TL;DR:

- Many Finnish SME owners are skilled in their trade but find financial language confusing and intimidating. Understanding core finance terms helps SMEs communicate better with banks, make smarter decisions, and stay in control of their business. Mastering these concepts offers a practical competitive advantage and reduces financial anxiety in everyday management.

Many Finnish SME owners are highly skilled in their trade but find financial language confusing and intimidating. Yet 18% of Finnish SMEs experienced payment-management difficulties in a recent barometer period, and a significant part of that struggle stems from not fully understanding the financial terms that govern loans, reporting, and cash flow. Finance terminology is not just for accountants. When you understand these terms yourself, you communicate more clearly with banks, make smarter decisions, and stay in control of your business. This guide explains the most important business finance terms in plain language, with Finnish equivalents and practical context throughout.

Table of Contents

- Core business finance terms every SME in Finland should know

- How financial statements reveal business health

- How financing conditions and terms affect your SME

- Applying financial terms for better SME decisions

- Why mastering finance terms sets SMEs apart in Finland

- Let Finovate simplify your business finance

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Clarify finance language | Mastering core business finance terms empowers SME owners to stay in control and communicate confidently. |

| Understand statements | Key financial statements reveal your business’s real health and support smart decisions. |

| Know loan mechanics | Repayment capacity, creditworthiness, collateral, and interest rates all affect loan terms and risk. |

| Avoid costly pitfalls | Understanding terms helps prevent misunderstandings with banks and compliance mistakes. |

| Turn terms into action | Using finance terminology when working with banks and accountants leads to better results for Finnish SMEs. |

Core business finance terms every SME in Finland should know

With the need for clarity established, let's define the finance terms that are crucial for everyday SME management. Whether you are applying for a business loan, reviewing a contract, or discussing your accounts with an adviser, the following terms will appear repeatedly.

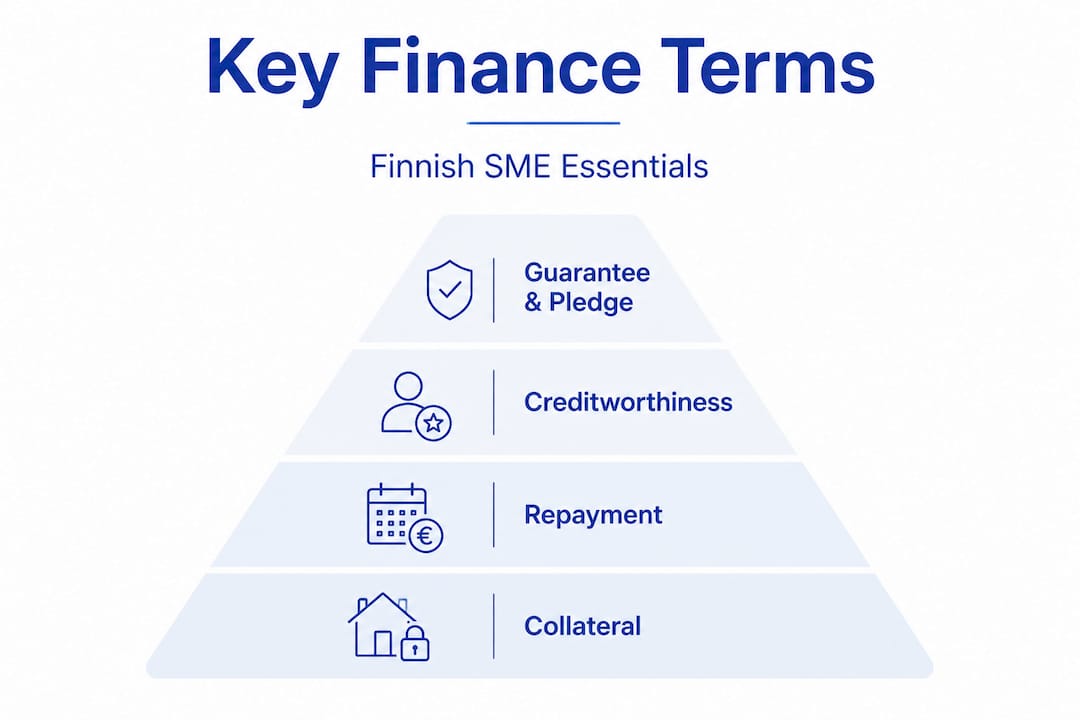

Repayment capacity (lyhennyksen maksukyky) refers to your business's ability to repay a loan from its regular income and cash flow. A bank will assess this before approving any credit. If your revenue is seasonal or unpredictable, your repayment capacity may be judged lower, even if your business is profitable overall. Understanding this term helps you present your finances in the most accurate and favourable light.

Creditworthiness (maksukykyisyys) is a broader assessment of your business's financial reliability. It takes into account payment history, outstanding debts, and overall financial stability. Banks and suppliers use creditworthiness to decide whether to extend credit and on what terms. A business with strong creditworthiness typically receives better loan conditions and more flexible payment arrangements.

Collateral security (vakuus) is an asset that you pledge to a lender to secure a loan. If you cannot repay, the lender can claim the collateral. Common examples include property, equipment, or business receivables. Finnish SME financing depends on repayment capacity, creditworthiness, and collateral, and also utilises reference rates and margins as core components of any lending agreement.

Two more terms you will encounter in loan agreements are guarantee (takuu) and pledge (pantti). A guarantee is a promise by a third party, often a business owner personally or a parent company, to repay the loan if the borrower cannot. A pledge is a specific asset formally assigned as security. Both reduce the lender's risk and can help you access financing that would otherwise be unavailable.

Key loan pricing terms

| Term | Finnish equivalent | What it means |

|---|---|---|

| Reference rate | Viitekorko | The base interest rate set externally (e.g., Euribor) |

| Margin | Marginaali | The lender's additional percentage added to the reference rate |

| Total interest | Kokonaiskorko | Reference rate plus margin combined |

| Repayment capacity | Maksukyky | Ability to repay from business income |

| Creditworthiness | Maksukykyisyys | Overall financial reliability of the borrower |

| Collateral | Vakuus | Asset pledged to secure the loan |

Understanding these terms helps you avoid expensive misunderstandings. For example, a loan advertised at a low margin might still carry a high total cost if the reference rate rises. Reviewing financial report requirements alongside your loan terms gives you a clearer picture of your obligations.

Key terms to watch in any financing agreement:

- Reference rate (viitekorko): usually Euribor at 3, 6, or 12 months, or the bank's own prime rate

- Margin (marginaali): the bank's fixed additional percentage, agreed at the time of signing

- Amortisation schedule (lyhennysohjelma): the timetable for repaying the loan principal

- Grace period (lyhennysvapaa jakso): a period during which you pay only interest, not principal

Pro Tip: Before signing any loan agreement, ask your bank to show you the total cost of credit over the full loan term, including all fees and projected interest changes. This single step can save you thousands of euros.

Familiarising yourself with Finnish accounting methods also supports your ability to interpret these figures correctly in your own financial records.

How financial statements reveal business health

Once you know the vocabulary, the next essential step is to see how these figures appear in standard financial statements. Finnish SMEs are required to produce certain financial documents, and understanding what each one reveals helps you manage your business more proactively.

Profit (voitto) is the amount left after all costs are deducted from revenue. It sounds simple, but profit appears in several forms. Gross profit is revenue minus the direct costs of goods or services. Operating profit (EBIT) deducts operating expenses as well. Net profit is what remains after taxes and interest. Each figure tells a different story about business efficiency.

Profitability (kannattavuus) measures how efficiently your business generates profit relative to its size or investment. A business can be profitable in absolute terms but still have poor profitability if it requires a disproportionate amount of capital or resources to operate. Statistics Finland's structural business and financial statement statistics include industry-specific data using profit, profitability, and balance-sheet structure, which allows you to benchmark your business against sector averages.

Balance-sheet structure (taseen rakenne) describes how your assets are financed, whether through equity, long-term debt, or short-term liabilities. A healthy balance sheet typically shows a strong equity base relative to total liabilities. Banks examine this closely when assessing loan applications.

Comparing the three core financial statements

| Statement | Finnish name | Primary purpose | Key figures |

|---|---|---|---|

| Income statement | Tuloslaskelma | Shows profit or loss over a period | Revenue, costs, operating profit, net profit |

| Balance sheet | Tase | Snapshot of assets and liabilities | Equity, debt, total assets |

| Cash flow statement | Rahavirtalaskelma | Tracks actual cash movement | Operating, investing, financing cash flows |

How to use these statements to spot strengths and weaknesses:

- Compare revenue trends across income statements from the past three years to identify growth or decline patterns.

- Check the equity ratio on the balance sheet. An equity ratio above 40% is generally considered healthy in Finland.

- Review operating cash flow on the cash flow statement. Positive operating cash flow confirms the business generates real cash, not just paper profit.

- Analyse the current ratio (current assets divided by current liabilities). A ratio above 1.0 indicates the business can cover short-term obligations.

- Benchmark against industry data using Statistics Finland's sector-specific figures to understand where you stand relative to competitors.

Pro Tip: Do not wait until year-end to review your financial statements. Reviewing them quarterly, or even monthly, allows you to catch cash flow issues before they become serious problems. Your bookkeeping basics process should support this rhythm.

How financing conditions and terms affect your SME

Understanding terms is just the beginning. It is the fine print of financing agreements that often has the biggest impact on your day-to-day cash flow and long-term risk.

Over half of Finnish SMEs do not have a bank or other lender loan, and 18% report payment-management difficulty. This means many businesses are either self-financing or relying on trade credit, which carries its own risks and terminology.

When you do take on external financing, the conditions attached to that financing directly shape your financial obligations. Collateral, guarantees, and pledges protect the lender, but they also expose you to specific risks. If you pledge personal property as collateral, a business downturn could have personal financial consequences. Understanding this distinction before signing is essential.

Important: Always clarify whether a guarantee is personal or limited. A personal guarantee means you are liable with your own assets, not just the business's. This distinction can have significant consequences if the business encounters difficulties.

Reference rates are another area where many SME owners are caught off guard. The total interest on a floating-rate loan is typically the reference rate plus the margin, but differences in reference rate resetting affect the overall cost. For example, a loan tied to 12-month Euribor resets less frequently than one tied to 3-month Euribor, which means your payments change less often but may not reflect falling rates as quickly.

Key pitfalls to avoid in loan negotiations:

- Ignoring the reset frequency of the reference rate, which determines how often your interest payments change

- Accepting a short grace period without confirming your cash flow can support full repayments once it ends

- Overlooking covenant clauses, which are conditions the bank can impose if your financial ratios fall below agreed thresholds

- Misunderstanding the pledge scope, particularly whether it covers only specific assets or all business property

- Failing to negotiate the margin, which is the one element of total interest that is fully negotiable at the time of signing

Payment conditions in supplier agreements also deserve attention. Extended payment terms from customers can create cash flow gaps, particularly for businesses with high upfront costs. Reviewing your SME bookkeeping workflow helps you track receivables and payables accurately, reducing the risk of being caught short.

Applying financial terms for better SME decisions

Having decoded the terms and their impact, let's focus on practical steps for everyday SME management. Knowing these terms is only valuable if you apply them in real situations.

Using the correct finance terms enables SME owners to negotiate better and manage business finances more effectively. This is not just about sounding knowledgeable. It is about asking the right questions and understanding the answers you receive.

Here is a step-by-step approach to preparing for a lender discussion:

- Gather your latest financial statements. Bring your income statement, balance sheet, and cash flow statement for the past two years. Be prepared to explain any significant changes.

- Calculate your key ratios. Know your equity ratio, current ratio, and net profit margin before the meeting. These are the figures the bank will examine first.

- Clarify your repayment capacity. Prepare a simple projection showing how your expected income covers the proposed loan repayments, including interest.

- Identify your collateral. Know which assets you are willing to pledge and their estimated value. Have documentation ready.

- Ask about the margin. Confirm whether the margin is fixed for the loan term or subject to review, and under what conditions it might change.

- Request a full cost illustration. Ask the bank to provide a written example of total loan costs under different reference rate scenarios.

Practical scenarios where this knowledge makes a direct difference:

- Anticipating cash flow gaps: If you know your reference rate resets in three months and Euribor has been rising, you can plan for higher payments in advance rather than being surprised.

- Responding to covenant breaches: If your equity ratio drops below the threshold agreed in your loan contract, you can approach the bank proactively rather than waiting for them to contact you.

- Reviewing supplier terms: Understanding payment conditions helps you negotiate longer payment terms with suppliers or shorter terms with customers to improve cash flow.

Pro Tip: Before any meeting with your bank or accountant, write down three specific questions using the correct terminology. This signals financial literacy and often leads to more detailed, useful responses from the other side of the table.

Staying compliant with Finnish reporting requirements is equally important. Your SME bookkeeping compliance guide and tax compliance essentials are practical references for meeting statutory obligations accurately and on time.

Why mastering finance terms sets SMEs apart in Finland

Most business advice focuses on strategy, products, or marketing. Financial literacy rarely gets the attention it deserves, yet it is one of the most practical competitive advantages available to any SME owner.

Here is what we observe consistently: SME owners who use correct financial language receive faster, clearer responses from lenders and accountants. This is not a coincidence. When you frame a question using precise terminology, the person on the other side of the conversation understands exactly what you need. There is less back-and-forth, fewer misunderstandings, and more productive outcomes.

Conventional wisdom suggests that financial terms are the accountant's domain. We disagree. An accountant can manage your books, but they cannot negotiate your loan or make your business decisions for you. The owner who understands the difference between a pledge and a guarantee, or between gross profit and operating profit, is the owner who walks into a bank meeting with genuine confidence rather than relying entirely on someone else to interpret the conversation.

There is also a subtler advantage. Lenders and advisers respond differently to business owners who demonstrate financial literacy. It signals that the business is managed thoughtfully, that risks are understood, and that obligations will be taken seriously. This perception can influence loan terms, credit limits, and the quality of advice you receive.

We also believe that finance literacy reduces anxiety. Many of the payment difficulties reported by Finnish SMEs arise not from a lack of funds but from a lack of anticipation. When you understand your loan conditions, your financial ratios, and your cash flow patterns, you can see problems forming weeks or months in advance. That lead time is often enough to take corrective action. Explore how accounting services advice can support your financial literacy journey alongside professional guidance.

Let Finovate simplify your business finance

Managing business finances in Finland requires both knowledge and reliable support. Understanding the terms is a strong foundation, but having an experienced team to handle the day-to-day detail makes a real difference to how confidently you can run your business.

At Finovate, we support Finnish SMEs with bookkeeping, financial reporting, payroll, and tax services designed to keep your finances accurate and compliant. Whether you are a light entrepreneur looking for a straightforward invoicing service or an established SME needing full accounting support, we are here to help. Visit Finovate to explore our services and find the right solution for your business. Clear finances start with the right partner.

Frequently asked questions

What is collateral security for business loans in Finland?

Collateral security is an asset pledged by the business or owner to secure a loan, reducing lender risk if repayments are missed. Collateral in Finnish SME lending includes pledged assets and guarantees as primary forms of security.

How do Finnish SMEs use reference rates and margins?

SMEs in Finland often take loans with floating reference rates plus a margin, so the total interest changes as the reference rate resets. The total interest rate is calculated as the reference rate plus the margin, and this combined figure can rise or fall over the loan term.

Why do bankers care about creditworthiness and repayment capacity?

Banks assess both to ensure the SME has the ability and track record to repay the loan, helping manage their lending risk. Banks assess repayment capacity and creditworthiness together as the foundation of any SME financing decision.

What are the most important financial statements for a Finnish SME?

Profit and loss, balance sheet, and cash flow statements show essential data about SME performance and obligations. Statistics Finland's financial statement statistics describe profit, profitability, and balance-sheet structure across industries, providing useful benchmarks.

How common are payment problems among Finnish SMEs?

18% of Finnish SMEs experienced payment-management difficulties in the latest barometer period, making it a widespread concern. 18% of Finnish SMEs reported these difficulties in the most recent Pk-yritysbarometri survey.