TL;DR:

- A balance sheet provides a snapshot of a business's assets, liabilities, and owner’s equity at a specific moment, essential for assessing financial health and making informed decisions. Key ratios like current ratio, debt-to-equity, and working capital reveal liquidity, leverage, and operational strength, with trends over time offering deeper insights. Regular review, accurate bookkeeping, and understanding disclosures are vital for Finnish SMEs to prevent financial issues and leverage their balance sheets as strategic management tools.

A balance sheet is a financial statement that shows what your business owns, what it owes, and the residual value belonging to you as the owner at a specific point in time. For Finnish entrepreneurs and small business owners, understanding balance sheets is not a compliance exercise. It is the clearest window into your company's financial health, and the decisions you make about credit, investment, and growth depend on reading it correctly. Tools like QuickBooks Online make it easier than ever to produce accurate statements, but knowing how to interpret what you see is where the real value lies.

What are the main components of a balance sheet?

The fundamental accounting equation is Assets = Liabilities + Equity, and this equation must always hold true at the date the statement is prepared. Every figure on the balance sheet sits on one side of this equation. If it does not balance, something has gone wrong in your bookkeeping.

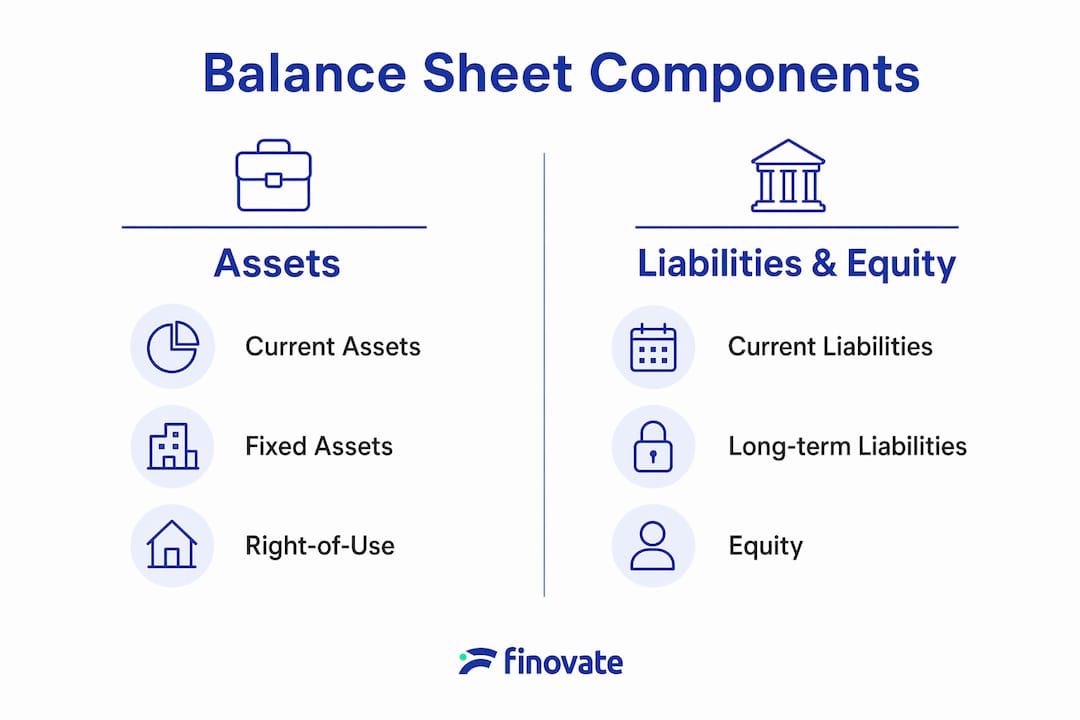

Assets represent everything your business controls that has economic value. They are split into two categories:

- Current assets: Cash, trade receivables, prepaid expenses, and inventory. These are expected to be converted to cash or consumed within 12 months.

- Non-current assets: Property, equipment, vehicles, and intangible assets such as patents or goodwill. These provide value over a longer period and are subject to depreciation.

Liabilities represent what your business owes to others. Again, the split matters:

- Current liabilities: Accounts payable, VAT payable, short-term loans, and accrued wages. These fall due within 12 months.

- Non-current liabilities: Long-term bank loans, deferred tax liabilities, and lease obligations under IFRS 16 right-of-use asset accounting. These extend beyond the coming year.

Equity is the residual interest once liabilities are subtracted from assets. For a Finnish sole trader or limited company (Oy), equity typically includes the owner's invested capital, retained earnings from prior years, and the current year's profit or loss. Owner's draws reduce equity directly, which is why mixing personal and business finances distorts this figure badly.

Depreciation deserves a specific mention. When you purchase a piece of equipment, its cost does not hit your expenses all at once. It is spread across its useful life, reducing the asset's carrying value on the balance sheet each year. Ignoring this means your assets are overstated and your equity is inflated.

Pro Tip: If your business leases premises or vehicles, check whether those leases are recorded as right-of-use assets and corresponding liabilities on your balance sheet. Under current accounting standards, many operating leases must appear on the balance sheet, and missing them understates your total obligations.

How do key ratios from the balance sheet reveal financial health?

Balance sheet analysis becomes most powerful when you calculate ratios from the figures. Ratio analysis works like a structured health assessment: standardised measurements tell you whether your financial position is strengthening or deteriorating over time.

Here are the three ratios every Finnish SME owner should track:

-

Current ratio (Current assets ÷ Current liabilities): A current ratio above 1.0 means you have enough short-term assets to cover immediate debts. A ratio below 1.0 signals potential liquidity problems. Most lenders and advisors look for a ratio between 1.5 and 2.0 for healthy small businesses.

-

Debt-to-equity ratio (Total liabilities ÷ Total equity): This measures how much of your business is financed by debt versus your own capital. Benchmarks vary by industry: a manufacturing company carrying significant equipment debt will naturally show a higher ratio than a consulting firm. Comparing your ratio against sector averages gives it real meaning.

-

Working capital (Current assets minus current liabilities): This is the cash buffer available to fund day-to-day operations. Negative working capital is a warning sign that your business may struggle to pay suppliers or staff on time.

| Ratio | Formula | What it tells you |

|---|---|---|

| Current ratio | Current assets ÷ current liabilities | Short-term liquidity and ability to meet immediate debts |

| Debt-to-equity | Total liabilities ÷ total equity | Degree of financial leverage and reliance on borrowed funds |

| Working capital | Current assets minus current liabilities | Operational buffer available for day-to-day expenses |

One critical point: a single ratio at one point in time tells you very little. Reviewing ratios over 3 to 5 years reveals whether your liquidity is improving, your debt is growing faster than your equity, or your working capital is being eroded. Trends are far more informative than snapshots.

Pro Tip: Never interpret a ratio in isolation. A debt-to-equity ratio of 2.0 might be perfectly acceptable for a Finnish manufacturing company with predictable cash flows, but alarming for a retail business with seasonal revenue.

What mistakes do entrepreneurs make when reading their balance sheets?

Most errors in balance sheet interpretation come not from complexity but from overlooked details. Recognising these pitfalls will save you from making decisions based on misleading figures.

-

Mixing personal and business finances. Owner's draws taken informally, personal expenses paid through the business account, or loans between the owner and the company all distort equity and liabilities. Finnish limited companies (Oy) are legally separate entities, and the balance sheet must reflect that separation.

-

Ignoring depreciation. If your fixed assets are not being depreciated correctly, your balance sheet overstates what the business is actually worth. This affects both your equity figure and any ratio calculations you perform.

-

Missing off-balance-sheet commitments. Footnotes and disclosures reveal lease commitments, contingent liabilities, and intangible asset valuations that raw numbers do not show. Skipping the notes means you are reading an incomplete picture.

-

Failing to update records regularly. A balance sheet prepared once a year for tax purposes is not the same as a management tool. Stale data leads to stale decisions.

-

Misinterpreting ratios without context. Comparing your debt-to-equity ratio to a generic benchmark without accounting for your industry or business model produces misleading conclusions. Debt-to-equity standards are industry-dependent, and SME owners must tailor interpretation to their sector.

-

Accepting an unbalanced sheet. When a balance sheet fails to balance, it almost always signals miscategorised or missing entries. This requires immediate review, not a workaround.

Pro Tip: Always read the footnotes before drawing conclusions from the main figures. A balance sheet that looks healthy on the surface can carry significant hidden obligations in the notes, particularly around lease commitments and related-party transactions.

How can Finnish SMEs use balance sheets for better financial management?

Understanding financial statements is one thing. Putting that understanding to work in your business is another. Here is a practical approach for Finnish small business owners.

-

Review monthly, not annually. A monthly review of your balance sheet alongside your income statement and cash flow statement gives you a complete picture of financial health. Annual reviews only catch problems after they have already caused damage.

-

Use accounting software. QuickBooks automates account reconciliation and classification, which reduces the manual errors that cause balance sheets to go out of balance. For Finnish SMEs, software that integrates with local VAT reporting requirements adds further value.

-

Track ratio trends as early warning signals. If your current ratio has fallen from 1.8 to 1.1 over six months, that is a signal to investigate before it drops below 1.0. Ratio changes are often visible on the balance sheet before they become visible in your bank account.

-

Use your balance sheet to plan credit decisions. Before applying for a business loan from a Finnish bank, calculate your debt-to-equity ratio and working capital position. Lenders will. Knowing your figures in advance lets you address weaknesses or present your position confidently.

-

Integrate balance sheet review with tax planning. In Finland, your balance sheet directly informs your corporate tax position. Retained earnings, depreciation schedules, and asset valuations all affect your taxable income. Working with an advisor who understands both the accounting and the Finnish tax framework means you are not leaving money on the table.

The importance of balance sheets extends beyond compliance. When you review your balance sheet regularly, you spot over-leveraging early, you identify assets that are no longer productive, and you make investment decisions from a position of clarity rather than guesswork. Finnish SMEs that treat their balance sheet as a live management tool, rather than a year-end formality, consistently make better financial decisions. Pairing this habit with financial reporting templates designed for Finnish SMEs makes the monthly review process faster and more consistent.

Pro Tip: If your balance sheet shows a strong equity position but your cash flow is consistently tight, investigate your receivables. Long payment terms or slow-paying clients can make your balance sheet look healthy while your business struggles to pay its bills on time.

Key takeaways

A balance sheet is the single most direct indicator of a business's financial position, and reading it correctly requires understanding its structure, its ratios, and its limitations.

| Point | Details |

|---|---|

| The accounting equation always holds | Assets must equal liabilities plus equity; any discrepancy signals a bookkeeping error requiring immediate attention. |

| Ratios need context and trends | Compare current ratio, debt-to-equity, and working capital over 3 to 5 years and against industry benchmarks, not in isolation. |

| Footnotes are not optional | Disclosures reveal off-balance-sheet obligations and accounting assumptions that raw figures do not show. |

| Monthly review is the standard | Reviewing your balance sheet monthly alongside the income and cash flow statements provides a complete picture of financial health. |

| Software reduces errors | Accounting tools like QuickBooks automate reconciliation and classification, improving accuracy as your business grows. |

Why balance sheet literacy matters more than most Finnish entrepreneurs realise

I have worked with many small business owners in Finland who are genuinely skilled at running their operations but treat their balance sheet as something their accountant handles once a year. That approach is a risk they are taking without realising it.

The balance sheet is not just a compliance document. It is a diagnostic tool that tells you whether your business is building real value or quietly accumulating fragility. A company can show a profit on its income statement while its balance sheet reveals deteriorating liquidity and growing debt. Those two things can coexist, and if you only look at profit, you will miss the warning.

What I have seen repeatedly is that financial distress rarely arrives without warning. The signals are there in the balance sheet months before a cash crisis becomes acute. A current ratio sliding toward 1.0, working capital shrinking quarter by quarter, equity being eroded by draws that exceed earnings. These are readable patterns, and they are preventable if you catch them early.

Finnish SMEs operate in a transparent financial environment. Banks, tax authorities, and potential investors all have access to your filed accounts. The business owners who understand their own numbers are always better positioned in those conversations than those who rely entirely on their accountant to explain what the figures mean.

My honest recommendation: schedule a 30-minute monthly review of your three core financial statements. You do not need to be an accountant to do this. You need to know what the key ratios mean, what direction they are moving, and when to ask for help. That habit alone separates businesses that grow with confidence from those that are perpetually surprised by their own finances.

— Busayo

Let Finovate help you put your balance sheets to work

If reading through your balance sheet still raises more questions than answers, you are not alone. Many Finnish entrepreneurs find that having a professional review their figures transforms the balance sheet from a confusing document into a genuine planning tool.

Finovate provides accounting and tax services tailored specifically for Finnish small businesses and entrepreneurs, covering bookkeeping, VAT reporting, payroll processing, and business advisory. Our team helps you maintain accurate, up-to-date financial records and interprets what your balance sheet is telling you about your business's health. Whether you need support with monthly reporting, tax planning, or growth advisory for Finnish SMEs, we are ready to help. Contact Finovate to discuss a service package that fits your business.

FAQ

What is a balance sheet in simple terms?

A balance sheet is a financial statement that lists everything your business owns (assets), everything it owes (liabilities), and the owner's residual interest (equity) at a specific date. The total assets must always equal the combined total of liabilities and equity.

How often should a small business review its balance sheet?

Monthly review is the recommended standard. Reviewing your balance sheet alongside your income statement and cash flow statement each month allows you to spot liquidity issues and ratio changes before they become serious problems.

What does it mean if my balance sheet does not balance?

If your total assets do not equal your total liabilities plus equity, there is an error in your bookkeeping entries. This typically means a transaction has been miscategorised or omitted, and it requires immediate investigation to maintain financial integrity.

Which balance sheet ratio is most useful for small businesses?

The current ratio (current assets divided by current liabilities) is the most immediately useful for small businesses because it directly measures your ability to meet short-term obligations. A ratio above 1.0 indicates sufficient liquidity; below 1.0 signals potential cash flow risk.

Is a balance sheet the same as a profit and loss statement?

No. A balance sheet shows your financial position at a specific point in time, covering assets, liabilities, and equity. A profit and loss statement (income statement) covers revenues and expenses over a period of time and measures profitability, not financial position.