TL;DR:

- Managing finances accurately with double entry accounting is legally required for most Finnish businesses and offers error detection, fraud prevention, and comprehensive financial insights. It involves recording each transaction with equal debits and credits across accounts, supporting clear financial statements and compliance. Regular reconciliation and understanding of accrual basis recording enhance decision-making and business growth.

Running a business in Finland means managing finances carefully, yet many small business owners find accounting confusing and time-consuming. If you have wondered what is double entry accounting and why it matters for your business, you are not alone. This article explains the core principles of double entry bookkeeping, outlines Finnish legal requirements, and shows you how to apply this system confidently. By the end, you will understand how double entry accounting supports accurate financial records, tax compliance, and better business decisions.

Table of Contents

- Double entry accounting explained: the core principles

- Why double entry accounting is essential for Finnish businesses

- Trial balance and accrual accounting: maintaining accuracy and clarity

- Double entry vs single entry bookkeeping: what Finnish entrepreneurs should know

- Practical steps to implement double entry accounting in your Finnish business

- The overlooked benefits and realities of double entry accounting for Finnish entrepreneurs

- Professional accounting services to support your double entry bookkeeping in Finland

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Double-entry basics | Every transaction affects at least two accounts keeping the accounting equation balanced. |

| Finnish legal requirement | Most Finnish companies and larger self-employed must use double-entry accounting to comply with law. |

| Accuracy tools | Trial balance and accrual accounting help maintain precise and clear financial records. |

| Better than single-entry | Double-entry provides a complete financial picture essential for compliance and growth. |

| Professional support | Using software and expert accountants reduces errors and simplifies your bookkeeping. |

Double entry accounting explained: the core principles

Double entry accounting is the foundation of modern financial record-keeping. Put simply, every financial transaction is recorded in at least two accounts with equal debits and credits, so the accounting equation Assets = Liabilities + Equity always balances. Every time money moves in your business, two things happen simultaneously: one account increases and another decreases by the same amount.

The accounting equation is central to how double entry works. If you purchase equipment for €5,000, your assets (equipment) increase by €5,000 and your cash (also an asset) decreases by €5,000. The equation stays in balance. If you take out a bank loan for €10,000, your cash assets rise by €10,000 and your liabilities rise by €10,000. Every transaction tells a complete story.

Understanding debits and credits is often where people stumble. They do not simply mean money coming in or going out. A debit increases asset and expense accounts but decreases liability, income, and equity accounts. A credit does the opposite. A useful mnemonic to remember this is DEAD/CLIC:

- Debits increase: Expenses, Assets, Drawings

- Credits increase: Liabilities, Income, Capital

This framework turns an abstract concept into something you can apply immediately. Understanding bookkeeping basics for small businesses gives you a strong starting point before applying these principles in practice.

Why double entry accounting is essential for Finnish businesses

Finnish law does not treat double entry bookkeeping as optional for most businesses. Double-entry bookkeeping is mandatory for all companies and corporations in Finland, and for self-employed business operators if two out of three thresholds are met: a balance-sheet total over EUR 100,000, turnover over EUR 200,000, or an average of more than three employees. If your business is growing, you may cross these thresholds sooner than expected.

"Double-entry provides a check and balance for each transaction, helping ensure accuracy, prevent fraud, and track finances effectively for better resource allocation decisions." — Coursera

Beyond legal compliance, double entry accounting gives you practical advantages that single entry simply cannot match. Here is what this system offers Finnish entrepreneurs:

- Error detection: Because every transaction must balance, mistakes create an imbalance that is immediately visible.

- Fraud prevention: Two-sided recording makes it much harder for transactions to be altered without leaving a trace.

- Complete financial picture: You can see not just cash flow but your full balance sheet, including what you own and what you owe.

- Tax reporting accuracy: Finnish tax authorities expect detailed, accurate financial statements. Double entry supports this directly.

- Investor and lender confidence: Banks and investors in Finland require auditable financial records before extending credit or funding.

Following bookkeeping best practices for Finnish businesses alongside double entry accounting means you are positioned well for both audits and growth. For a broader view, our guide on accounting rules and best practices in Finland covers the regulatory framework in detail.

Trial balance and accrual accounting: maintaining accuracy and clarity

Once you have recorded transactions using double entry bookkeeping, the trial balance is your key verification tool. The trial balance lists all ledger account balances where total debits must equal total credits, to verify accuracy before producing financial statements. Think of it as a final check before you commit numbers to an official report.

In Finland, double entry accounting is used alongside accrual basis recording. Under Finnish Accounting Standards (FAS), accrual basis recording recognises income and expenses when earned or incurred, not when cash changes hands. This gives a more accurate view of your business's financial position at any given moment.

Here is a comparison of cash basis versus accrual basis accounting to clarify the difference:

| Feature | Cash basis | Accrual basis |

|---|---|---|

| Revenue recognition | When cash is received | When earned |

| Expense recognition | When cash is paid | When incurred |

| Financial accuracy | Lower | Higher |

| Required under FAS | No | Yes for most |

| Suited to | Very small sole traders | Most Finnish businesses |

Preparing your trial balance involves a clear process. Follow these steps each month:

- Post all journal entries to the relevant ledger accounts.

- Calculate the closing balance for every account.

- List all debit balances in one column and all credit balances in another.

- Confirm total debits equal total credits.

- Investigate and correct any discrepancy before preparing financial statements.

Pro Tip: The trial balance catches arithmetic errors, but it does not catch every mistake. If you debit the wrong account or record a transaction twice, the balance may still appear equal. Monthly bank reconciliation, as outlined in this step-by-step bookkeeping guide, is essential for catching these subtler errors. For businesses exploring simpler methods, you can also read about cash accounting in Finland to understand when it might apply. The OP Financial Group's financial coaching resource is also worth consulting if you want to deepen your understanding.

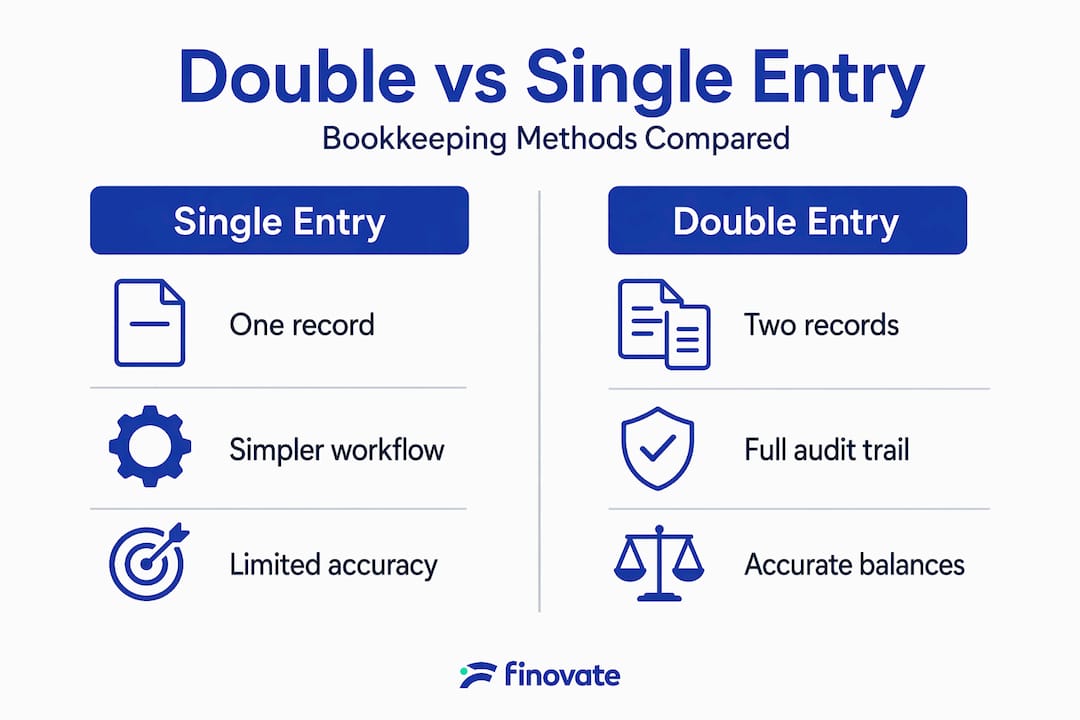

Double entry vs single entry bookkeeping: what Finnish entrepreneurs should know

Single entry bookkeeping records each transaction once, usually as either an income or an expense. It is simpler and quicker, but it paints an incomplete picture. Unlike single entry, which tracks only one side, double entry reflects both the money source and its destination, which is essential for accurate reports, compliance, and informed decisions.

| Feature | Single entry | Double entry |

|---|---|---|

| Recording method | One entry per transaction | Two entries per transaction |

| Error detection | Difficult | Built in |

| Financial statements | Income statement only | Full balance sheet and income statement |

| Compliance with Finnish law | Limited use cases | Mandatory for most businesses |

| Fraud detection | Weak | Strong |

| Suitable for | Very small, informal businesses | Companies, corporations, growing sole traders |

The practical difference becomes clear when you need to apply for a loan or respond to a tax authority query. With double entry bookkeeping, you can produce a balance sheet, an income statement, and a cash flow statement. With single entry, you cannot.

Here are the key advantages double entry offers over single entry for Finnish entrepreneurs:

- You always know your exact asset and liability position.

- Financial statements required by Finnish law are straightforward to produce.

- Your accounts are auditable, which protects you in the event of a tax inspection.

- You can track profitability by product line, project, or time period.

Pro Tip: If you are a freelancer or sole trader just starting out, review whether you meet the thresholds requiring double entry. Our guide on accounting for freelancers in Finland clarifies your obligations. For those growing into SME territory, the SME bookkeeping compliance guide is a practical next step.

Practical steps to implement double entry accounting in your Finnish business

Starting double entry bookkeeping is far more manageable when you follow a clear process. Recording journal entries chronologically and then posting them to ledger accounts is the core workflow. FAS-compliant software automates much of this, but reviewing your trial balance regularly ensures total debits equal total credits and prevents common errors from compounding.

Here is a practical step-by-step process to get started:

- Open a chart of accounts. This is a structured list of every account your business uses, covering assets, liabilities, equity, income, and expenses.

- Record transactions in a journal. For every transaction, note the date, the accounts affected, the amounts debited and credited, and a brief description.

- Post entries to ledger accounts. Transfer each journal entry to the relevant account in your ledger, updating the running balance.

- Prepare a monthly trial balance. Verify that debits and credits match across all accounts.

- Conduct bank reconciliations. Compare your ledger cash balance against your bank statement monthly.

- Produce financial statements. At year end, prepare your income statement and balance sheet, which are required for Finnish tax filings.

Pro Tip: Choose accounting software that supports Finnish Accounting Standards (FAS) and can generate VAT reports in the format the Finnish Tax Administration expects. This saves considerable time during tax season and reduces the risk of errors in your VAT declarations. See our bookkeeping best practices guide for software recommendations suited to Finnish businesses. Our essential tax tips for Finnish entrepreneurs also cover year-end preparation in detail.

The overlooked benefits and realities of double entry accounting for Finnish entrepreneurs

Most articles about double entry accounting stop at compliance. That is understandable, but it misses the point. The most valuable thing double entry gives you is clarity. Double-entry accrual accounting provides comprehensive insights on capital, liabilities, and assets, which are crucial for Finnish entrepreneurs to interpret key figures and plan ahead with accountant support. When you can see your full financial picture at any moment, you make better decisions about hiring, purchasing, and pricing.

One reality we see regularly is that business owners misunderstand the direction of debits and credits when they start. This leads to entries that appear balanced but are posted to the wrong accounts. A bank deposit credited as income instead of as an asset reduces your apparent liabilities but overstates your revenue. The trial balance will not flag this. Only a careful review of individual account entries, or a professional audit, will catch it.

Another underestimated point: double entry accounting is not just for year-end tax preparation. When you review your trial balance monthly, you gain a rolling picture of profitability, cash position, and liability levels. This is how financially sound Finnish businesses spot problems early and respond before they become crises. Our bookkeeping best practices guide goes into this monthly discipline in more depth.

The honest advice we would give any Finnish entrepreneur is this: do not wait until your business hits the legal thresholds to adopt double entry. Start early, build good habits, and use your financial data actively. Businesses that treat accounting as a management tool, not just a legal obligation, consistently make sharper decisions about growth, financing, and resource allocation.

Professional accounting services to support your double entry bookkeeping in Finland

Getting double entry bookkeeping right from the start saves time, reduces costly errors, and protects your business during tax audits.

We offer tailored accounting, VAT reporting, payroll processing, and tax planning services designed specifically for small Finnish businesses and entrepreneurs. Whether you are setting up your books for the first time or need ongoing support to maintain compliance, we are here to help. Our team understands Finnish Accounting Standards and the specific requirements of the Finnish Tax Administration, so you can focus on running your business with confidence. Explore our expert accounting and tax services to find the right level of support for your situation. If you are operating as a light entrepreneur, our light entrepreneur accounting package is designed to keep your records accurate and your obligations clear.

Frequently asked questions

Is double entry accounting mandatory for all businesses in Finland?

Double entry bookkeeping is mandatory for all companies and corporations in Finland, and for self-employed business operators meeting two of three thresholds relating to balance-sheet total, turnover, or employee count. Very small sole traders below these thresholds may use single entry.

What is the main difference between single entry and double entry bookkeeping?

Single entry records only one side of each transaction, while double entry records both debit and credit sides to keep accounts balanced and produce full financial statements required for compliance.

How does the trial balance help in double entry bookkeeping?

The trial balance lists all ledger balances to confirm that total debits equal total credits, which helps you detect arithmetic errors before finalising financial statements.

Why is accrual accounting used in Finland alongside double entry?

Accrual accounting recognises income and expenses when earned or incurred rather than when cash is received or paid, providing a true financial position required under Finnish Accounting Standards.

Can I manage double entry bookkeeping without an accountant?

Yes, FAS-compliant software can automate much of the process, but regular trial balance reviews and periodic professional input are strongly recommended to avoid errors that the software alone will not flag.