TL;DR:

- Many Finnish SME owners face accounting issues during tax filing or audits due to misallocated transactions and incomplete steps. The accounting cycle ensures accurate, timely financial reporting by guiding each stage, from transaction recognition to closing the books, with compliance to Finnish regulations. Mastering this cycle enhances financial clarity, reduces errors, and streamlines growth and tax processes.

Many Finnish small business owners discover accounting problems at the worst possible moment, usually when preparing for tax filing or facing a Vero.fi audit query. A single misallocated transaction, a skipped adjusting entry, or a closing step left incomplete can distort your financial statements and trigger compliance issues that take significant time and expense to correct. The accounting cycle exists precisely to prevent this. It is a structured, repeating process that ensures every financial transaction is properly captured, verified, and reported within the correct period. This guide explains each stage of the cycle in clear terms, with specific attention to Finnish regulations and the practical realities facing SME owners.

Table of Contents

- What is the accounting cycle?

- Step-by-step: The main stages of the Finnish accounting cycle

- Why timing and accruals matter: Critical points for SMEs

- From closing the books to filing: Compliance deadlines and preparing financial statements

- Why mastering the accounting cycle is a business superpower for Finnish SMEs

- Professional support for your accounting cycle in Finland

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Accounting cycle basics | The accounting cycle is a structured process that ensures all business transactions are tracked and reported correctly. |

| Finnish compliance essentials | SMEs must match bookkeeping methods to their structure and meet strict financial statement deadlines to stay compliant. |

| The importance of timing | Accurately recording transactions in the correct period prevents errors and avoids compliance risks for Finnish businesses. |

| Strategic advantage | A disciplined accounting cycle is more than compliance—it enables smarter decisions and more efficient use of resources. |

What is the accounting cycle?

The accounting cycle is the complete sequence of steps a business follows to record, process, and report its financial transactions for a given period. It starts the moment a financial event occurs and ends when the books are closed and financial statements are prepared. Then it begins again for the next period. Think of it as a quality-control system for your finances, one that repeats monthly, quarterly, or annually depending on your business.

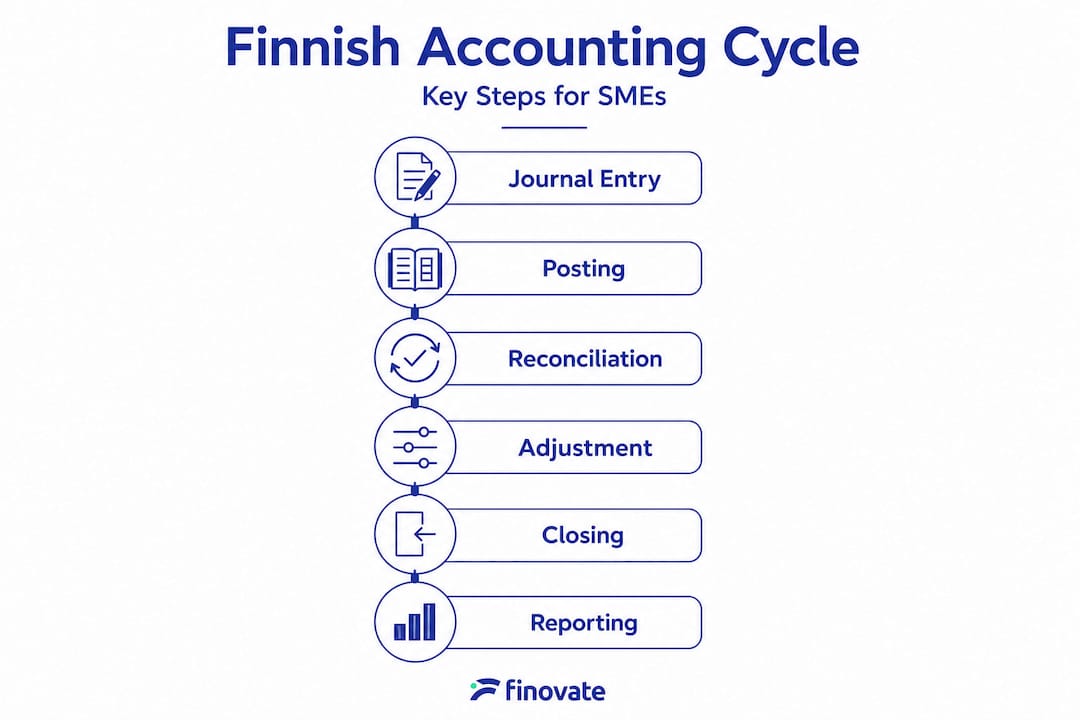

The classic phases of the accounting cycle are:

- Transaction identification: Recognising which business events have a financial impact

- Journal entry: Recording those events in chronological order with supporting documents

- Ledger posting: Transferring journal entries to the relevant accounts in your general ledger

- Trial balance: Checking that debits equal credits before making any adjustments

- Adjusting entries: Correcting for accruals, prepayments, and timing differences at period end

- Financial statements: Preparing the income statement, balance sheet, and cash flow statement

- Closing the books: Resetting temporary accounts so the cycle can restart

Understanding these finance terms explained before you engage with your accountant will make every conversation more productive and every review far less stressful.

In Finland, the legal framework shapes how you move through this cycle. For Finnish businesses, double-entry bookkeeping on an accruals basis is mandatory for companies and corporations, which supports the accounting cycle approach of recording transactions in the correct period. Self-employed individuals, such as sole traders and freelancers, may use single-entry bookkeeping but must still make accrual adjustments at year-end for tax purposes. The cycle structure applies to both, even if the mechanics differ slightly.

Key insight: Getting each period right is not just about compliance. It gives you an accurate picture of your business performance at any given moment, which is essential for making sound decisions.

Step-by-step: The main stages of the Finnish accounting cycle

Now that you understand what the accounting cycle is, let us walk through each stage in practical terms, with attention to how Finnish rules and SME realities shape your responsibilities.

-

Transaction identification: Every purchase, sale, payroll payment, and bank transfer must be identified as a financial event. In Finland, this includes VAT-liable sales, purchases with deductible VAT, and any transaction affecting your taxable income. Not every business event is a financial transaction, so this step requires judgement.

-

Journal entry: Once identified, each transaction is recorded as a journal entry. For companies using double-entry bookkeeping, every entry has a debit and a credit side. A sale of €1,000 plus VAT, for example, is recorded as a debit to accounts receivable and a credit to both the revenue and VAT payable accounts. Accuracy here prevents problems downstream.

-

Ledger posting: Journal entries are transferred to the relevant accounts in the general ledger. This is where your running totals for income, expenses, assets, and liabilities are maintained. Regular posting (weekly is ideal for most SMEs) prevents backlogs.

-

Trial balance: Before making adjustments, you prepare a trial balance to verify that total debits equal total credits. Errors here usually indicate a missed entry or a data input mistake. Catching this early saves significant effort later.

-

Adjusting entries: This is arguably the most critical step for Finnish SMEs. Adjustments account for accrued income, accrued expenses, prepayments, and depreciation. They ensure transactions are allocated to the period they relate to, not just when cash changes hands. Finland's accounting cycle mechanics are influenced by the entity's required bookkeeping method, and this directly affects how you capture timing differences, even though the goal of correct period reporting remains the same.

-

Financial statements: Using the adjusted trial balance, you prepare your income statement (profit and loss), balance sheet, and where required, a cash flow statement. These are the documents Vero.fi and other stakeholders rely on to assess your business.

-

Closing the books: Temporary accounts (income and expense accounts) are reset to zero so the new period starts fresh. Permanent accounts (assets, liabilities, equity) carry their balances forward. This step formally ends one cycle and begins the next.

Pro Tip: Pay extra attention to period-end reconciliation, particularly your accounts receivable, accounts payable, and bank statements. Reconciling monthly rather than only at year-end catches errors while they are still easy to fix and keeps your step-by-step bookkeeping on track throughout the year.

| Stage | Companies (double-entry accrual) | Self-employed (single-entry) |

|---|---|---|

| Journal entry | Full double-entry required | Income and expense log |

| Adjusting entries | Mandatory each period | Required for tax at year-end |

| Trial balance | Mandatory | Not formally required |

| Financial statements | Full set required | Simplified accounts |

| Closing the books | Formal reset of accounts | Year-end summary |

Following bookkeeping best practices at each stage reduces the risk of errors accumulating and makes each subsequent stage faster and more reliable.

Why timing and accruals matter: Critical points for SMEs

After walking through each stage, it is worth focusing on the element that causes the most confusion and the most compliance problems for Finnish SMEs: the timing of entries and adjustments.

Accrual accounting means you record income when it is earned and expenses when they are incurred, regardless of when cash actually moves. If you invoice a client in December but receive payment in January, that income belongs in December's financial statements under the accruals basis. If you pay for a year's insurance in June, only the portion relating to the current financial year is an expense for that year.

Getting this wrong is more common than most business owners realise. For SMEs, the "edge case" errors that trip up the accounting cycle are whether transactions belong in the current period or the next one. This is precisely why adjusting entries and period-end reconciliation are part of the cycle rather than optional extras.

Consider these real-world examples:

| Scenario | Incorrect treatment | Correct treatment |

|---|---|---|

| Invoice issued Dec, paid Jan | Record income in January | Accrue income in December |

| Insurance paid June (full year) | Expense full amount in June | Prepay 6 months, expense monthly |

| Salaries for Dec, paid Jan | Record as January expense | Accrue as December liability |

| Supplier invoice received Jan (Dec work) | Record in January | Accrue in December |

Each of these errors distorts your profit figure for the period. Cumulatively, they can significantly misrepresent your tax position.

"The 'edge case' that trips up the accounting cycle is whether transactions belong in the current period or the next one. This is why adjusting entries and period-end reconciliation are part of the cycle rather than optional." Investopedia

Pro Tip: Build a monthly cut-off checklist that covers outstanding invoices, unpaid supplier bills, prepaid expenses, and accrued payroll. Reviewing these items each month, rather than only at year-end, keeps your bookkeeping workflow clarity intact and prevents surprises when it matters most.

Getting the timing right protects you at tax time, gives you reliable figures for business decisions, and reduces the likelihood of queries from Vero.fi. It is one of the most practical investments of attention you can make as an SME owner.

From closing the books to filing: Compliance deadlines and preparing financial statements

Once the books are closed for a financial year, the focus shifts to producing compliant financial statements and meeting statutory deadlines. This is where the accounting cycle connects directly to your legal obligations as a Finnish business.

The closing step involves making final adjusting entries, completing reconciliations, and formally transferring temporary account balances. Only once this is complete can you produce financial statements that accurately reflect the year's activity.

Key Finnish compliance deadline: In Finland, financial statements must be prepared within four months of the end of the financial year. For businesses with a 31 December year-end, this means financial statements must be ready by 30 April at the latest. Missing this deadline can result in penalties and complications with your tax filing.

Supporting documents that you typically need alongside your financial statements include:

- General ledger: The complete record of all transactions for the year

- Bank reconciliations: Confirming that your records match your bank statements

- VAT reports: Matching your declared VAT to your ledger entries

- Fixed asset register: Documenting depreciation calculations

- Accounts receivable and payable listings: Outstanding amounts at year-end

- Loan and liability schedules: Confirming balances owed

Your compliance steps following the cycle should proceed in this order:

- Complete all adjusting entries and reconciliations

- Prepare and review the adjusted trial balance

- Produce the income statement, balance sheet, and cash flow statement

- Have financial statements reviewed or audited if required

- File your corporate income tax return within the applicable deadline

- Archive all supporting documents for the legally required retention period (in Finland, this is generally six years)

Understanding the financial report requirements that apply to your specific entity type will help you prepare more efficiently. Reviewing financial statement examples relevant to Finnish entrepreneurs can also clarify what the finished product should look like and what level of detail is expected.

The four-month window is tighter than many business owners realise, particularly if your year-end is busy. Starting the closing process early, ideally in the final weeks of your financial year, makes a significant difference to the quality and timeliness of your statements.

Why mastering the accounting cycle is a business superpower for Finnish SMEs

Most SMEs view the accounting cycle as an obligation, a process to get through so they can focus on running their business. We understand this perspective, but it misses something important.

When your accounting cycle is working correctly, it becomes your financial control dashboard. You know your current cash position, which clients owe you money, what expenses are coming up, and whether your business is actually profitable in the current period. That clarity is not just useful for tax filing. It informs decisions about hiring, investment, pricing, and how much you can draw from the business.

Here is the contrarian view that experience has taught us: SMEs who invest time up front in building good cycle discipline almost always spend less overall on problem-solving, error correction, and professional fees. Businesses that manage their cycle reactively tend to face higher accountant costs because their books require more clean-up before anything useful can be done. The discipline is not additional work; it replaces more stressful, more expensive work later.

There is also a less discussed benefit. When your accounting cycle is clean and consistent, your accountant can focus on higher-value work: tax planning, identifying deductions, advising on structure, and helping you grow. A well-maintained bookkeeping for compliance and success approach gives your adviser the reliable data they need to provide genuinely strategic input, rather than spending most of their time correcting transactional errors.

Pro Tip: Treat your monthly close not as an administrative chore but as a brief financial health check. Fifteen to thirty minutes reviewing your trial balance and outstanding items each month is one of the highest-return habits an SME owner can develop.

The SMEs we see navigating tax time with the least stress are not necessarily the ones with the simplest financial situations. They are the ones with consistent, well-maintained accounting cycles. That discipline is entirely learnable and within reach for any business owner willing to prioritise it.

Professional support for your accounting cycle in Finland

Understanding the accounting cycle is an excellent starting point. Implementing it correctly, consistently, and in compliance with Finnish regulations is where professional support makes a real difference.

We work with Finnish SMEs and entrepreneurs at every stage of the accounting cycle, from setting up a reliable bookkeeping process to preparing compliant financial statements on time. Our services are designed to reduce your administrative burden, eliminate compliance risk, and give you the financial clarity you need to run your business with confidence. Whether you are a registered company or operating as a light entrepreneur, we offer bookkeeping packages tailored to your situation. If you are ready to put your accounting cycle on a solid footing, explore our full range of services and get in touch to discuss how we can support you.

Frequently asked questions

Is the accounting cycle mandatory for all business types in Finland?

Yes, but the requirements differ by entity type. Finnish companies must use double-entry bookkeeping on an accruals basis, while self-employed individuals may use single-entry bookkeeping with accrual adjustments for tax purposes at year-end.

How long after year-end do Finnish SMEs have to file financial statements?

Financial statements must be prepared within four months of the end of the financial year, so a 31 December year-end means statements are due by 30 April.

What is the most common accounting cycle mistake SMEs make?

The most common mistake is misallocating transactions to the wrong period. As Investopedia notes, these timing errors are a major pitfall for SMEs, which is why adjusting entries and period-end checks are essential rather than optional.

Do SMEs need software or can the accounting cycle be managed manually?

Manual bookkeeping is legally permitted in Finland, but accounting software significantly reduces the risk of errors, makes adjusting entries easier to manage, and speeds up the process of producing financial statements. For most SMEs, the efficiency gains more than justify the cost.