TL;DR:

- Auditing financial statements confirms a company's financial accuracy and builds trust with stakeholders. It helps detect fraud, lowers borrowing costs, ensures regulatory compliance, and supports strategic decisions. Proper preparation enhances audit efficiency and strengthens a business’s financial credibility annually.

Auditing financial statements is the independent, evidence-based examination of a company's financial records to confirm they present a true and fair view of its financial position. The process follows established frameworks such as the International Financial Reporting Standards (IFRS) and produces an auditor's opinion that stakeholders rely on for decisions. For Finnish business owners, understanding why audit financial statements matter goes well beyond satisfying a legal requirement. Audits build credibility, reduce risk, and open doors to better financing. This guide explains the core benefits, clears up common misconceptions, and gives you practical steps to get the most from the process.

What are the primary benefits of auditing financial statements?

Financial audits deliver measurable, concrete advantages that affect your bottom line directly.

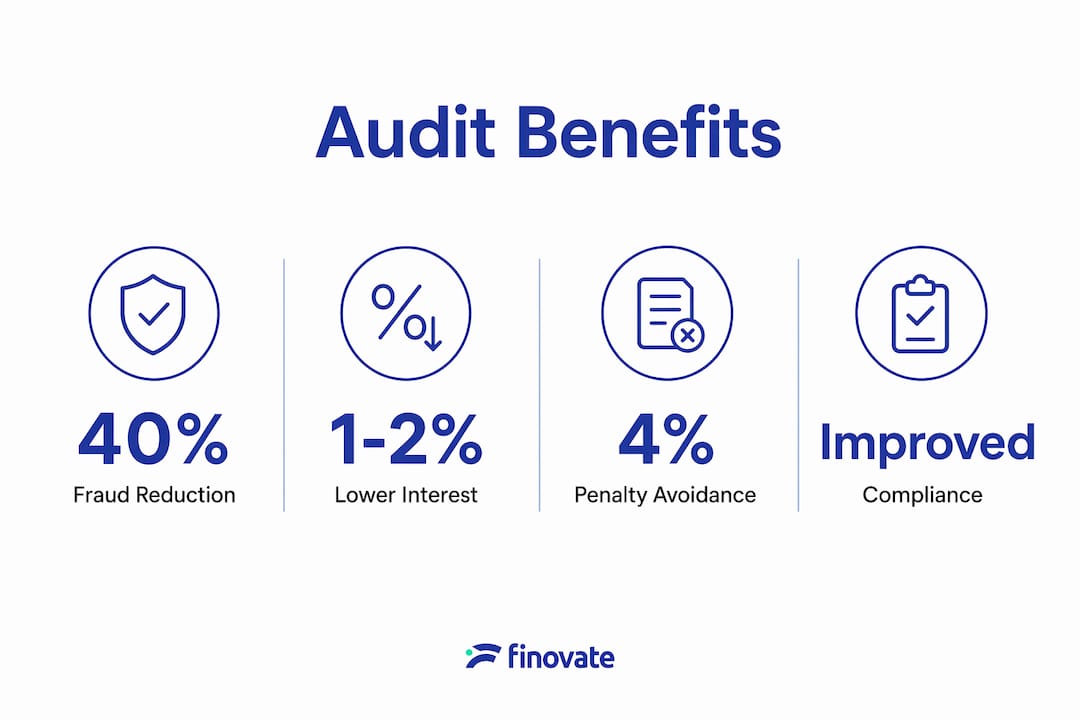

Fraud detection and loss reduction

The Association of Certified Fraud Examiners reports that audits identify 34% of workplace fraud cases and reduce average fraud losses by 40% for organisations with regular annual audits. That figure means a business turning over €500,000 a year could save tens of thousands in fraud-related losses simply by committing to an annual audit cycle.

Lower borrowing costs

Clean, audited financial statements can reduce borrowing interest rates by 1–2% on average because lenders gain confidence in the numbers. On a €200,000 business loan, that saving compounds significantly over a five-year term.

Regulatory compliance and penalty avoidance

Non-compliance with reporting regulations can lead to fines up to 4% of an organisation's annual global revenue under 2026 EU guidance. For Finnish businesses operating within the EU regulatory environment, that exposure is real and avoidable through consistent, audited reporting.

Better strategic decisions

Reliable financial data is the foundation of sound business decisions. When your figures have been independently verified, you can plan hiring, investment, and expansion with confidence rather than guesswork.

- Audits confirm revenue recognition is accurate and consistent.

- They verify that liabilities are fully disclosed, not hidden.

- They highlight areas where internal controls are weak before those weaknesses become costly.

- They produce a management letter with specific recommendations your team can act on immediately.

Pro Tip: Request a copy of the management letter at the end of every audit. It often contains the most practical, specific advice your business will receive all year.

How does auditing financial statements support compliance and reduce business risk?

Compliance is not a single event. It is an ongoing discipline, and audits are the mechanism that keeps that discipline in place.

Finnish companies must comply with the Finnish Accounting Act, and those operating across borders must also meet EU financial reporting standards. An audit verifies that your financial statements align with these requirements. It also confirms that your accounting policies are applied consistently from one period to the next. Consistency matters because it makes your figures comparable, which is exactly what banks, investors, and tax authorities need to see.

Beyond compliance, audits reduce operational and reputational risk in four specific ways:

- Risk identification. Auditors examine your internal controls and flag gaps that could expose the business to fraud or error. Addressing those gaps early is far less costly than dealing with the consequences later.

- Reporting consistency. The audit process enforces discipline around bookkeeping, reconciliations, and documentation. That discipline carries over into daily financial management throughout the year.

- Regulatory protection. A clean audit opinion is evidence of good governance. If a regulator or tax authority ever questions your reporting, audited statements are your strongest defence.

- Reputational assurance. High-quality audits prevent risks from being buried within financial reporting and maintain confidence for employees, customers, and investors alike.

Reviewing your accounting compliance practices alongside your audit cycle is the most effective way to close gaps before an auditor finds them.

Pro Tip: Share your auditor's risk findings with your management team, not just your accountant. The people running daily operations are often best placed to fix the control weaknesses auditors identify.

What common myths and misconceptions surround auditing financial statements?

The most persistent myth is that audits are only for companies in trouble. The reality is the opposite. Well-executed audits help SMEs identify inefficiencies and improve operations, making them a tool for growth rather than a sign of distress.

A second misconception is that an audit's sole purpose is to catch mistakes. Audits provide reasonable assurance, not a guarantee that every error has been found. The auditor's role is to assess whether the financial statements, taken as a whole, are free from material misstatement. That distinction matters because it sets realistic expectations and prevents disappointment when minor errors surface after the audit closes.

A third myth is that voluntary audits are a waste of money for small businesses. Voluntary audits signal company maturity to suppliers and banks, enabling better trade credit terms and lower interest rates. The cost of the audit is often recovered through the financing benefits alone.

Consider what audits actually deliver beyond the formal report:

- A structured review of your financial processes that highlights inefficiencies.

- Independent confirmation that your accounts are reliable, which you can share with partners and lenders.

- A management letter containing specific, practical recommendations on internal controls.

- A stronger position in any due diligence process, whether for investment, a merger, or a bank facility.

The strategic value of financial statements for entrepreneurs is often underestimated. Audited statements are not just a compliance document. They are a business asset.

How does the audit process work in practice?

Understanding the audit process removes the anxiety that many business owners associate with it. A standard statutory audit moves through four stages.

Planning

The auditor assesses your business, its risks, and its accounting policies. They identify areas requiring closer examination and agree on the scope of work with management.

Evidence gathering

Auditors test transactions, verify balances, and review supporting documentation. They apply professional scepticism throughout, meaning they do not simply accept management's assertions without independent evidence.

Opinion formulation

The auditor evaluates all findings and forms a view on whether the financial statements present a true and fair position.

Reporting

The auditor issues a formal opinion and, separately, a management letter. The four types of audit opinion are:

| Opinion type | What it means |

|---|---|

| Unqualified | Financial statements are clean and reliable |

| Qualified | Minor issues exist but statements are broadly reliable |

| Adverse | Statements are materially misstated and unreliable |

| Disclaimer | Insufficient evidence to form an opinion |

An unqualified opinion is the outcome most businesses receive when their records are well maintained. Auditor independence and professional scepticism are non-negotiable throughout this process. Without them, the opinion carries no credibility.

Pro Tip: Ask your auditor to walk you through their planning findings before fieldwork begins. Understanding what they intend to focus on lets you prepare documentation in advance and reduces delays.

What practical steps can Finnish business owners take before an audit?

Preparation determines how smoothly an audit runs and how much value you extract from it.

- Maintain clean records year-round. Regular bookkeeping is the single most effective way to reduce audit time and cost. Reconcile bank accounts monthly, keep receipts organised, and resolve discrepancies as they arise rather than leaving them for year-end.

- Understand what auditors need. Prepare a schedule of your key accounting policies, a list of significant transactions during the year, and supporting documentation for material balances. Having these ready before fieldwork begins saves time on both sides.

- Select a qualified auditor. In Finland, statutory auditors must hold a KHT or HT qualification. Verify your auditor's credentials and confirm they have experience in your industry sector.

- Use findings to improve controls. The management letter is not a criticism. Treat each recommendation as a free consultancy point. Implement the suggestions before the next audit cycle begins.

- Leverage audited statements actively. Audit readiness reduces due diligence time in fundraising or exits by weeks because data is independently verified and organised. Share your audited statements proactively with banks, investors, and key suppliers.

The discipline that develops through regular audits, including better bookkeeping, timely reconciliations, and consistent accounting estimates, compounds over time. Businesses that treat audits as an annual discipline rather than a one-off event build stronger financial foundations year on year.

For Finnish SMEs navigating the audit process for the first time, the practical guide to auditing for SMEs covers the statutory requirements and preparation steps in detail.

Key takeaways

Auditing financial statements delivers measurable benefits across fraud prevention, regulatory compliance, financing terms, and strategic decision-making, making it one of the highest-return investments a Finnish business owner can make.

| Point | Details |

|---|---|

| Fraud prevention | Annual audits reduce average fraud losses by 40%, protecting business assets directly. |

| Lower borrowing costs | Audited statements reduce interest rates by 1–2% on average, saving money on every loan. |

| Regulatory protection | Clean audit opinions protect against EU fines that can reach 4% of annual global revenue. |

| Operational discipline | The audit process builds better bookkeeping habits and internal controls throughout the year. |

| Strategic asset | Audited statements accelerate due diligence, improve credit terms, and support growth decisions. |

The audit mindset that separates growing businesses from stagnant ones

I have worked with Finnish business owners who dread the audit season and others who actively look forward to it. The difference is not the size of the business or the complexity of the accounts. The difference is mindset.

The owners who dread audits tend to see them as an inspection. They feel exposed, defensive, and relieved when it is over. The owners who look forward to audits treat them as a structured opportunity to get an independent view of their business. They ask questions, engage with the management letter, and implement the recommendations before the next cycle begins.

Independent assurance from audits supports governance and market integrity, making it easier to secure funding and make strategic decisions. That is not a theoretical benefit. I have seen Finnish SMEs use a clean audit opinion to negotiate better loan terms within weeks of the report being issued.

The businesses that grow consistently are the ones that treat financial discipline as a competitive advantage, not a compliance burden. An audit is the clearest signal you can send to banks, investors, and partners that your business is run with rigour and transparency. That signal has real commercial value, and it compounds every year you maintain it.

— Busayo

How Finovate supports Finnish businesses with audit-ready finances

Preparing for an audit is far easier when your financial records are accurate, up to date, and well organised throughout the year.

Finovate provides bookkeeping, tax preparation, and financial management services tailored for Finnish business owners and entrepreneurs. We keep your accounts in order so that when your auditor arrives, the groundwork is already done. Our team understands Finnish accounting regulations and the EU compliance environment, which means we help you avoid the gaps that auditors flag most often. Whether you are preparing for your first statutory audit or looking to strengthen your financial controls, Finovate is ready to support you. Get in touch to discuss how we can help your business stay audit-ready all year round.

FAQ

Why audit financial statements if my business is small?

Audits are not reserved for large companies. Small businesses benefit from fraud detection, lower borrowing costs, and stronger credibility with banks and suppliers, regardless of turnover.

What is the difference between a statutory and a voluntary audit?

A statutory audit is legally required under Finnish law for companies meeting certain size thresholds. A voluntary audit is chosen by the business owner to gain the same credibility and assurance benefits without a legal obligation.

What does an unqualified audit opinion mean?

An unqualified opinion means the auditor found no material misstatements and the financial statements present a true and fair view of the company's financial position.

How long does a financial audit typically take?

The duration depends on the size and complexity of the business. A well-prepared SME with clean records can expect the fieldwork phase to take a few days to two weeks.

Can audited financial statements help me secure a bank loan in Finland?

Yes. Audited statements give lenders independent confirmation of your financial position, which reduces their risk assessment and can result in lower interest rates and better loan terms.