TL;DR:

- Financial statements provide entrepreneurs with a comprehensive view of their business's financial health, performance, and cash flows.

- Regularly reviewing all four key statements helps identify cash flow issues, cost trends, and supports better decision-making.

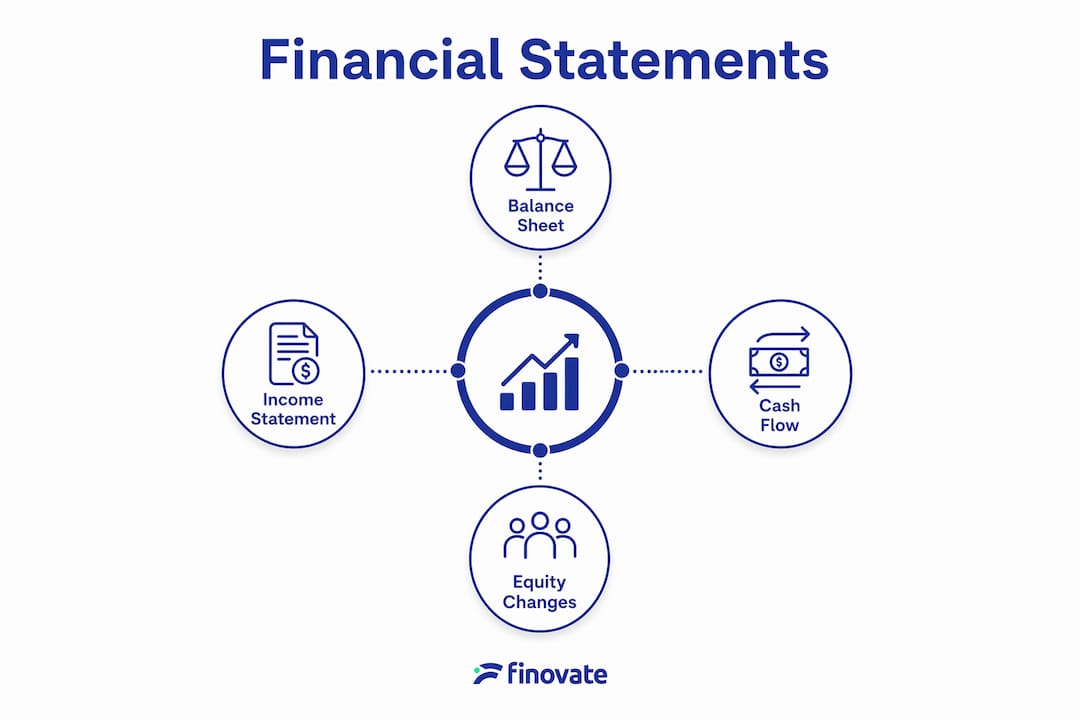

Financial statements are structured records that capture a business's financial performance, position, and cash flows, giving entrepreneurs the clearest possible picture of where their business stands. The role of financial statements goes far beyond satisfying an accountant's checklist. These documents, specifically the balance sheet, income statement, cash flow statement, and statement of changes in equity, are the primary tools through which you understand whether your business is genuinely healthy or simply appearing to be. For any entrepreneur or small business owner in Finland, reading and acting on these statements regularly is one of the most direct routes to better financial management and long-term stability.

What are the types of financial statements and their roles?

The four primary financial statements provide a comprehensive view of a company's financial health, and each one captures a different dimension of your business. Relying on only one gives you an incomplete picture, much like trying to assess your physical health from a single test result. Together, they form a complete financial portrait.

The balance sheet

The balance sheet shows what your business owns, what it owes, and what remains for the owners at a specific point in time. Assets sit on one side; liabilities and equity on the other. For a small business owner, this statement answers a direct question: if the business stopped trading today, what would be left?

The income statement

The income statement, sometimes called the profit and loss account, measures revenue, expenses, and net profit or loss over a defined period, typically a month, quarter, or financial year. It tells you whether your core operations are generating value. A business can show strong revenue on this statement while still facing serious financial difficulty, which is precisely why the income statement alone is never sufficient.

The cash flow statement

The cash flow statement tracks actual cash moving in and out of the business. Profit on paper differs from actual cash liquidity, and businesses may be profitable yet insolvent without sufficient liquidity. This statement is the one most commonly overlooked by entrepreneurs, yet it is often the first to signal a crisis.

The statement of changes in equity

This statement records movements in the owners' equity over a period, including retained profits, drawings, and any new capital introduced. It connects the income statement to the balance sheet and is particularly relevant when you have multiple shareholders or are planning to bring in investors.

Pro Tip: Review all four statements together at the end of each month, not just the income statement. The cash flow statement and balance sheet will often reveal pressures that your profit figures conceal.

| Statement | Primary focus | Key question answered |

|---|---|---|

| Balance sheet | Financial position at a point in time | What does the business own and owe? |

| Income statement | Profit or loss over a period | Is the business generating profit from operations? |

| Cash flow statement | Cash inflows and outflows | Does the business have enough cash to operate? |

| Statement of changes in equity | Movements in ownership equity | How has the owners' stake changed over the period? |

How do financial statements help entrepreneurs make better decisions?

Financial statements and decision making are inseparable for any business owner who wants to manage proactively rather than reactively. Regular review of financial statements reveals trends and cash flow cycles that a bank balance alone will never show. A bank balance tells you what is there right now. Financial statements tell you why it is there and what is likely to happen next.

Here are four specific ways these documents improve your decision making:

-

Identifying cash flow cycles. Many small businesses experience seasonal revenue patterns. Your cash flow statement, reviewed monthly, will show you exactly when cash tightens and when it builds. This allows you to plan credit facilities, defer non-urgent expenditure, or time major purchases more precisely.

-

Spotting cost trends before they become problems. The income statement, compared across multiple periods, exposes rising costs that erode margins gradually. A 2% increase in supplier costs may seem minor in isolation, but tracked over six months it can represent a significant shift in profitability.

-

Supporting funding applications. Lenders use financial statements to decide on credit extension and may terminate loans based on them. When you approach a bank or investor, your statements are the primary evidence of your business's creditworthiness. Accurate, well-prepared statements accelerate the process and improve your terms.

-

Budgeting and forecasting with real data. Forecasts built on actual financial statement data are far more reliable than estimates based on memory or intuition. Your historical income statements and cash flow records give you a factual baseline from which to project future performance. You can also explore financial management tips to strengthen how you use this data in practice.

Pro Tip: Never assess your business's health on profit alone. A business showing net profit can still run out of cash if receivables are slow and payables are due. Always cross-reference the income statement with the cash flow statement before making any major spending decision.

Why are financial statements important beyond internal management?

The importance of financial statements extends well beyond your own management decisions. Financial statements are used in taxation, wage negotiations, and detailed business performance assessments by parties outside your organisation. This means the quality and accuracy of your statements directly affects your relationships with a wide range of external stakeholders.

External parties who rely on your financial statements include:

- Banks and lenders, who assess your ability to service debt and determine lending terms based on your balance sheet and cash flow statement.

- Investors and shareholders, who use your income statement and equity statement to evaluate returns and growth potential.

- Tax authorities, including the Finnish Tax Administration, which uses your financial records to verify reported taxable income and VAT obligations.

- Suppliers and trade creditors, who may assess your financial position before extending payment terms.

- Employees and unions, who may reference financial performance during wage negotiations or assessments of business stability.

Transparency and accuracy build investor confidence and access to capital. This is not simply a matter of good practice. Inaccurate or misleading statements can result in penalties from tax authorities, withdrawal of credit facilities, or lasting damage to your business reputation. For Finnish entrepreneurs, compliance with local accounting standards and timely submission of financial records is a legal obligation, not an optional discipline.

You can read more about how financial reports guide decisions and why their accuracy matters for businesses at every stage of growth.

Common pitfalls entrepreneurs face with financial statements

Many entrepreneurs understand that financial statements exist but do not use them to their full potential. Treating financial statements as annual obligations rather than ongoing management tools is one of the most common and costly mistakes a small business owner can make. The businesses that scale successfully tend to be those that review their statements frequently and interpret them actively.

The most common pitfalls include:

- Ignoring the cash flow statement. Focusing exclusively on net profit is a significant risk. A business can report strong profits while simultaneously running out of cash, particularly if it carries large receivables or has rapid growth consuming working capital.

- Annual-only reviews. Reviewing statements once a year, typically at tax time, means problems are identified months after they began. Monthly or at minimum quarterly reviews allow you to course-correct while options are still available.

- Misreading financial ratios in isolation. A current ratio or gross margin figure means little without context. Comparing ratios to your own historical data and to industry benchmarks gives them meaning. For sector-specific context, resources such as law firm financial statement guidance illustrate how professional services firms interpret these figures in practice.

- Failing to reconcile statements with each other. Each statement connects to the others. If your net profit does not reconcile with movements in your cash position and equity, something requires investigation.

Pro Tip: Use your financial statements as scenario planning tools. Run a simple projection: what happens to your cash position if your largest client pays 30 days late? Your cash flow statement gives you the data to answer that question before it becomes a crisis.

Guidance on how often to review your numbers confirms that most business owners review their finances far less frequently than is advisable. The discipline of regular review is what separates reactive management from genuinely informed leadership.

Key takeaways

Financial statements are most powerful when all four are reviewed together regularly, not treated as annual compliance documents.

| Point | Details |

|---|---|

| Use all four statements together | No single statement gives a complete picture; combine all four for accurate financial insight. |

| Cash flow is not the same as profit | A profitable business can still face insolvency if cash flow is poorly managed. |

| External stakeholders depend on accuracy | Lenders, tax authorities, and investors all base decisions on the quality of your statements. |

| Review monthly, not annually | Monthly reviews allow early detection of cost trends, cash shortfalls, and margin pressures. |

| Statements support forecasting | Historical statement data provides the factual baseline for reliable budgeting and planning. |

Why I think most entrepreneurs are using financial statements wrong

After working with small business owners across a range of sectors, the pattern I observe most consistently is this: entrepreneurs treat financial statements as a record of what happened, not as a tool for deciding what to do next. That distinction matters enormously.

I have seen businesses where the income statement showed consistent profitability for two consecutive years, yet the owners were genuinely surprised when a cash crisis emerged. The cash flow statement had been signalling the problem for months. Receivables were stretching, a major client had quietly extended payment terms, and the gap between profit and actual cash had been widening steadily. The data was there. Nobody was reading it.

The mindset shift I would encourage is straightforward. Stop thinking of your financial statements as documents you produce for your accountant or for the tax authority. Start thinking of them as the most reliable source of intelligence you have about your own business. Each statement serves a distinct purpose, and used together they tell you things that no dashboard, no gut feeling, and no bank notification can replicate.

The businesses I see grow with confidence are those where the owner sits down with their statements every month, asks specific questions, and adjusts their decisions accordingly. That habit, more than any single strategy, is what separates businesses that scale from those that stall.

— Busayo

How Finovate can help you get more from your statements

Accurate financial statements start with accurate records, and that is where many small business owners lose time and confidence. At Finovate, we provide bookkeeping, tax preparation, payroll processing, and business advisory services specifically designed for entrepreneurs and small businesses in Finland. We prepare your financial statements to the standard required by Finnish accounting regulations, and we help you understand what they are telling you about your business.

If you are ready to move from compliance-only thinking to genuinely informed financial management, visit Finovate's accounting services to see how we support entrepreneurs at every stage. You can also explore our Finnish SME financial statement examples to see how each statement applies in practice.

FAQ

What is the role of financial statements in a small business?

Financial statements provide a structured record of a business's financial performance, position, and cash flows, enabling owners to make informed decisions, meet legal obligations, and communicate financial health to lenders and investors.

Which financial statement is most important for entrepreneurs?

No single financial statement is most important. The balance sheet, income statement, and cash flow statement each capture different aspects of financial health and must be used together for a complete and accurate assessment.

How do financial statements support tax compliance in Finland?

The Finnish Tax Administration uses your financial records to verify taxable income, VAT obligations, and other reporting requirements. Accurate statements prepared in line with Finnish accounting standards are a legal requirement for registered businesses. You can find further guidance in our 2026 company tax planning guide.

How often should entrepreneurs review their financial statements?

Monthly reviews are the recommended standard. Frequent internal reviews contribute to scaling and avoiding cash crises, whereas annual-only reviews mean problems are typically identified too late to address effectively.

Can a profitable business still run into financial difficulty?

Yes. A business may report net profit while simultaneously facing a cash shortfall if receivables are slow or growth is consuming working capital faster than cash is collected. The cash flow statement is the document that reveals this risk.