TL;DR:

- Capital income in Finland includes dividends, interest, rental income, and part of sole trader profits.

- It is taxed at flat rates of 30% up to €30,000 and 34% above that threshold.

- Strategic structuring and timely decisions can optimize tax outcomes for entrepreneurs.

Not all business income in Finland is taxed the same way. Many entrepreneurs assume their profits face the same progressive rates as a salaried employee's wages, but capital income works quite differently. In Finland, capital income is taxed separately from earned income at flat rates of 30% up to €30,000 and 34% above that threshold. This distinction matters enormously for how you structure your business and time your financial decisions. This guide will help you identify what qualifies as capital income, understand how it is calculated, and apply practical strategies to optimise your tax position with confidence.

Table of Contents

- What is capital income? Key types for Finnish entrepreneurs

- How capital income is taxed in Finland: rates, rules, and examples

- Deductions and relief: how to lower capital income tax

- 2026 changes and special cases: what's new for entrepreneurs?

- Optimisation strategies: how to structure and time your capital income

- Why capital income strategies matter more than many realise

- Get expert support to optimise your capital income tax

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Capital income taxed separately | In Finland, capital income is taxed at flat rates, offering optimisation opportunities for entrepreneurs. |

| Deduct valid expenses | You can reduce taxable capital income by deducting interest, maintenance, depreciation, and certain losses. |

| Strategic structuring matters | Choosing the right split or company form can lower your effective tax and maximise wealth. |

| 2026 brings new rules | Bank bonuses and stricter compliance for refunds and share swaps are key changes requiring prompt action. |

What is capital income? Key types for Finnish entrepreneurs

Capital income is income that arises from wealth or assets rather than from your personal labour. It stands apart from earned income, which covers salaries, wages, and the portion of sole trader profit attributed to your personal work effort. Understanding this boundary is the starting point for any sound tax strategy.

"Capital income includes dividends, interest, rental income, capital gains, and more for entrepreneurs."

According to Vero's income classifications, the Finnish Tax Administration recognises a broad range of capital income sources. For entrepreneurs, the most relevant categories include:

- Dividends received from company shareholdings

- Capital gains from selling shares, property, or other assets

- Rental income from property you own

- Interest income from loans or deposits

- Bank loyalty bonuses (taxable as capital income from 2026 onwards)

- The capital portion of sole trader business profit, calculated from net business assets

As Quickbooks Finland tax tables confirm, capital income for entrepreneurs comprises dividends, interest, rental income, capital gains, and the calculated capital portion of sole trader income. This last point often surprises business owners. If you operate as a sole trader, a defined share of your annual profit is reclassified as capital income rather than earned income, which can reduce your overall tax burden depending on your circumstances.

For broader context on managing these categories efficiently, our tax tips for Finnish entrepreneurs offer a practical starting point.

How capital income is taxed in Finland: rates, rules, and examples

Now that you know what is included, let us see how these types of income are actually taxed.

The flat rate on capital income is 30% on amounts up to €30,000 and 34% on any amount above that. This contrasts with earned income, which is subject to progressive national and municipal tax rates that can exceed 50% for higher earners. For many entrepreneurs, this makes capital income structurally more efficient.

For sole traders, the rules are specific. The capital portion of business income is calculated as 20% of the prior year's net business assets, though you may optionally elect a 10% rate instead. The remainder of your profit is treated as earned income and taxed progressively.

Comparison: sole proprietorship vs. limited company capital taxation

| Feature | Sole proprietorship | Limited company (Oy) |

|---|---|---|

| Capital income rate | 30% / 34% (flat) | 20% corporate tax, then 30% / 34% on dividends |

| Capital split basis | 20% or 10% of net assets | Dividend distribution decision |

| Earned income tax | Progressive | Salary set by owner |

| Flexibility | Moderate | High |

Here is a simple example. Suppose your net business assets at the end of the prior year were €50,000. Using the 20% rate, €10,000 of your current year profit is treated as capital income and taxed at 30%. The remaining profit is taxed as earned income at your marginal rate. This can produce meaningful savings if your earned income rate is high.

Pro Tip: If your marginal earned income tax rate is relatively low, electing the 10% capital split may result in more income being taxed at the lower progressive rate rather than the flat 30%, which could work in your favour. Review this annually with reference to tax compliance in 2026 requirements.

For detailed filing instructions for self-employed individuals, Vero provides clear guidance on how to report these splits correctly.

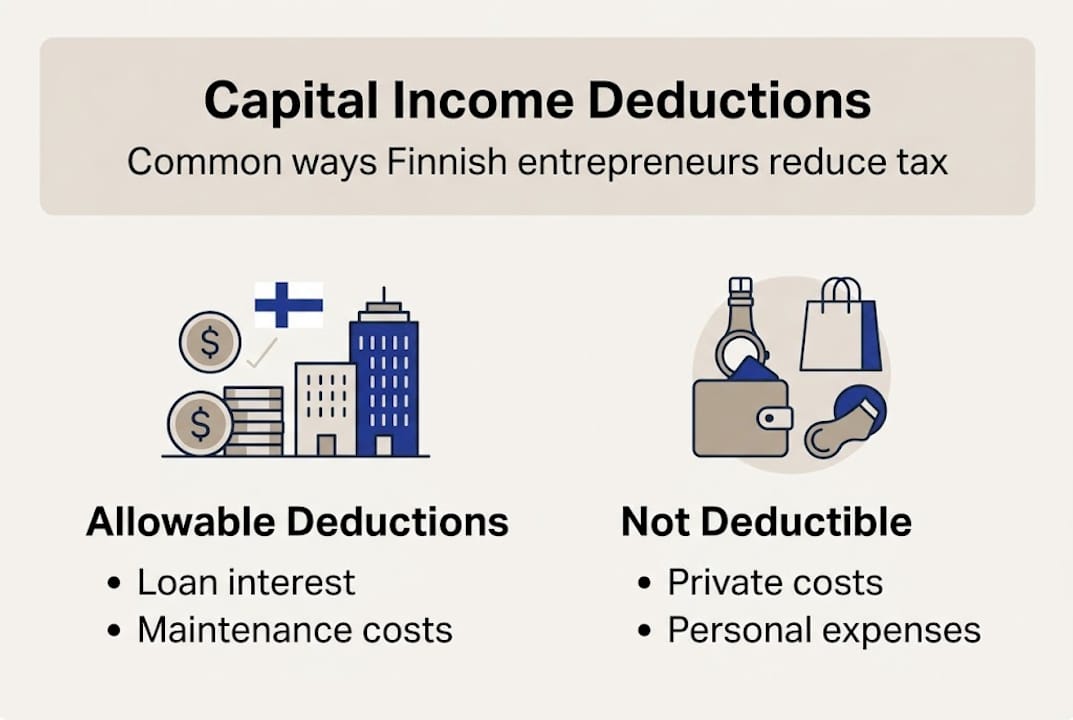

Deductions and relief: how to lower capital income tax

Understanding the rates is vital, but smart deductions can make a real difference to your final tax bill.

Finnish tax law allows a range of deductions against capital income. Allowable deductions include interest on loans used to acquire income-producing assets, maintenance and repair costs for rental property, depreciation on furnishings and fixtures, and capital losses that can be offset against capital gains over up to five years. These rules apply on a paid basis, meaning you claim them in the year you actually pay the expense.

Deductible vs. non-deductible items for common capital income categories

| Category | Deductible | Not deductible |

|---|---|---|

| Rental property | Loan interest, repairs, depreciation | Personal use costs, capital improvements (in full) |

| Share investments | Capital losses (offset over 5 years) | Personal financial advice fees |

| Business assets | Depreciation, maintenance | Private expenses mixed with business |

Common errors made by small business owners when claiming deductions include:

- Claiming personal expenses as business or investment costs

- Forgetting to carry forward capital losses from previous years

- Missing the deadline to report rental income deductions

- Failing to track loan interest attributable to income-producing assets

- Overlooking depreciation on property furnishings

Pro Tip: Keep a dedicated record of all capital income related expenses throughout the year. When you have a capital loss, register it promptly so it can be offset against future gains within the five-year window. Our guidance on accounting for freelancers covers practical record-keeping methods that apply equally to sole traders.

For a thorough overview of rental and capital gains tax rules, specialist resources can help you avoid costly mistakes.

2026 changes and special cases: what's new for entrepreneurs?

Beyond typical income and deductions, some 2026 rule changes and niche scenarios require special attention.

"2026 introduces expanded definitions and enhanced compliance for capital income."

The Finnish Tax Administration has confirmed that bank loyalty bonuses become capital income from 2026, alongside tighter scrutiny of capital refunds from non-listed companies and share swaps under the 10-year rule for capital gains. These changes affect a wider group of entrepreneurs than many realise.

Key compliance changes that affect entrepreneurs in 2026:

- Bank loyalty bonuses must now be reported as capital income, with banks providing annual information returns to Vero.

- Capital refunds from non-listed companies are subject to stricter classification rules, potentially triggering capital gains tax rather than a tax-free return of capital.

- Share swaps face enhanced reporting requirements, particularly where transactions occurred within the past 10 years.

- Crypto and digital assets continue to be treated as capital gains on disposal, with no new exemptions introduced.

- Reporting deadlines for certain investment income have been tightened, so early preparation is essential.

For entrepreneurs managing complex ownership structures, reviewing the capital refunds instructions from Vero is a practical first step. Our article on accounting methods for entrepreneurs also addresses how to align your bookkeeping with these updated requirements.

Optimisation strategies: how to structure and time your capital income

With compliance covered, let us see how to proactively shape your tax outcomes.

Structuring and timing your capital income decisions can have a significant impact on what you actually pay. Entrepreneurs may opt for the 10% capital split to reduce tax if their earned income rate is lower, time asset sales to benefit from the €1,000 annual exemption on small gains, and use equity savings accounts to defer personal tax on investment returns.

Scenario-based tips for typical Finnish SME owners:

- Asset-heavy sole traders should calculate both the 10% and 20% capital splits each year to identify which produces the lower combined tax bill.

- Property investors should time repairs and maintenance payments to maximise deductions in high-income years.

- Shareholders in limited companies should consider the timing of dividend distributions relative to the €30,000 threshold to stay within the lower 30% band.

- Entrepreneurs selling business assets should check whether the gain falls below the €1,000 exemption before reporting.

- Those with investment portfolios should use equity savings accounts where possible to defer tax on returns until withdrawal.

Pro Tip: If your business is growing and accumulating significant assets, a limited company structure may allow you to retain profits within the company at the 20% corporate tax rate, deferring personal capital income tax until you choose to distribute. Explore the full picture of SME accountant benefits before making structural decisions.

For further context on how private trader taxation compares with limited company structures, OP's guidance provides a useful reference.

Why capital income strategies matter more than many realise

Flat tax rates on capital income sound straightforward and, for many entrepreneurs, they are genuinely attractive. But the assumption that capital income is always the more efficient route can lead to poor decisions, particularly for asset-light businesses.

As flat capital tax rates provide predictability, sole proprietor capital splits may actually disadvantage businesses with fewer assets. If your net assets are modest, the capital portion of your profit will be small, meaning most of your income is still taxed as earned income regardless. In these cases, spending time optimising the capital split delivers less value than focusing on allowable deductions or reviewing your business structure altogether.

We have seen small firms invest considerable effort in calculating the capital split only to find the tax saving is negligible. The more productive question is whether your current business structure still fits your financial goals.

"A review of your capital income strategy can mean the difference between compliance and missed opportunities."

Regular review matters. Tax rules change, your asset base evolves, and the optimal structure today may not be optimal in three years. We encourage you to revisit your approach annually, particularly in light of 2026 changes. Our overview of accounting service options can help you identify where professional support adds the most value.

Get expert support to optimise your capital income tax

Practical advice can get you started, but specialist support ensures you maximise tax efficiency year after year.

Navigating capital income taxation in Finland involves multiple moving parts: choosing the right capital split, tracking deductions, adapting to new rules, and structuring your business for long-term efficiency. Getting this right consistently requires more than a once-a-year review.

At Finovate, we provide accounting, tax planning, and financial advisory services tailored to Finnish entrepreneurs and small business owners. Whether you need support with annual tax filings, bookkeeping, or a full review of your business structure, we are here to help. Our Invoicing Service Pro and light entrepreneur accounting packages are designed to make compliance straightforward and your tax position as efficient as possible. Reach out to us today to discuss your specific situation.

Frequently asked questions

How is capital income calculated for Finnish sole proprietors?

The portion of business profit classified as capital income is normally 20% of prior year net assets, or optionally 10% if that produces a more favourable outcome for you.

What are the main deductions from capital income in Finland?

Allowable deductions include loan interest, property maintenance, depreciation, and capital losses offset against gains for up to five years.

Are dividends from my limited company capital income?

Yes, dividends paid to individual shareholders are taxed as capital income at 30% up to €30,000 and 34% on any amount above that threshold.

How do 2026 rule changes impact capital income taxation?

From 2026, bank loyalty bonuses are taxable as capital income and stricter rules apply to capital refunds and share swaps, affecting how and when you report these items.

When should I consider changing from sole proprietorship to a limited company?

If you have significant business assets or want to defer personal tax on profits, a limited company structure may offer greater capital income optimisation through the 20% corporate tax rate and flexible dividend timing.