TL;DR:

- Many Finnish small businesses believe cash accounting is always simpler, but it involves eligibility rules and adjustments. It is suitable for sole traders with modest turnover, but larger businesses must switch to accrual bookkeeping as they grow. For tax purposes, cash-based books require adjustments to an accrual basis, and understanding these rules is essential for compliance and effective financial management.

Many Finnish small business owners assume that cash accounting is always the simpler, safer choice. On paper, it sounds straightforward: record money when it comes in and when it goes out. But the reality in Finland is more nuanced. Cash accounting comes with eligibility rules, VAT changes, and tax adjustments that can catch even careful business owners off guard. This article explains exactly who can use cash accounting in Finland, how it works day to day, and how it compares with accrual methods, so you can make an informed decision that supports both your bookkeeping and your tax obligations.

Table of Contents

- Who can use cash accounting in Finland

- How cash accounting works: process and timing

- Comparing cash and accrual accounting for Finnish small businesses

- Cash accounting and tax preparation: special rules for Finnish businesses

- The real impact: what small business owners overlook about cash accounting

- Find expert help for cash and accrual accounting in Finland

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Eligibility rules | Cash accounting is available to micro businesses and sole traders unless double-entry criteria are met. |

| Simplicity advantage | Cash accounting streamlines bookkeeping by directly reflecting actual bank transactions. |

| Tax adjustments required | Year-end tax reporting must convert cash records to accrual basis, so cash accounting alone isn't enough. |

| VAT changes | VAT relief for small businesses ended in 2025, but cash VAT can still be used. |

| Best fit for micro scale | Cash accounting is ideal for uncomplicated, small-scale operations but not for growth or complexity. |

Who can use cash accounting in Finland

Not every Finnish business is free to choose its bookkeeping method. The Finnish tax authority and accounting legislation set clear boundaries around who may use cash accounting, known in Finnish as maksuperusteinen kirjanpito, which translates loosely as single-entry bookkeeping on a payment basis.

Cash accounting is permitted for self-employed persons and business operators (toiminimi) who are not required to use double-entry bookkeeping. This typically covers sole traders and freelancers running simple operations with modest turnover and few or no employees.

The critical question is: when does a business have to switch to double-entry accrual bookkeeping? Finnish law sets out a three-part test. Double-entry accrual bookkeeping is mandatory if two of the following three criteria are met in the most recent financial year: annual turnover exceeds approximately €200,000, the balance sheet total exceeds approximately €100,000, or the average number of employees exceeds three. Additionally, if your financial year does not align with the calendar year, you must use double-entry bookkeeping regardless of size.

Key rule: Meeting just one of the three size criteria does not force a switch. You must meet two or more before double-entry bookkeeping becomes a legal requirement.

Common scenarios where cash accounting is permitted include:

- A freelance designer or consultant operating as a toiminimi with annual turnover below €200,000

- A self-employed tradesperson with no employees and a small balance sheet

- A sole trader who invoices clients irregularly and whose financial year follows the calendar year

- A light entrepreneur using an invoicing platform to manage occasional project work

If you are exploring accounting for freelancers or wondering how to select the right method from the outset, understanding these eligibility rules is the foundation. Getting clarity early prevents costly corrections later. You can also review guidance on choosing accounting methods as your business model develops.

How cash accounting works: process and timing

Once you know if you qualify, understanding the mechanics of cash accounting is the next step. The principle is straightforward: you record income when you actually receive payment, and you record expenses when you actually make payment. You do not record an invoice the moment you send or receive it.

Under single-entry cash basis bookkeeping, all entries reflect actual bank transactions, and the financial year must be the calendar year. This means your bookkeeping period runs from 1 January to 31 December with no exceptions for cash accounting users.

Here is a practical step-by-step process for managing cash accounting day to day:

- Record income on receipt. When a client payment arrives in your bank account, log it as income for that date. If a payment arrives in January for an invoice you sent in December, it is January income.

- Record expenses on payment. When you pay a supplier or purchase a business expense, record it on the date the money leaves your account.

- Keep all receipts and bank records. Every entry must be supported by a document. Bank statements, receipts, and payment confirmations are your primary evidence.

- Reconcile monthly. Cross-check your bookkeeping records against your bank statements at least once a month to catch any discrepancies early.

- Prepare a year-end summary. At the close of the calendar year, compile all recorded income and expenses into a clear summary for tax reporting.

Pro Tip: Link your business bank account directly to bookkeeping software so that transactions are imported automatically. This reduces manual data entry and minimises the risk of missed entries, which is one of the most common errors in cash basis records.

For those new to this process, reviewing bookkeeping basics gives a solid starting point. Once you are comfortable with the fundamentals, bookkeeping best practices can help you refine your approach and keep records in excellent order.

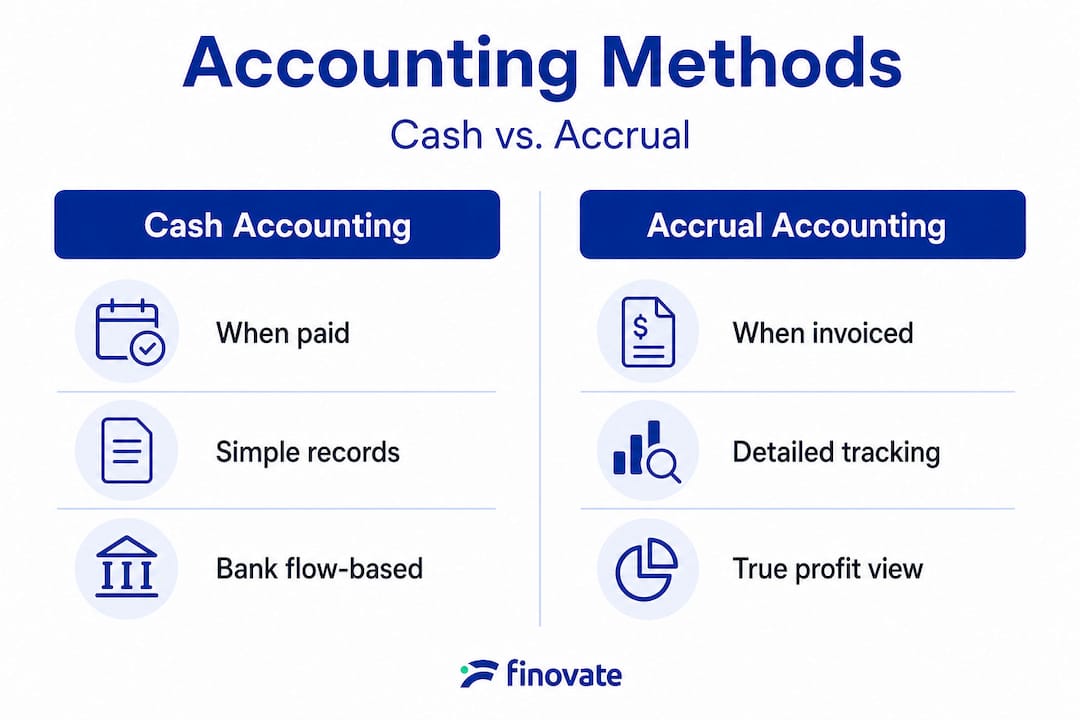

Comparing cash and accrual accounting for Finnish small businesses

With the basic mechanics laid out, it is important to understand how cash accounting measures up against its alternative: accrual bookkeeping. The two methods differ primarily in timing, and that timing difference has real consequences for your financial picture and tax position.

| Feature | Cash accounting | Accrual accounting |

|---|---|---|

| Income recorded | When payment received | When invoice issued |

| Expense recorded | When payment made | When cost incurred |

| Cash flow visibility | High | Lower without extra tools |

| Profitability view | Limited | Accurate |

| Receivables tracking | No | Yes |

| Payables tracking | No | Yes |

| Suitable for growth | Limited | Well suited |

| Regulatory compliance | Sole traders only | All business types |

| Financial year | Calendar year only | Flexible |

Cash accounting simplifies financial management for small businesses by mirroring actual bank flows, reducing administrative burden, and making it easier to track the cash available to you at any moment. This is genuinely valuable for a sole trader who wants a clear, real-time view of liquidity without complex software or significant accounting knowledge.

However, the limitations are significant: cash accounting does not provide an accurate view of profitability, it does not track receivables (money owed to you) or payables (money you owe others), and if you are required to prepare formal financial statements, those must be prepared on an accrual basis regardless.

Key advantages of cash accounting for small Finnish businesses:

- Simple record-keeping that does not require accounting expertise

- Clear connection between your books and your bank balance

- Lower cost of administration, particularly useful for sole traders

- Easier VAT management through cash VAT (maksuperusteinen ALV)

Key advantages of accrual accounting:

- Accurate picture of business profitability at any point in time

- Proper tracking of all outstanding invoices and obligations

- Better suited to securing financing or working with investors

- Required for businesses above the statutory size thresholds

Worth noting: Many businesses that start on cash accounting find that accrual methods serve them better as they grow, even before they are legally required to switch. The insight accrual bookkeeping provides is genuinely valuable for planning.

Businesses considering their options can explore accounting methods explained in more detail. Professional bookkeeping support services are also available for those who want hands-on assistance with the transition or day-to-day management.

Cash accounting and tax preparation: special rules for Finnish businesses

Comparing methods frames the bigger picture, but for most owners, tax reporting is where things get tricky with cash accounting. There is a common misconception here that needs to be addressed directly: using cash accounting for your bookkeeping does not mean your taxes are also calculated on a cash basis.

For income tax purposes, even if you keep your books on a cash basis, you must adjust your figures to an accrual basis (suoriteperuste) when preparing your tax return. This adjustment process accounts for outstanding invoices and unpaid expenses that straddle the year-end. In practice, this means year-end tax preparation for cash accounting users involves more work than many expect.

VAT rules have also changed significantly. The VAT relief scheme that previously benefited small businesses with turnover below €30,000 is no longer available: VAT relief for small businesses with turnover under €30,000 ended for VAT periods starting from 2025 onwards. Cash VAT (maksuperusteinen ALV), which allows you to declare VAT only when payments are actually received or made, remains available and is a useful tool for managing cash flow.

Here is a practical approach to year-end tax preparation for cash accounting users:

- Compile all income received during the calendar year. Include every bank receipt linked to business activity.

- Compile all expenses paid during the calendar year. Gather receipts and bank records for every business payment made.

- Identify any outstanding invoices at 31 December. These represent income earned but not yet received, which must be included in your accrual-adjusted tax figures.

- Identify any unpaid business expenses at 31 December. These represent costs incurred but not yet paid, which must also be reflected in your adjusted figures.

- Prepare the accrual adjustment. Add outstanding income and deduct unpaid expenses to arrive at the taxable income figure required by the Finnish Tax Administration.

- File your tax return accurately and on time. Errors in the accrual adjustment are a frequent source of tax discrepancies for sole traders using cash accounting.

Pro Tip: Keep a simple spreadsheet of all open invoices and unpaid bills as at 31 December each year. This makes the accrual adjustment straightforward and significantly reduces the risk of errors in your tax filing.

For more detailed guidance, our tax tips for entrepreneurs cover the most common pitfalls. You can also review accounting rules in Finland for the broader regulatory context, and our tax preparation guide provides step-by-step support. The small business tax guide is also a useful reference for owners navigating Finnish tax obligations for the first time.

The real impact: what small business owners overlook about cash accounting

Having covered the tax and compliance details, let us look at what most articles and advisors miss about cash accounting for Finnish small businesses. The honest truth is that cash accounting is often sold as a universal solution for simplicity, but it is more accurate to describe it as a starting point rather than a long-term strategy.

Cash accounting genuinely works well for micro sole traders with very simple, predictable cash flows. If you invoice one or two clients a month and pay a small number of regular expenses, the administrative ease is real and worthwhile. Cash accounting's primary role for Finnish small business owners is simplifying day-to-day bookkeeping and VAT timing to improve cash flow management. However, even in this context, the requirement to adjust to accrual basis for income tax limits the full tax deferral benefits that business owners often hope for.

The hidden risk that we see most often is this: business owners who rely solely on cash records lose visibility into their true financial position. Without tracking receivables and payables, you may feel cash-rich in January only to discover that three large supplier invoices are due in February and two major client invoices are still unpaid. This is not a bookkeeping technicality. It is a business blind spot that can lead to genuine cash flow crises.

Growth is the other trigger that catches owners off guard. Switching to accrual accounting becomes both legally necessary and practically beneficial once your business starts to scale. The sooner you build accrual-ready records and financial habits, the smoother that transition will be. Waiting until you are legally required to switch often means a disorganised handover and a higher risk of compliance errors.

Our view, based on working with Finnish entrepreneurs across a wide range of sectors and sizes, is this: cash accounting is a legitimate and useful tool for eligible businesses, but it should be managed with a clear understanding of its limits. Use it while it serves you, but plan the transition before it becomes a problem.

Find expert help for cash and accrual accounting in Finland

To round off, here is how you can get the guidance and support you need for cash accounting, tax, and compliance in Finland.

Managing bookkeeping, VAT reporting, and year-end tax adjustments on your own is entirely possible, but the rules are detailed and the consequences of errors can be costly. Whether you are just starting out as a sole trader or reaching the point where switching to accrual accounting makes sense, professional support makes the process significantly easier.

At Finovate, we provide bookkeeping, tax preparation, payroll processing, and business advisory services tailored specifically for Finnish small businesses and entrepreneurs. We also offer a dedicated accounting service for light entrepreneurs, designed to keep your finances compliant and well-organised without the overhead of a full accounting department. Get in touch with us to find out which service best fits your current situation and growth plans.

Frequently asked questions

Which Finnish businesses are allowed to use cash accounting?

Self-employed persons, toiminimi and sole traders with simple cash flows who do not meet the two-of-three size criteria for double-entry bookkeeping are permitted to use cash accounting in Finland.

Is cash accounting enough for Finnish tax reporting?

No. Income tax statements require adjustment to an accrual basis (suoriteperuste) even if you maintain your books on a cash basis throughout the year.

Can I use cash accounting if my business grows?

Once you meet two of the three statutory thresholds, double-entry accrual bookkeeping becomes mandatory, covering turnover, balance sheet total, and average employee count.

What are the main advantages and disadvantages of cash accounting?

Cash accounting simplifies management and mirrors actual bank flows, but it does not provide a reliable profitability view and lacks tracking for receivables and payables, making it unsuitable for growing businesses.

Has VAT relief changed for small businesses using cash accounting?

Yes. VAT relief for turnover under €30,000 ended for VAT periods starting from 2025 onwards, though cash VAT (maksuperusteinen ALV) remains available for eligible businesses.