TL;DR:

- Not all business expenses are deductible in Finland; proper documentation and clear business purpose are essential.

- Entrepreneurs must accurately track, categorize, and retain receipts to maximize deductions and ensure compliance.

- Misunderstanding rules, poor recordkeeping, or claiming non-deductible expenses can lead to audits, penalties, and lost savings.

Many entrepreneurs assume that if they spend money on their business, they can deduct it from their taxes. In Finland, that assumption can be costly. Strict rules mean not all business expenses are deductible, and misunderstanding the boundaries leads to missed savings or, worse, compliance issues with the Finnish Tax Administration. Whether you run a sole trader business, operate as a light entrepreneur, or manage a small company, knowing exactly which expenses qualify, how to document them, and where the exceptions lie is essential. This guide walks you through the key rules, practical categories, and strategies to help you maximise your deductions confidently.

Table of Contents

- What qualifies as a deductible expense

- How to track and report deductible expenses

- Nuances, exceptions and edge cases

- Non-deductible expenses and compliance risks

- What most entrepreneurs overlook about deductible expenses

- Your next step: Professional help for optimal deductions

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Strict definition applies | Only expenses directly linked to income production and business operations are deductible in Finland. |

| Documentation is critical | Receipts, logbooks and business/private separation protect deductions and safeguard against audits. |

| Certain costs are excluded | Personal spending, fines, and full entertainment expenses are not deductible and may trigger compliance risks. |

| Limits for asset deductions | Low-value assets can be deducted up to €1,200/item and €3,600/year immediately. |

| Expert support boosts compliance | Professional advice and tools help entrepreneurs maximise deductions while ensuring full legal compliance. |

What qualifies as a deductible expense

Having highlighted the critical importance and misconceptions around deductible expenses, let us break down what actually qualifies under Finnish tax rules.

Deductible expenses are those directly related to business activities and income production. If an expense helps you generate revenue, it is likely deductible. If it primarily benefits you personally, it is not. That distinction sounds straightforward, but it causes considerable confusion in practice.

Common categories of deductible expenses include:

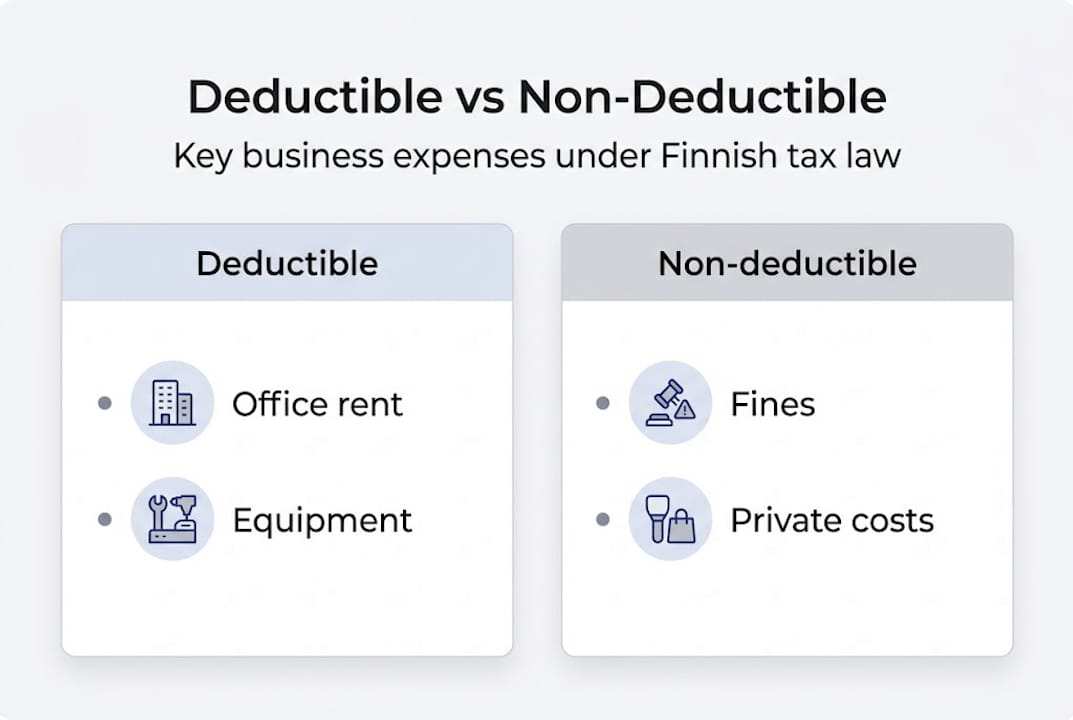

- Office costs: Rent, utilities, and supplies used exclusively for business

- Travel: Business trips, client visits, and mileage at the approved rate

- Equipment: Computers, tools, machinery, and software used for work

- Marketing: Advertising, website costs, and promotional materials

- Insurance: Professional liability and business-related insurance premiums

- Professional fees: Accounting, legal, and advisory services

- Training: Courses and materials directly relevant to your current work

For every expense you claim, you need a receipt and a clear business reason. The Finnish Tax Administration expects you to demonstrate a direct connection between the cost and your income-producing activities. Vague or undocumented claims are the most common reason deductions get rejected during a review. Reviewing essential tax tips for Finnish entrepreneurs can help you avoid those pitfalls from the start.

One rule worth knowing immediately: low-value assets can be deducted in full in the year of purchase, rather than depreciated over several years. The current limits are €1,200 per item and €3,600 in total per year. Assets above these thresholds must be depreciated according to Finnish tax law. Understanding accounting methods examples helps you decide which approach applies to your purchases.

Here is a quick comparison to clarify the difference between fully and partially deductible expenses:

| Expense type | Deductibility | Notes |

|---|---|---|

| Office rent (dedicated space) | Fully deductible | Must be used solely for business |

| Business travel costs | Fully deductible | Receipts and logs required |

| Mobile phone (mixed use) | Partially deductible | Business proportion only |

| Home internet (mixed use) | Partially deductible | Estimate business share accurately |

| Client entertainment | Partially deductible | 50% limit applies |

| Normal clothing | Not deductible | No exceptions for standard attire |

For a broader breakdown of deductible business expenses under Finnish corporate tax rules, it is worth reviewing the guidance from a qualified source.

Pro Tip: Keep a simple spreadsheet that categorises each expense as fully deductible, partially deductible, or personal. Doing this monthly saves hours at tax time and reduces errors significantly.

How to track and report deductible expenses

Once you understand what qualifies, it is vital to track, document, and report your deductible expenses correctly to stay compliant and optimise savings.

Sole traders report deductions in a business tax return, must keep receipts and invoices, and file via MyTax. The deadline for the 2025 tax year is 1 April 2026. Missing this deadline can result in penalties and lost deductions, so planning ahead matters.

Here is a practical step-by-step process for tracking and reporting your deductions:

- Collect receipts immediately. Save every receipt, whether digital or paper, at the point of purchase. Use a dedicated folder or accounting app.

- Log the business purpose. For each expense, note why it was incurred and how it relates to your income. This is especially important for travel and entertainment.

- Separate business and personal finances. Use a dedicated business bank account and card. Mixing personal and business transactions is one of the most common audit triggers.

- Categorise expenses monthly. Do not leave this until year-end. Monthly categorisation keeps your records accurate and manageable.

- Calculate depreciation where needed. For assets above the low-value threshold, apply the correct depreciation rate under Finnish tax law.

- File via MyTax. Log in to the Finnish Tax Administration's MyTax portal, complete your business tax return, and submit deductions with supporting documentation.

For VAT-registered businesses, there is an additional layer: you can reclaim the VAT portion of business expenses, but only for purchases used in VAT-liable activities. Keeping VAT records separate from income tax records avoids confusion and errors. Reviewing tax deductions overview in Finnish provides further detail on VAT-related deductions.

| Record type | Minimum retention period | Format accepted |

|---|---|---|

| Receipts and invoices | 6 years | Paper or digital |

| Travel logs | 6 years | Written or electronic |

| Bank statements | 6 years | Digital copies accepted |

| Asset purchase records | Life of asset + 6 years | Paper or digital |

Solid bookkeeping basics for small businesses in Finland underpin every successful deduction claim. If your records are incomplete, even legitimate deductions can be disallowed. Building tax compliance essentials into your monthly routine removes the last-minute stress entirely.

Pro Tip: Set a recurring calendar reminder on the first day of each month to reconcile your business expenses. Thirty minutes monthly prevents a thirty-hour scramble in March.

Nuances, exceptions and edge cases

Beyond the routine categories, there are many exceptions and nuanced rules entrepreneurs need to master to avoid costly errors.

Mixed-use assets such as a phone or internet connection are only partially deductible, based on the business proportion of use. Home office costs follow a similar logic: you can deduct them only if the space is used regularly and primarily for business. A kitchen table used occasionally for emails does not qualify. A dedicated room used daily for client work does.

Here are some of the most commonly misunderstood edge cases:

- Protective clothing: Deductible if required for safety or hygiene reasons specific to the job. Normal clothing, even if worn only for work, is not deductible.

- Start-up costs: Expenses incurred before you received your Business ID can still be deducted, provided they were genuinely aimed at establishing the business. This is a valuable rule many new entrepreneurs miss. See the starting a business guide for more context.

- Light entrepreneurs: If you invoice through a light entrepreneur platform, your deductions are simplified. You can claim travel at €0.27 per kilometre for 2026. However, a recent Supreme Court ruling confirmed that invoicing service fees paid to platforms are not deductible as business expenses.

- Research and development: Finland offers an enhanced R&D deduction for qualifying costs, which can significantly reduce taxable income for innovative businesses.

Important: For mixed-use items, you must estimate the business proportion honestly and consistently. The Finnish Tax Administration can request evidence of how you calculated the split. Vague estimates invite scrutiny.

Reviewing bookkeeping best practices for Finnish small businesses helps you build the habits needed to handle these nuances without confusion. Getting the split right on mixed-use items alone can save you a meaningful amount each year.

Pro Tip: Create a simple usage log for any mixed-use asset. Record business versus personal use weekly for one month, then use that ratio as your annual estimate. It is defensible, practical, and quick.

Non-deductible expenses and compliance risks

Understanding the boundaries of deductible expenses helps minimise compliance risk and ensures your business does not fall foul of Finnish tax authorities.

No deduction is allowed for fines, private expenses, normal clothing, full entertainment costs, or voluntary pension contributions made outside approved schemes. These are firm boundaries, not grey areas.

Common non-deductible expenses include:

- Traffic fines and penalties: Regardless of whether they occurred during business travel

- Private living costs: Food, personal clothing, household expenses

- Gifts above the threshold: Client gifts over €25 per person per year are not deductible

- Full entertainment costs: Only 50% of qualifying entertainment expenses are deductible

- Voluntary pension contributions: Unless made through a specifically approved arrangement

- Costs unrelated to income production: Any expense without a clear business purpose

The compliance risks of claiming non-deductible expenses are real. The Finnish Tax Administration conducts targeted audits, and incorrect deductions can result in back taxes, interest charges, and administrative penalties. You can also optimise capital tax planning to reduce your overall burden, but only if your deduction records are clean.

The scale of the problem in Finland is significant. Grey economy losses from false entries in small and medium-sized companies amount to approximately €120 million per year in lost corporate tax. The Tax Administration's own audit data shows that after a tax audit, net profit rises by an average of €72,000 per year per company. That figure reflects how much incorrect deduction behaviour costs businesses when it is eventually corrected.

"After a tax audit, the average company's net profit increases by €72,000 per year, reflecting the scale of deduction errors across Finnish SMEs."

Working with a qualified tax advisor reduces this risk substantially. Proactive compliance is always less expensive than reactive correction.

What most entrepreneurs overlook about deductible expenses

Most entrepreneurs focus on learning the rules. Fewer focus on applying them consistently. That gap is where real money is lost.

Documentation is the true foundation of every successful deduction claim. You can know every rule perfectly and still lose deductions if your records are incomplete or ambiguous. The Finnish Tax Administration does not reward good intentions. It rewards accurate records.

The business and private expense separation is not optional. It is a legal requirement. Ambiguity in this area is the single most common reason audits result in additional tax assessments. Keeping finances clearly separated from day one protects you.

Proactive tax planning, rather than reactive filing, is where the real advantage lies. Entrepreneurs who review their deduction position quarterly, plan asset purchases around the €1,200 low-value threshold, and consider R&D claims before year-end consistently pay less tax. The rules reward preparation. Working with an accountant who understands Finnish tax law means subtle opportunities, like pre-Business ID start-up costs or enhanced R&D deductions, do not get missed. Small details, applied consistently, produce meaningful outcomes over time.

Your next step: Professional help for optimal deductions

If you are ready to optimise your business deductions, expert guidance could make all the difference.

Navigating Finnish tax rules on your own takes time and carries risk. Missed deductions and compliance errors both cost money, often more than the cost of professional support.

At Finovate, we support entrepreneurs, sole traders, and light entrepreneurs with accounting, bookkeeping, and tax planning tailored to Finnish rules. Whether you need our invoicing service pro for straightforward invoicing or dedicated accounting for light entrepreneurs, we have the right solution for your situation. Let us help you claim every deduction you are entitled to, stay compliant, and approach next tax season with confidence.

Frequently asked questions

How do I prove a business expense is deductible in Finland?

You must show a clear connection to income production, provide receipts and logs, and use accurate bookkeeping as required by Finnish tax authorities. Receipts and a clear business nexus are both essential.

Can I deduct home office expenses as an entrepreneur?

Home office costs are deductible if the space is used regularly for business purposes under Finnish rules. You must meet the specific conditions and document your usage clearly.

What expenses are never deductible?

Private expenses, fines, normal clothing, and full entertainment costs over the 50% limit are not deductible under Finnish business tax rules.

What are the limits for low-value asset deductions?

Low-value assets are immediately deductible up to €1,200 per item and €3,600 total per year according to current Finnish tax guidelines.

When is the deadline for filing deductible expenses for 2025?

The deadline is 1 April 2026 for filing your deductible expenses for the 2025 tax year in Finland.