TL;DR:

- In Finland, an accounting period is the specific timeframe covered by your company's financial statements, typically lasting 12 months but flexible based on your bookkeeping method. The chosen period directly affects tax deadlines, VAT reporting, and compliance with Trade Register registration, making it a strategic business decision. Changes to the period require careful registration updates and alignment across financial and tax reporting to avoid penalties and ensure smooth operations.

Many Finnish business owners use the terms "accounting period", "financial year", and "tax period" interchangeably, but each carries specific legal meaning. Confusing them can lead to filing errors, missed deadlines, and even registration problems with the Finnish Trade Register. If you are setting up a new company, changing your bookkeeping method, or simply trying to get your compliance house in order, understanding exactly what an accounting period is and how it shapes your obligations is one of the most practical steps you can take. This article walks you through everything you need to know.

Table of Contents

- What is an accounting period?

- The Finnish approach: financial year, tax period, and compliance

- Single-entry vs double-entry: how bookkeeping method affects your accounting period

- Changing your accounting period: registration and reporting considerations

- The accounting period and your SME tax obligations

- Why the right accounting period strategy could save your SME time and stress

- Get expert support for stress-free accounting periods

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Accounting period meaning | The accounting period is the defined time span covered by a company’s financial statements and is crucial for compliance. |

| Compliance ties | Your chosen accounting period dictates when tax filings and statutory reports are due in Finland. |

| Method matters | Single-entry and double-entry bookkeeping have different rules for setting your accounting period. |

| Registration match | Your financial statements’ period must always match what’s registered with the Trade Register. |

| Plan for deadlines | Knowing and managing your accounting period helps you avoid missed tax and reporting deadlines. |

What is an accounting period?

At its simplest, an accounting period is the specific timeframe your company's financial statements cover. It is the reporting window used to prepare your income statement, balance sheet, cash flow statement, notes, and changes in equity. IAS 1 Presentation of Financial Statements confirms that an accounting period is the time span that the entity's financial statements cover, forming the foundation of all financial reporting.

For most Finnish SMEs, the accounting period lasts 12 months. However, it does not have to begin on 1 January. You might run a period from 1 July to 30 June, for instance, if that better reflects your business cycle. What matters is consistency: once chosen and registered, your period becomes the anchor for every financial document you produce.

It is worth distinguishing three terms that often get muddled:

- Accounting period: The time span covered by your financial statements. This is the formal, legal window for reporting.

- Financial year: In Finland, this is used almost synonymously with accounting period. It is the period registered with the Trade Register.

- Tax period: The timeframe relevant to a specific tax obligation, such as VAT or income tax. Your tax periods are derived from your accounting period.

Understanding these essential accounting rules is not just about ticking boxes. It has a direct bearing on how you analyse your business performance, compare results year on year, and satisfy auditors or investors.

Key principle: Your accounting period is the backbone of your entire financial reporting structure. Every statutory document, tax filing, and audit trail links back to this defined window of time.

The practical documents tied to your accounting period include your annual accounts, tax return, VAT reconciliation, and payroll summary. Choosing your accounting method will also depend on this period, as different methods carry different rules for recognising income and expenses within the timeframe.

The Finnish approach: financial year, tax period, and compliance

Finland's tax authority, Vero, is clear on how accounting periods and tax obligations relate. Financial year and tax period guidance confirms that the terms "financial year" and "tax period" are tied to when accounts are kept and when tax returns are filed, with taxes based directly on the books. This means that how you define your accounting period has an immediate knock-on effect on your VAT reporting cycle and your income tax filing deadline.

For Finnish SMEs, the accounting period determines when statutory financial statements examples must be drawn up, and therefore when tax return filing deadlines begin to count. Vero confirms this: tax return deadlines start counting from the end of your accounting period, not from the calendar year-end.

To illustrate how your choice of accounting period can affect your tax deadline timing, see the table below:

| Accounting period end date | Income tax return deadline (4 months) | VAT annual summary due |

|---|---|---|

| 31 December | 30 April | February following period end |

| 31 March | 31 July | May following period end |

| 30 June | 31 October | August following period end |

| 30 September | 31 January | November following period end |

As you can see, a period ending in June pushes your income tax return to October, which gives you more breathing room if your business is busiest in the spring. A period ending in December means a spring filing deadline, which can coincide with other administrative pressures.

Understanding the financial report requirements for your chosen period end date is therefore a strategic consideration, not just an administrative one.

Pro Tip: Align your accounting period end date with your quietest business month. Closing accounts and filing returns is far smoother when your team is not managing peak trading at the same time.

The period registered with the Trade Register is the legal reference point. If your financial statements do not match the registered period, you risk compliance breaches and potential penalties. This is a point we return to in more detail in the section on changing your period.

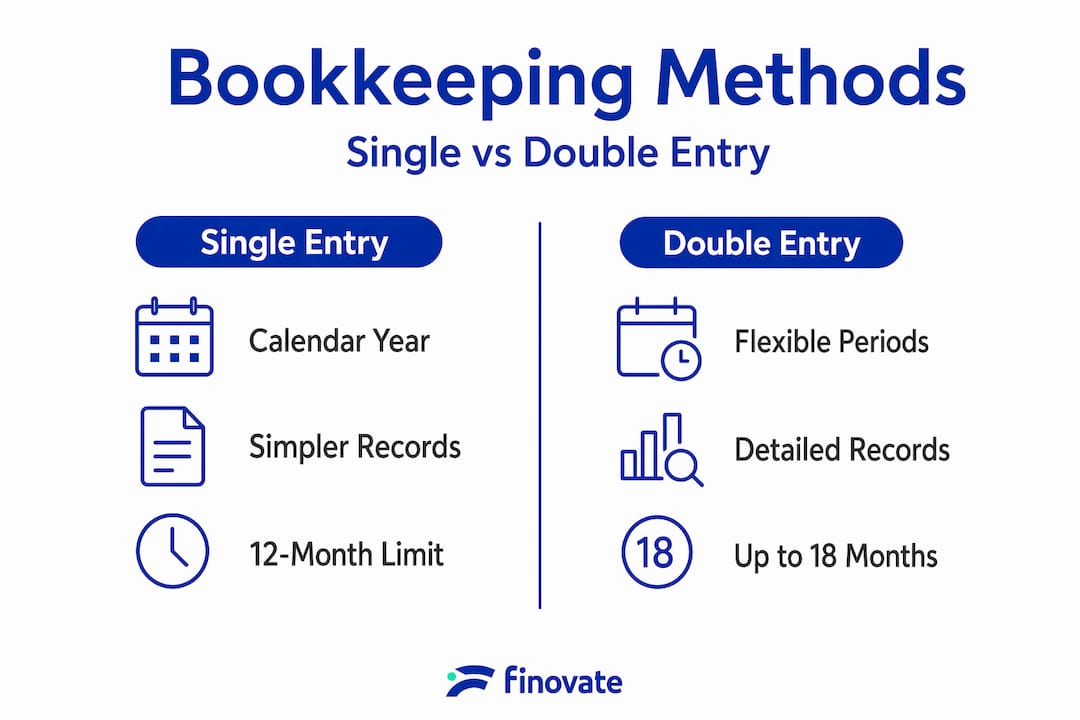

Single-entry vs double-entry: how bookkeeping method affects your accounting period

The bookkeeping method you use places direct constraints on what accounting period you can have. This is where many new Finnish business owners are caught out, so it is worth being precise.

Vero confirms that for Finnish businesses: if you use single-entry bookkeeping, your financial year must always be the calendar year (1 January to 31 December), with a maximum length of 12 months. If you use double-entry bookkeeping, you can choose a 12-month period other than the calendar year, and your first financial year can extend up to 18 months.

| Feature | Single-entry bookkeeping | Double-entry bookkeeping |

|---|---|---|

| Permitted period | Calendar year only | Any 12-month period |

| Maximum first period | 12 months | 18 months |

| Period flexibility | None | High |

| Typical users | Sole traders, very small firms | Limited companies, growing SMEs |

| Period change allowed | Limited | Yes, with registration |

This distinction matters enormously for new businesses. A company that starts trading in April using double-entry bookkeeping can choose a period running from April to March, aligning with its natural business year. A sole trader using single-entry is locked to the January to December cycle regardless of when they started.

Before setting or changing your accounting period, check the following:

- Which bookkeeping method are you currently using? Single-entry limits your options entirely.

- Is your chosen period registered correctly with the Trade Register? Mismatches cause compliance failures.

- Does your period end align with your business's quiet season? This makes year-end work less stressful.

- Have you checked the impact on VAT reporting cycles? Your VAT obligations follow your accounting period.

- Has your accountant confirmed the change is permissible? An expert review prevents costly errors.

Good bookkeeping documents for SMEs must be structured around your chosen period. Keeping thorough records from day one, following bookkeeping best practices, and following a clear Finnish bookkeeping step-by-step process will save significant time when period-end arrives.

Pro Tip: Switching from single-entry to double-entry bookkeeping? Confirm the change with both your accountant and the Finnish Tax Administration before you act. Making the switch mid-year without proper notification can result in non-compliance and potential penalties.

Changing your accounting period: registration and reporting considerations

There are legitimate reasons to change your accounting period. You might be merging with another company that uses a different cycle. You might want to align with an international parent company. You might simply realise that your current period end creates unnecessary pressure at a busy time of year.

Whatever the reason, changing your accounting period in Finland involves specific compliance steps. The PRH Financial Statements guidance is explicit: if you change your accounting period, the financial period in your financial statements must match the financial period registered for your company in the Finnish Trade Register.

Compliance warning: Filing financial statements for a period that does not match your Trade Register entry is a formal error. It can trigger queries from the Trade Register, delay filings, and potentially expose your company to penalties. Always update your registration before preparing statements for the new period.

Here is what you must do when changing your accounting period:

- Decide on the new period dates and confirm they are permissible under your bookkeeping method.

- Notify the Finnish Trade Register and submit the required change notification. This must be done before the new period begins.

- Inform your accountant so all records, software settings, and reporting templates are updated.

- Notify the Finnish Tax Administration (Vero) to ensure your tax filing deadlines are recalculated correctly.

- Update any internal financial systems including payroll, invoicing, and management accounts to reflect the new period.

- Prepare a transitional period financial statement if the change creates a period shorter or longer than 12 months.

- Check that all future financial statements reference the new registered period consistently.

Common pitfalls include preparing statements for the old period while operating under the new one, and failing to update Vero's records so that tax reminders and deadlines remain incorrectly timed. A good bookkeeping compliance guide will walk you through these steps in detail and help you avoid the most common mistakes.

The accounting period and your SME tax obligations

Your accounting period end date is one of the most important dates in your business calendar. Every major tax obligation is timed around it.

Vero's tax handbook states that a limited liability company must file its income tax return within 4 months from the end of the last calendar month of its accounting period. This is a statutory requirement, and missing it can result in a late-filing penalty. For a company with a period ending 31 December, that means filing by 30 April. For a period ending 30 June, the deadline shifts to 31 October.

Key tax events directly tied to your accounting period include:

- Income tax return deadline: 4 months after the period end for limited companies.

- Annual financial statements: Must be finalised and submitted in line with the period registered with the Trade Register.

- VAT reporting: Monthly or quarterly VAT returns follow the period, with an annual VAT summary required after period end.

- Corporate tax prepayments: Calculated and timed based on the accounting period's projected income.

- Payroll and employer contributions: Annual summaries align with the period end.

The 4-month income tax filing window is firm. Many SMEs only think about this deadline when it is already approaching, which leaves insufficient time to prepare accurate accounts. The better approach is to set calendar reminders at period-end, at the 2-month mark, and at the 3-month mark, so nothing catches you by surprise.

Partnering with specialists who understand accounting services for SMEs ensures that your tax obligations are tracked continuously, not just in the final weeks before a deadline.

Why the right accounting period strategy could save your SME time and stress

Most business owners treat the accounting period as a bureaucratic formality: something to register once and forget about. In our experience working with Finnish SMEs, this attitude is one of the most common sources of avoidable stress.

Choosing the right period from the outset is a strategic decision. An SME in the retail sector with peak trading in November and December will struggle to prepare accurate year-end accounts if its period closes on 31 December. The numbers are still moving. Staff are exhausted. A period ending in February, by contrast, captures the full season cleanly and gives the team time to close properly.

Similarly, a construction company with project cycles that run April to March may find a calendar-year period creates artificial splits in project profitability. Adjusting to match the project cycle gives management accounts that actually reflect reality.

The compliance case for revisiting your accounting rules perspective is equally strong. SMEs that consult early, ideally before their first period closes, minimise administrative missteps and avoid the costly process of correcting mismatches later. Getting it right from year one is far cheaper than rectifying errors in year three.

We also see that SMEs aligned with business growth milestones benefit from period-end reviews that coincide with natural planning windows. If your business reviews strategy in September, a period ending in August gives you fresh, finalised accounts to inform those decisions.

The accounting period is not just a compliance requirement. It is a management tool. Treated strategically, it gives you cleaner data, calmer year-ends, and a stronger platform for growth.

Get expert support for stress-free accounting periods

Setting up, managing, or changing your accounting period involves more than a simple form. The compliance requirements, bookkeeping constraints, and tax deadline implications all need careful handling.

We work with Finnish SMEs at every stage, from initial registration to annual reporting and period changes. Whether you are a new entrepreneur choosing your first accounting period or an established company looking to realign your financial year, our team can help you get it right. Explore our accounting solutions for entrepreneurs or visit our main site to learn about the full range of accounting and tax services we offer. We take the complexity off your hands so you can focus on running your business with confidence.

Frequently asked questions

What is the difference between an accounting period and a financial year in Finland?

In Finland, these terms mean essentially the same thing: the official time period your financial statements and tax filings cover, and both must match your Trade Register entry.

How long can the first accounting period be for a new Finnish business?

The first period can be up to 18 months for businesses using double-entry bookkeeping, but is capped at 12 months for those using single-entry bookkeeping, which must also follow the calendar year.

What happens if I change my company's accounting period?

You must update your registration with the Trade Register and ensure your financial statements reflect the new period, as the registered period and the period shown in your financial statements must always match.

When do Finnish SMEs have to file income tax returns after their accounting period ends?

Limited companies must file their income tax return within 4 months from the end of the last calendar month of their accounting period, making it critical to know your exact period-end date.

Can I align my accounting period with a different business cycle, not the calendar year, in Finland?

Yes. Double-entry bookkeeping allows you to choose any 12-month period, giving you the flexibility to align your financial year with your business's natural trading cycle rather than the calendar year.