TL;DR:

- Effective cash flow management in Finnish SMEs depends on building a practical budget that offers clear financial insights. Regularly reviewing and adjusting this budget helps prevent cash shortages and supports informed decision-making amid market fluctuations. Utilizing appropriate tools, accurate data, and scenario planning ensures sustainable growth and financial control.

Managing cash flow when revenue is unpredictable is one of the most persistent challenges facing small and medium-sized business owners in Finland. Without a clear financial plan, everyday decisions about hiring, purchasing, and investment become guesswork rather than strategy. This guide walks you through the exact steps needed to build a practical, reliable budget that gives your business genuine financial clarity. From gathering the right data to reviewing performance each quarter, you will find actionable guidance tailored specifically to Finnish SMEs at every stage of this process.

Table of Contents

- Why budgeting matters for Finnish SMEs

- Essential tools and information for successful budgeting

- Step-by-step business budgeting process for SMEs

- Monitoring, adjusting, and learning from your budget

- A fresh perspective: Avoiding the pitfalls of SME budgeting

- How Finovate can simplify your business budgeting

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Budgeting builds control | Structured budgets give SMEs clarity and confidence to plan for growth and emergencies. |

| Use modern budgeting tools | Digital solutions and scenario analysis make business budgeting faster and more reliable. |

| Adapt and update regularly | Review your budget monthly and be ready to adjust lines as conditions change. |

| Keep healthy cash reserves | Maintain savings equivalent to 3–6 months’ expenses to weather unforeseen disruptions. |

Why budgeting matters for Finnish SMEs

Many business owners associate budgeting with large corporations, compliance requirements, or accountants working in back offices. The reality is very different. A well-structured budget is one of the most powerful tools available to any SME, regardless of size or sector.

Finnish small businesses face particular pressures. Seasonal demand shifts, rising input costs, and fluctuating export conditions can all create sudden cash shortfalls. Without a budget, you are reacting to problems rather than anticipating them. With one, you gain control.

Budgeting for business growth is not simply about tracking income and expenses. It is about making deliberate, informed choices about where your resources go. This distinction matters enormously for SMEs operating with thin margins.

"Regular budgeting helps business owners track money sources and spending, monitor implementation, plan personal salary, and seek SME financial advice." Suomi.fi frames this as a core practice for preventing financial difficulties, not just managing existing ones.

The core benefits of maintaining a structured budget include:

- Visibility: You see exactly where money comes from and where it goes, month by month.

- Confidence: Decisions about hiring, investment, or cost-cutting are based on real data rather than gut feeling.

- Competitiveness: You can respond faster to market shifts because your financial position is always clear.

- Financial sustainability: Conservative revenue estimates and maintaining emergency cash reserves protect your business during downturns.

- Planning accuracy: Over time, your budget forecasts become more precise as you compare actuals against predictions.

Even a simple budget, reviewed consistently, delivers these benefits. You do not need elaborate software or a finance team to start. You need commitment and the right approach.

Essential tools and information for successful budgeting

Before you build a budget, you need the right inputs. Attempting to forecast without accurate historical data is one of the most common errors SMEs make. The preparation phase is just as important as the budgeting itself.

Start by collecting the following core data sets:

- Recent sales figures: At minimum, the last 12 months of actual revenue, broken down by product line or service category where possible.

- Fixed and variable costs: Rent, utilities, salaries, insurance, and subscriptions are fixed. Raw materials, shipping, and marketing spend tend to vary.

- Vendor contracts: Review renewal dates and any price escalation clauses that may affect your cost base.

- Payroll obligations: Include gross salaries, employer contributions, and any upcoming pay reviews.

- Tax obligations: VAT deadlines, corporate income tax prepayments, and any outstanding liabilities must be factored into cash flow planning.

Optimising your bookkeeping workflow in advance makes gathering this data much faster and less stressful. If your records are well-organised, the data collection phase takes hours rather than days.

Regarding tools, you have two practical routes. Excel-based templates work well for businesses with straightforward finances and a single revenue stream. SaaS platforms offer more automation, real-time dashboards, and multi-user access, which suits growing businesses. The key feature to prioritise in either case is scenario planning functionality. According to Ornamo's small business financial planning tool, a good SME budgeting tool allows you to input planned costs and sales, compile monthly and yearly results, track actuals versus budget, and test scenarios such as a 20% revenue drop or a 10% expense increase.

| Tool type | Best for | Key benefit | Limitation |

|---|---|---|---|

| Excel/Sheets templates | Simple businesses, single revenue stream | Low cost, full control | Manual updates, error-prone |

| SaaS budgeting platforms | Growing SMEs, multiple revenue lines | Automation, real-time data | Monthly subscription cost |

| Accountant-managed tools | Complex financials, time-poor owners | Expert oversight | Higher cost |

Understanding finance terms SMEs must know before you start, such as gross margin, operating expenses, and net cash flow, will help you use any tool more effectively. Improving workflow efficiency in budgeting also reduces the time burden significantly, letting you focus on running your business.

Pro Tip: Always verify your data sources for reliability before building a budget on them. Incorrect input figures will produce misleading forecasts, and decisions based on those forecasts can be costly. Reconcile your accounting records against bank statements at least monthly.

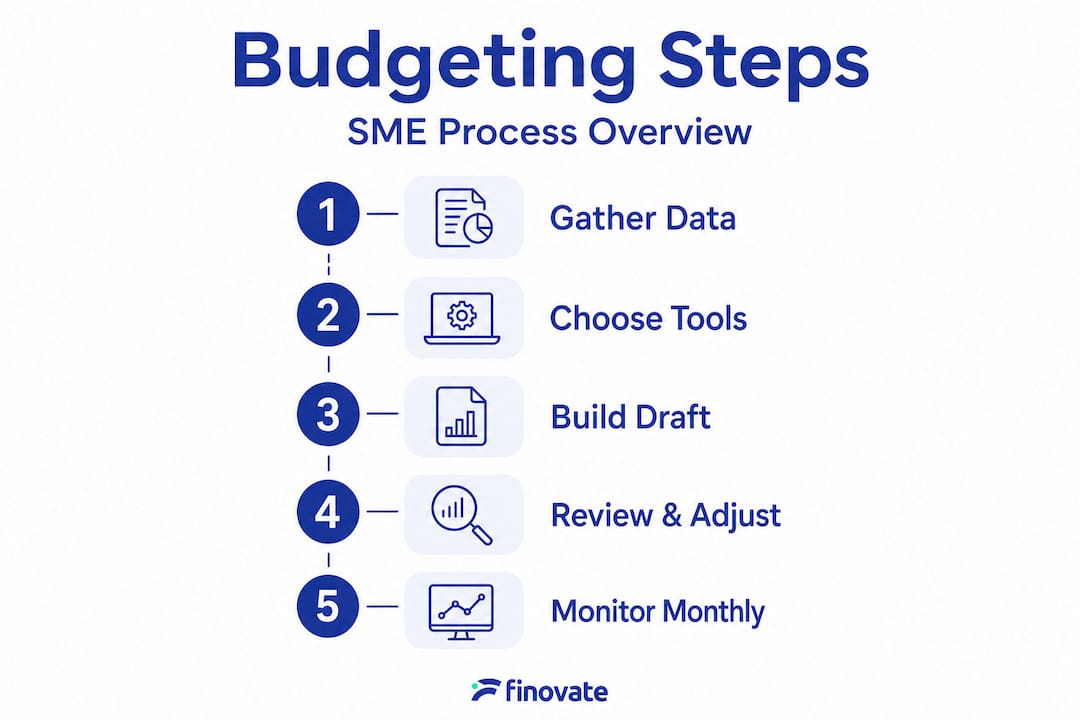

Step-by-step business budgeting process for SMEs

With your data assembled and your tools chosen, here is a clear, practical process for building and implementing a working budget for your Finnish SME.

- Gather and verify your historical data. Use the last 12 to 24 months of financials. Identify seasonal patterns, one-off costs, and any anomalies that should not be projected forward.

- Forecast your revenue conservatively. Base projections on known contracts, recurring customers, and realistic new business estimates. Avoid optimistic assumptions. If actual revenue exceeds forecasts, that is a positive surprise. The reverse is financially dangerous.

- Set your budget lines. Assign a planned spend figure to every cost category: staffing, premises, marketing, equipment, professional services, and tax. Refer to budgeting salary and payroll guidance to ensure payroll costs are calculated correctly, including all employer-side contributions.

- Build in scenario plans. Prepare at least two alternative versions of your budget: one assuming a 15 to 20% revenue shortfall, and one assuming a significant unexpected cost. This forces you to think through contingency responses before you need them.

- Review and approve the budget. If you have business partners or a management team, present the budget formally. Agreement from all decision-makers prevents conflicts later when actual spending diverges from plan.

- Implement and communicate. Share relevant budget lines with the people responsible for spending in each area. A budget that only the owner knows about cannot constrain or guide anyone else's decisions.

- Schedule reviews from day one. Monthly and quarterly review dates should be in your calendar before the budget period begins.

One strategic choice worth understanding is the difference between incremental budgeting and zero-based budgeting.

| Method | How it works | Pros for SMEs | Cons for SMEs |

|---|---|---|---|

| Incremental budgeting | Adjust last year's figures by a percentage | Fast, familiar, low effort | Perpetuates inefficiencies and outdated assumptions |

| Zero-based budgeting | Justify every expense from scratch each period | Surfaces waste, challenges assumptions | Time-intensive, requires discipline |

Zero-based budgeting requires justifying every expense anew each period. While it is most associated with large organisations, it is genuinely applicable to SMEs looking to improve cost efficiency. You do not have to apply it to every budget cycle, but using it periodically produces significant clarity.

Pro Tip: Apply zero-based budgeting at least once a year, even if you use incremental budgeting for shorter cycles. It forces a fresh look at costs you may have stopped questioning. Many SMEs discover 5 to 15% of their expenditure is difficult to justify under proper scrutiny.

If SME accounting services are part of your support structure, involve your accountant in the review of your draft budget before it is finalised. Their perspective on tax timing and cost classification can prevent planning errors. For more strategic questions, advisory services for SMEs can help you interpret what your budget is telling you about your business model. You can also consider outsourcing business processes that fall outside your core expertise, freeing resources for your primary activities.

Monitoring, adjusting, and learning from your budget

Creating a budget is an achievement, but its value depends entirely on what you do with it afterwards. A budget that sits untouched for six months is not a financial plan. It is a document. The monitoring phase is where real financial discipline pays off.

Regular monitoring of budget implementation and active financial review are central to preventing difficulties before they escalate. Suomi.fi emphasises this alongside planning your personal salary as a business owner, which is a step many Finnish SME owners overlook until cash flow becomes critical.

Your monthly review should cover:

- Actuals versus budget variance: For each budget line, calculate the difference between planned and actual figures. Any variance exceeding 10% in either direction warrants investigation.

- Cash position: Confirm your bank balance against projected cash flow. A profitable business can still face a cash crisis if receivables are slow and payables are immediate.

- Revenue tracking: Are you achieving the sales volumes and prices you projected? If not, identify whether this is a temporary issue or a structural trend requiring a budget revision.

- Cost creep: Small unplanned expenses accumulate quickly. Review whether any new recurring costs have appeared that were not in the original budget.

Experts recommend maintaining cash reserves equal to 3 to 6 months of operating expenses to manage economic uncertainties and protect against revenue interruptions. For Finnish SMEs navigating seasonal cycles or export market volatility, this guidance is particularly relevant.

Each quarter, conduct a more thorough review. Revise revenue forecasts based on year-to-date performance. Adjust budget lines where actual costs have settled at different levels than projected. Update your scenario plans if business conditions have shifted significantly.

Understanding your financial reporting requirements helps you align your internal budget reviews with the reporting obligations you already have. Your tax advisor support can also flag tax-related budget implications as the year progresses. For a broader framework, organising your finances step by step makes ongoing monitoring far more manageable.

Pro Tip: Schedule a 30-minute monthly budget review in your calendar as a recurring appointment. Treat it like a client meeting. SME owners who review their budget consistently make better hiring decisions, manage costs more tightly, and experience fewer cash flow surprises over time.

A fresh perspective: Avoiding the pitfalls of SME budgeting

Here is something most budgeting guides do not tell you directly: overengineering your budget is a real risk, and it stalls progress just as effectively as having no budget at all.

We have worked with Finnish business owners who spent weeks building elaborate financial models before launching a product, only to find that reality diverged so sharply from the model that the whole exercise had to be repeated. A budget that takes three months to build and cannot be adjusted quickly is not an asset. It is a constraint.

The practical truth is that for most SMEs, a good enough budget reviewed regularly outperforms a perfect budget reviewed rarely. Your goal is insight, not a finance department presentation.

The most common budgeting mistakes we see Finnish SMEs make, and how to avoid them:

- Overly optimistic revenue forecasts. Always apply a conservative discount to projected income, particularly for new products or customers. Aim low, exceed targets.

- Ignoring employer-side payroll costs. In Finland, employer contributions add meaningfully to your gross payroll. Forgetting them leads to systematic budget shortfalls.

- Treating the budget as fixed. A budget is a living document. Adjusting it based on new information is not failure. Refusing to adjust it when reality demands change is.

- Skipping scenario planning. When the budget is running on time, scenario plans feel unnecessary. They are most valuable precisely because they are prepared before the pressure arrives.

- Not separating business and personal finances. This is particularly common among sole traders. Mixing funds makes accurate budget tracking almost impossible.

The benefits of hiring an accountant do not lie in outsourcing your entire financial life. They lie in having a professional review the decisions that carry the most risk, such as tax structure, payroll accuracy, and year-end reporting, while you maintain ownership of day-to-day financial management. Use expert support strategically, not as a substitute for your own financial literacy.

How Finovate can simplify your business budgeting

Building a reliable budget requires clean financial records, accurate payroll data, and clear tax visibility. These are exactly the foundations we help Finnish SMEs establish at Finovate.

Whether you are a light entrepreneur managing invoicing independently or an established SME with a growing team, our services are structured to reduce the administrative burden so you can focus on what matters. Our Invoicing Service Pro supports light entrepreneurs with straightforward, professional invoicing. Our accounting for light entrepreneurs package keeps your records compliant and clearly organised. For a full view of how Finovate accounting and tax services can support your business, explore our range of solutions built specifically for the Finnish market. We are here to help you take confident financial control.

Frequently asked questions

What is the main benefit of budgeting for a small business?

Budgeting helps small businesses gain control over their finances by forecasting expenses and income, enabling smart, sustainable decision-making. Suomi.fi recommends regular budgeting to track money sources, monitor spending, and plan personal salary.

How often should a business review its budget?

SMEs should review budgets monthly and conduct a thorough revision each quarter to adapt to changes and maintain accuracy. Active financial review is a key part of preventing financial difficulties.

What is zero-based budgeting and should Finnish SMEs use it?

Zero-based budgeting requires justifying every expense in each period and can benefit SMEs by improving cost efficiency rather than carrying over assumptions from previous years. Fortune 500 companies have long used this method, and it scales effectively for smaller businesses too.

How much cash reserve is advisable for Finnish SMEs?

Experts recommend keeping reserves equal to 3 to 6 months of operating expenses to manage economic uncertainties and revenue interruptions.

Which software tools are recommended for small business budgeting?

Excel-based templates and SME-specific financial planning software both enable monthly and yearly budgeting, scenario testing, and actuals tracking. A dedicated SME budgeting tool allows you to model cost and revenue changes quickly and compare them against real outcomes.