TL;DR:

- Financial statements summarize business assets, liabilities, income, and cash flow, forming the basis for management and legal compliance.

- Reading all three documents regularly ensures accurate assessment of financial health and helps avoid potential cash flow issues.

Financial statements are formal records that summarise what your business owns, owes, earns, and spends. For Finnish small business owners, understanding these documents is not optional. They are the foundation of sound financial management, the basis for tax filings, and a legal requirement under Finnish accounting law. This article covers financial statements explained in plain language, walking you through each core statement, how to read it, and what Finnish-specific obligations apply to your business.

What are the core financial statements?

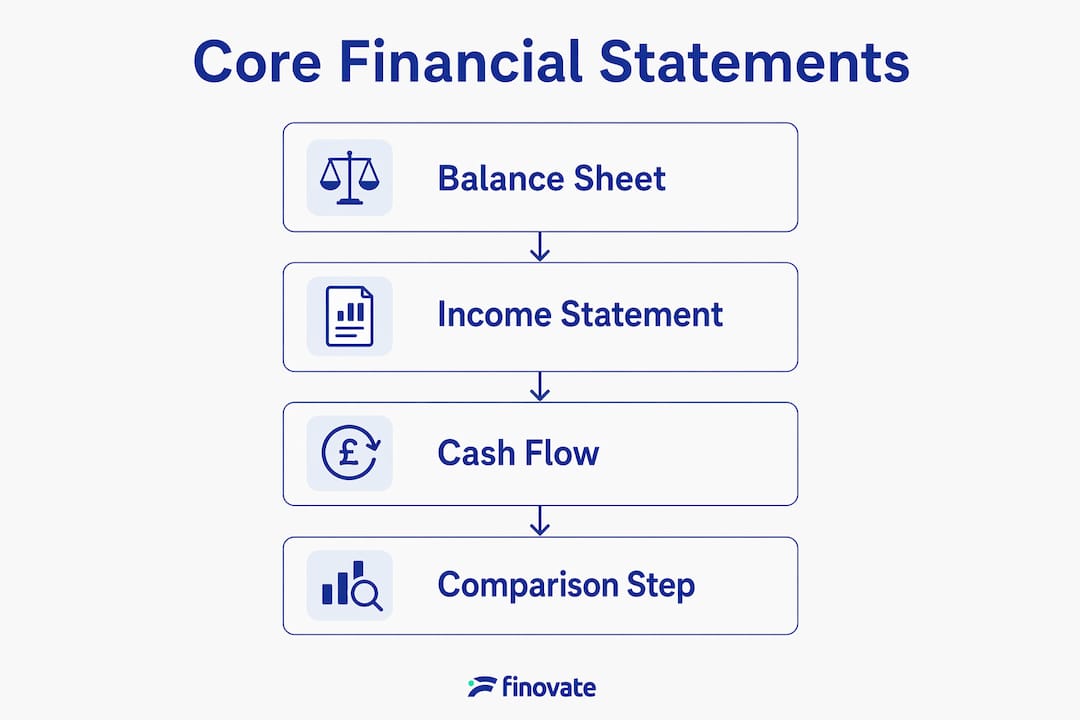

Financial statements consist of three core documents, and each one answers a different question about your business. The balance sheet, income statement, and cash flow statement together provide a complete picture of your financial position, profitability, and liquidity. No single document tells the whole story on its own.

Here is what each one does:

- Balance sheet (tase): Shows what your business owns (assets) and owes (liabilities) at a specific point in time. The difference between the two is your equity. It answers: what do we own and owe right now?

- Income statement (tuloslaskelma): Tracks revenue and expenses over a period, such as a financial year, to show whether your business made a profit or a loss. It answers: are we profitable?

- Cash flow statement (rahavirtalaskelma): Records actual cash moving in and out of your business over a period. It answers: do we have cash available to pay our bills?

Reading these three documents together reveals how profit affects your equity and cash position. For example, income statement profit flows directly into retained earnings on the balance sheet. The cash flow statement then explains why your actual cash balance may differ from that profit figure.

Pro Tip: If you only review one document, you are missing critical information. A business can show a profit on the income statement while running dangerously low on cash. Always read all three together.

How do you interpret each financial statement?

Understanding what each statement contains is one thing. Knowing what to look for when you read it is another. Here is a practical approach for each document, tailored to the Finnish small business context.

1. reading the balance sheet

Start with the equity figure. This is your business's net worth at that moment. If equity is growing year on year, your business is building value. If it is shrinking, you are consuming reserves. Next, examine the ratio of current assets (cash, receivables, inventory) to current liabilities (short-term debts, unpaid invoices). A healthy business holds more current assets than current liabilities.

2. reading the income statement

Focus on three lines: total revenue, total expenses, and net profit or loss. A Finnish sole trader (toiminimi) will want to track whether net profit is consistent across periods. Watch for expenses growing faster than revenue. That pattern signals a problem before it becomes a crisis.

3. reading the cash flow statement

The cash flow statement reconciles accounting profit with actual cash, revealing whether your profits are backed by real money. This is especially useful when you use accrual accounting, where you record income when invoiced rather than when paid. A Finnish entrepreneur who invoices in December but receives payment in February will show profit in December but no cash until February. The cash flow statement makes this timing gap visible.

4. comparing all three together

The most common mistake is reading each statement in isolation. Compare the net profit on your income statement with the net cash from operations on your cash flow statement. A large gap between the two signals a working capital issue, often caused by slow-paying customers or high inventory levels. Reviewing your bookkeeping best practices regularly helps you catch these gaps early.

Pro Tip: Set a fixed date each month to review all three statements side by side. Thirty minutes of structured review is worth more than hours of reactive problem-solving later.

What are the finnish bookkeeping and filing requirements?

Finnish law sets clear rules on how you must keep your books and when you must file your financial statements. Getting this right protects you from penalties and keeps your business credible.

Bookkeeping methods under finnish law

Finnish bookkeeping law permits toiminimi entrepreneurs to use single-entry bookkeeping (muistiinpanomenetelmä) if they meet all three of the following thresholds:

| Threshold | Limit |

|---|---|

| Annual turnover | Under €200,000 |

| Balance sheet total | Under €100,000 |

| Number of employees | Maximum 3 |

If your business exceeds any one of these limits, you must switch to double-entry accounting. Double-entry accounting produces both a balance sheet and an income statement to the legal standard. Single-entry bookkeeping only records cash received and paid, which means it does not produce a full balance sheet. Understanding double-entry accounting before you approach these thresholds saves significant stress.

PRH filing obligations and deadlines

All limited companies (osakeyhtiö) and most other registered business forms must file their annual financial statements (tilinpäätös) with the Finnish Trade Register (PRH). The deadline is eight months after the end of the financial year. For a business with a calendar year ending 31 December, the filing deadline falls on 31 August.

The consequences of missing this deadline are financial and reputational:

- Late fees start at €150 for filings submitted after the deadline.

- Fees rise to €600 if the filing is more than four months late.

- Repeated late filings result in doubled penalties.

- Around 35,000 tilinpäätös filings were missing as of late 2025, representing roughly 10% of all registered companies.

That last figure is striking. One in ten Finnish companies failed to meet the filing deadline. PRH began active enforcement in autumn 2025, so the era of overlooked late filings is over. A compliance calendar is no longer a nice-to-have. It is a practical necessity.

What challenges do finnish business owners face with financial statements?

Most small business owners in Finland are not accountants. The following pitfalls are common, and knowing them in advance helps you avoid them.

- Over-relying on the income statement. Profit looks reassuring on paper. But accrual accounting can show profit while your bank account is nearly empty. Always cross-check with the cash flow statement.

- Misreading cash timing. Invoicing a client does not mean you have cash. Finnish payment terms of 14–30 days create gaps between revenue recognition and actual receipt. Track these gaps on your cash flow statement.

- Ignoring equity changes. If retained earnings on your balance sheet are declining, your business is spending more than it earns over time. This is a slow warning sign that the income statement alone may not reveal clearly.

- Delaying the transition to double-entry bookkeeping. Toiminimi entrepreneurs approaching the simplified bookkeeping thresholds often wait too long to switch. Transitioning mid-year creates complexity. Plan the move at the start of a new financial year.

- Not using software. Manual bookkeeping increases error rates and makes it harder to produce accurate statements quickly. Tools like Procountor, Netvisor, or Visma Fivaldi are widely used by Finnish SMEs and integrate directly with PRH reporting requirements.

"Understanding your financial statements is not just a compliance task. It is the clearest signal you have about where your business stands and where it is heading."

Reading all three statements together, on a regular schedule, is the single most effective habit a Finnish entrepreneur can build. The financial reporting basics are not complicated once you know what each document is telling you.

Key takeaways

Reading all three core financial statements together is the only reliable way to understand your business's true financial health, meet Finnish legal obligations, and make confident decisions.

| Point | Details |

|---|---|

| Three core statements | Balance sheet, income statement, and cash flow statement each answer a distinct financial question. |

| Read them together | Profit on the income statement does not equal cash in the bank; always cross-check all three. |

| Finnish filing deadlines | PRH requires tilinpäätös filing within eight months of year-end; late fees start at €150. |

| Bookkeeping thresholds | Toiminimi owners may use single-entry bookkeeping only if turnover, balance sheet, and employee limits are all met. |

| Act before thresholds | Plan the switch to double-entry accounting before you exceed simplified bookkeeping limits, not after. |

Why finnish entrepreneurs should treat financial statements as a management tool

Most of the Finnish business owners I work with come to financial statements reluctantly. They see them as a compliance obligation, something to hand to an accountant once a year and forget about. That view is understandable, but it is also costly.

The income statement is the document most owners look at first, and often last. It shows a profit, they feel reassured, and they move on. What they miss is the cash flow statement sitting quietly alongside it, showing that the same business has a growing gap between invoiced revenue and collected cash. That gap is where businesses get into trouble, not because they are unprofitable, but because they run out of cash while waiting to be paid.

The balance sheet is even more neglected. Equity is not just an accounting figure. It tells you whether your business is accumulating value or slowly eroding it. A declining equity position over two or three years is a serious warning. Catching it early gives you options. Catching it late gives you a crisis.

My honest recommendation is this: schedule a monthly thirty-minute review of all three statements. You do not need to be an accountant to do it. You need to know what questions to ask. Is cash from operations positive? Is equity growing? Are expenses rising faster than revenue? Those three questions, answered monthly, will tell you more about your business than any single annual review ever will.

The PRH enforcement changes in 2025 are also a signal worth taking seriously. The Finnish Trade Register is no longer passive about late filings. If you are not already working with a bookkeeper or accountant who tracks your deadlines, now is the time to put that support in place.

— Busayo

How Finovate can help you stay on top of your financial statements

Managing your financial statements alongside running a business is demanding. Finovate provides expert accounting and bookkeeping services for Finnish small businesses and entrepreneurs, covering everything from day-to-day bookkeeping to PRH-compliant tilinpäätös preparation.

Whether you are a light entrepreneur needing a reliable monthly invoicing service or a growing toiminimi approaching the double-entry accounting threshold, Finovate's team handles the compliance work so you can focus on your business. We keep your books accurate, your filings on time, and your financial statements ready when you need them. Contact Finovate today to discuss how we can support your financial reporting and help you avoid costly PRH late fees.

FAQ

What are the three main financial statements?

The three core financial statements are the balance sheet (tase), the income statement (tuloslaskelma), and the cash flow statement (rahavirtalaskelma). Each answers a different question about your business's financial position, profitability, and liquidity.

When must finnish companies file their financial statements with PRH?

Finnish companies must file their annual financial statements (tilinpäätös) with the Finnish Trade Register (PRH) within eight months of the end of their financial year. Missing this deadline results in late fees starting at €150, rising to €600 for filings more than four months overdue.

Can a finnish sole trader use simplified bookkeeping?

A toiminimi entrepreneur may use single-entry bookkeeping (muistiinpanomenetelmä) only if all three thresholds are met: annual turnover under €200,000, balance sheet total under €100,000, and no more than three employees. Exceeding any one threshold requires a switch to double-entry accounting.

Why does my business show a profit but have no cash?

This is a common result of accrual accounting, where income is recorded when invoiced rather than when received. The cash flow statement reconciles this difference by showing actual cash movements, making it the most reliable document for assessing short-term liquidity.

How often should i review my financial statements?

Monthly reviews of all three statements are the most effective approach for small business owners. A regular review helps you spot cash timing issues, track equity changes, and identify rising costs before they become serious problems.