizes | Easy document access and backup | Not a standalone accounting solution |

| Receipt management apps (e.g., Receiptful, Expensify) | Sole traders and small teams | Instant digital capture of receipts | Requires integration with accounting software |

| Spreadsheet-based systems | Very small or new businesses | Low cost, flexible | Manual, error-prone, not scalable |

Following a clear bookkeeping step-by-step process from the outset will help you avoid common setup mistakes. It is also worth reviewing Finnish accounting essentials to ensure your chosen system aligns with Vero's requirements.

Pro Tip: When selecting accounting software, confirm that it supports Finnish VAT reporting formats and can generate the reports required for Vero's OmaVero portal. This will save you considerable time during tax filings.

The practical workflow: Step-by-step finance organisation

Setting up a system is only half the work. Maintaining it consistently is what keeps your finances healthy and your compliance intact. The following workflow is grounded in guidance from the Finnish Tax Administration and reflects what professional accountants recommend for Finnish businesses.

- Collect all supporting documents. Every transaction, whether a purchase, sale, or expense, must have a supporting document. This includes invoices, receipts, bank statements, and contracts.

- Date and number each document. Each document should carry a clear date and a sequential reference number. This makes retrieval straightforward during audits or tax reviews.

- Store documents securely. Digital storage is strongly recommended. Scanned or photographed documents stored in a secure cloud system are easier to organise, search, and share with your accountant. Vero advises that supporting documents are collected and stored in a structured and accessible manner.

- Record transactions promptly. Enter each transaction into your accounting software as soon as possible. Delayed entries increase the risk of errors and omissions.

- Reconcile your accounts monthly. Compare your bookkeeping entries against your bank statements every month. Discrepancies should be investigated and resolved immediately.

- Engage a professional for oversight. Even if you handle day-to-day entries yourself, having a qualified accountant review your books periodically reduces risk and ensures compliance.

The table below compares the DIY approach with working alongside a Finnish accounting professional:

| Factor | DIY bookkeeping | Professional accountant |

|---|---|---|

| Cost | Lower upfront | Higher, but reduces risk |

| Accuracy | Depends on your knowledge | High, with specialist expertise |

| Time commitment | Significant | Minimal for the business owner |

| Compliance confidence | Variable | Consistently high |

| Audit readiness | Requires preparation | Always prepared |

Reviewing essential bookkeeping documents will help you understand exactly what Vero expects you to retain. For businesses that want professional support, exploring accounting services for SMEs is a practical next step.

Pro Tip: Set a recurring calendar reminder on the first working day of each month to reconcile your accounts. This single habit prevents the year-end scramble that many Finnish entrepreneurs dread.

Common pitfalls and expert solutions

Even with a good system in place, certain mistakes appear repeatedly among Finnish small business owners. Recognising them early means you can correct course before they cause real problems.

The most common pitfalls include:

- Mixing personal and business accounts. Using one bank account for both personal and business transactions creates confusion and makes it nearly impossible to produce accurate accounts. Open a dedicated business account as soon as you register your business.

- Missing or incomplete documents. A transaction without a supporting document is a liability. If Vero requests documentation and you cannot provide it, the expense may be disallowed, or worse, a penalty may be issued.

- Failing to reconcile regularly. Many entrepreneurs record transactions but never check them against bank statements. Unreconciled books accumulate errors over time, making year-end corrections laborious and costly.

- Cash-basis errors for tax purposes. Some business owners track income and expenses on a cash basis, meaning they record money when it is received or paid. While this feels intuitive, Finnish taxation for business operators often requires accrual-style adjustments. As Vero confirms, double-entry bookkeeping on an accruals basis is mandatory for companies and corporations, and even single-entry users must adjust for accruals at tax time.

"Design your organising system so that the numbers you rely on day-to-day align with what the tax authorities base your liability on: the books."

Understanding the different accounting methods in Finland helps you choose the right approach from the start and avoid costly corrections later.

A special note on financial years: if your financial year does not align with the calendar year, your obligations do not change. Double-entry bookkeeping remains mandatory, and you will need to ensure your financial statements and tax filings reflect the correct period. This is an area where many entrepreneurs are caught off guard, particularly in the first year of trading.

Pro Tip: If you discover a discrepancy in your records, do not attempt to correct it by simply deleting the entry. Use a correction entry with a clear note explaining the change. This maintains a clean audit trail and demonstrates good faith to Vero if your records are ever reviewed.

Verifying your records and preparing for taxes

The final phase of a well-organised financial year is verification. This is where you confirm that everything recorded is accurate, complete, and ready for VAT and income tax reporting.

Follow this checklist to prepare your records for tax season:

- Verify all entries against source documents. Every line in your accounts should correspond to a dated, numbered document. Cross-check a sample of entries to confirm accuracy.

- Reconcile all accounts with bank statements. Your bank balance and your bookkeeping balance should match. Any difference must be explained and corrected.

- Check VAT entries. Confirm that all VAT-liable transactions have been recorded correctly, and that input VAT (VAT you have paid on purchases) and output VAT (VAT you have charged on sales) are both accurately captured.

- Review deductible expenses. Ensure that all business expenses are properly documented and that personal costs have not been included in business accounts.

- Prepare for income tax reporting. Your taxable income is calculated from the result shown in your accounts. Confirm that your profit and loss statement reflects the actual performance of your business.

- Consider your financial year timing. As Vero notes, if your financial year is not the calendar year, double-entry bookkeeping is mandatory regardless of company type, and some financial statement requirements may differ based on your year-end date and the size of your business.

- File on time. Late filings attract penalties in Finland. Mark your VAT and income tax deadlines clearly in your calendar and build in preparation time.

Reviewing a dedicated compliance and success resource can help you confirm that your year-end process meets all current Finnish requirements.

A fresh perspective: What most guides miss about Finnish business finance

Most articles on business finance focus on tools: which software to use, which app to download, which spreadsheet template to follow. Tools matter, but they are not the deciding factor in whether your finances are truly organised.

In our experience working with Finnish entrepreneurs, the businesses that consistently maintain clean, compliant accounts share one thing in common: they treat bookkeeping as a regular habit, not a once-a-year event. The entrepreneurs who struggle are not necessarily less intelligent or less capable. They simply treat their accounts as something to deal with later, and "later" arrives in a panic at tax time.

We have seen businesses with sophisticated accounting software that still had chaotic records, because no one was entering data consistently. We have also seen sole traders using simple spreadsheets who had flawless records, because they updated them every single week without fail. The tool is secondary. The habit is primary.

There is also a hidden cost to poor financial separation that most guides do not address directly. When personal and business finances are mixed, it is not just a tax headache. It affects your ability to understand whether your business is actually profitable. Many entrepreneurs are surprised to discover, once accounts are properly separated, that their business was either more profitable or less profitable than they believed. That clarity is genuinely valuable, not just for tax purposes but for every decision you make about pricing, hiring, and growth.

The single habit we recommend above all others is this: spend thirty minutes every week on your accounts. Review transactions, file documents, and note anything unusual. This weekly rhythm prevents backlogs, reduces errors, and means that when tax season arrives, you are reviewing records rather than rebuilding them from scratch.

If you want to understand the full value of professional support, exploring the SME accountant benefits in the Finnish context is well worth your time.

Take your business finances to the next level

Applying the steps in this guide will put you on solid ground, but you do not have to manage everything alone. At Finovate, we work with Finnish entrepreneurs and small business owners to make financial management straightforward, compliant, and stress-free.

Whether you are a light entrepreneur needing invoicing support, a sole trader looking for reliable bookkeeping, or a growing SME that needs payroll, tax planning, and business advisory services, we have the expertise to help. Our team understands Finnish accounting requirements inside and out, so you can focus on running your business with confidence. Contact us today to find out how we can support your financial organisation from day one.

Frequently asked questions

Is single-entry bookkeeping allowed for all Finnish businesses?

Single-entry bookkeeping is only permitted in specific cases, typically for self-employed businesses operating under a business name, and you must adjust it on an accruals basis for tax purposes.

What supporting documents should Finnish businesses keep?

Businesses must retain all receipts and documents that support each transaction, and documents must be dated and numbered for proper accounting and tax compliance.

Does the financial year have to match the calendar year in Finland?

No, but if your financial year does not align with the calendar year, double-entry bookkeeping is mandatory regardless of company type, and some reporting requirements may differ.

Should I use an accountant or can I organise finances myself?

You can manage your own finances, but Vero advises arranging accounting with a qualified firm or expert accountant to ensure accuracy and full compliance.