TL;DR:

- The financial reporting workflow transforms raw data into accurate, compliant reports through structured, sequential steps. Following each phase without skipping ensures timely, error-free reports and better stakeholder communication. Proper tools, clear procedures, and disciplined execution are essential for efficient financial reporting processes.

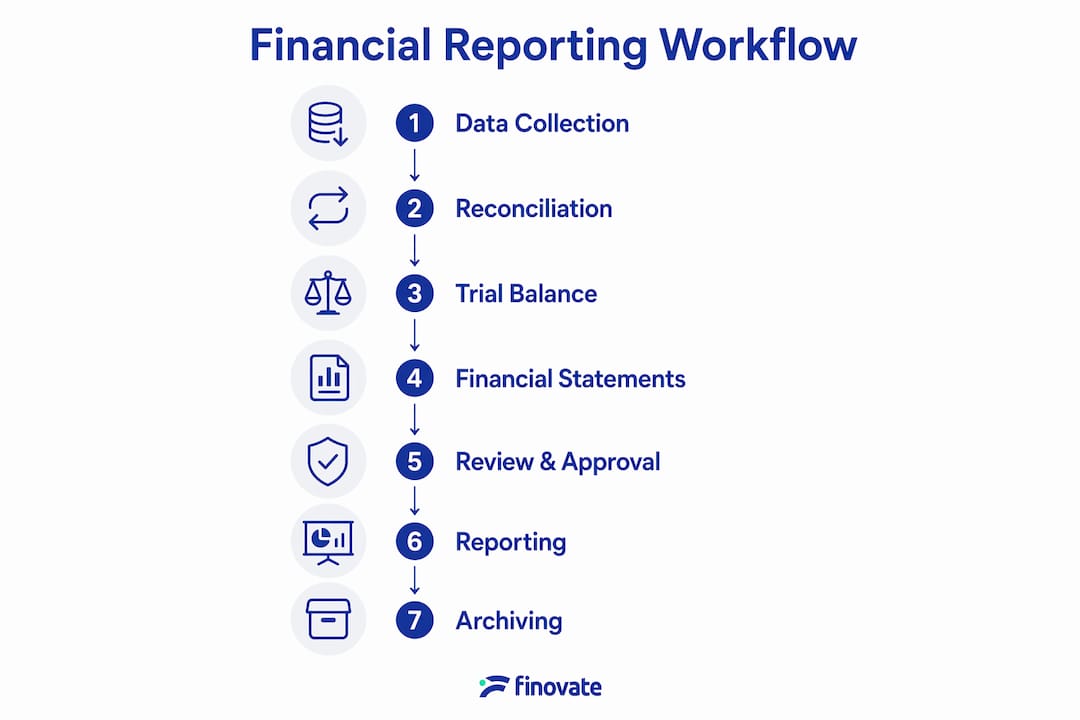

The financial reporting process workflow is the structured sequence of steps that transforms raw financial data into accurate, compliant reports delivered to stakeholders. Also known as the record-to-report (R2R) cycle, this process covers everything from initial data collection through to final distribution and archiving. Business owners and finance managers who master this sequence gain better control over close timelines, reduce errors, and meet compliance obligations with confidence. Getting it right requires the right tools, clear role assignments, and a disciplined approach to each phase.

What are the core phases of the financial reporting process workflow?

The financial reporting workflow steps typically span 5–8 sequential phases, each depending on the successful completion of the one before it. Rushing or skipping a phase does not save time. It creates errors that compound downstream and force costly rework.

The phases follow this order:

- Data collection. Gather all transaction records, bank statements, invoices, and payroll data from source systems. Incomplete data at this stage contaminates every subsequent step.

- Journal entry posting. Record all accruals, prepayments, and adjustments in your accounting system. Every entry requires supporting documentation.

- Reconciliation. Match ledger balances against bank statements, supplier accounts, and intercompany balances. This is the most labour-intensive phase and the most consequential.

- Adjustments. Post any correcting entries identified during reconciliation. Adjustments must be approved before the ledger is considered clean.

- Consolidation. For businesses with multiple entities, combine individual ledgers into a single group view, eliminating intercompany transactions.

- Financial statement preparation. Produce the income statement, balance sheet, and cash flow statement from the consolidated ledger.

- Review and sign-off. An independent reviewer checks the narrative and reasonableness of figures before distribution.

- Distribution and archiving. Deliver reports to stakeholders and lock the period immediately.

The R2R lifecycle is a seven-phase sequential process where each phase depends on the completion and validation of the prior one. That dependency is not a formality. A reconciliation left open on day two will delay every phase that follows. In a typical month-end close, the core close occupies days 1–3, with reporting and distribution occurring on days 4–5.

| Phase | Owner | Deadline | Automation potential |

|---|---|---|---|

| Data collection | Finance team | Day 1 | High (ERP feeds) |

| Journal posting | Accountant | Day 1–2 | Medium (templates) |

| Reconciliation | Finance manager | Day 2–3 | High (auto-match) |

| Adjustments | Senior accountant | Day 3 | Low (judgement required) |

| Consolidation | Group finance | Day 3–4 | High (consolidation tools) |

| Statement preparation | Finance manager | Day 4 | Medium (reporting tools) |

| Review and sign-off | Independent reviewer | Day 4–5 | Low (qualitative) |

| Distribution and archiving | Finance team | Day 5 | Medium (scheduled delivery) |

What tools and preparations does an efficient reporting workflow require?

The financial report preparation process runs on two foundations: clear standard operating procedures (SOPs) and the right technology. Formal SOPs reduce manual extraction time and errors, particularly in complex ERP environments. Without documented procedures, each close cycle depends on individual memory rather than repeatable process.

The core tools that support the workflow include:

- ERP software such as SAP, Oracle NetSuite, or Microsoft Dynamics 365 for centralised transaction recording and automated feeds.

- Automated reconciliation tools that match transactions against bank data without manual intervention.

- Reporting dashboards built in tools such as Power BI or Tableau for management-level visibility.

- AI-assisted variance analysis that flags period-over-period movements and drafts initial commentary.

- Collaboration platforms such as Microsoft Teams or Slack for structured handoff communication between team members.

Aligning your reporting outputs with your audience matters as much as the tools themselves. Management dashboards require high-level KPIs and trend lines. Statutory reports require full disclosure and supporting schedules. Producing one format for all audiences wastes time and reduces clarity.

| Tool or preparation | Benefit | Typical user |

|---|---|---|

| ERP system | Centralises data, reduces manual entry | Finance team |

| Automated reconciliation | Cuts reconciliation time significantly | Accountant |

| Reporting dashboard | Delivers real-time visibility | Finance manager, board |

| SOPs documentation | Ensures consistency across close cycles | All finance staff |

| Collaboration platform | Reduces handoff delays | Cross-functional teams |

Pro Tip: Archive all working papers in a structured, secure folder immediately after each period closes. Locking periods promptly prevents retrospective changes and preserves a clean audit trail for future reviews or external audits.

How to execute each workflow step effectively and avoid common pitfalls

Execution quality determines whether your close cycle runs to schedule or collapses under rework. The most common source of delay is not technical complexity. Workflow delays most often stem from manual handoffs and poor communication between departments rather than system failures.

Follow these execution steps to keep each phase on track:

- Lock your data sources early. Set a clear cut-off time for transaction submissions from operational teams. Late entries after cut-off should require formal approval.

- Use standardised journal templates. Pre-built templates with mandatory fields reduce posting errors and speed up review.

- Reconcile in priority order. Start with bank accounts and high-value ledgers. Resolve differences before moving to lower-value accounts.

- Document every adjustment. Each correcting entry needs a reason code and an approver. Undocumented adjustments are a red flag in any audit.

- Tie out your statements. Upstream task completion directly affects downstream reliability. Confirm that net profit flows correctly from the income statement through retained earnings to the balance sheet, and that the cash flow statement reconciles to the closing bank balance.

- Conduct a structured review. The reviewer checks for narrative coherence and reasonableness, not arithmetic. If the numbers tell a story that does not match the business reality, that is the signal to investigate.

- Distribute on schedule. Late reports erode stakeholder confidence. Set automated delivery where possible.

- Archive and lock immediately. Close the period in your system the moment distribution is confirmed.

The tie-out step in point five is where many teams lose time. A mismatch between the income statement and the cash flow statement signals an error somewhere upstream. Tracing it back through the ledger is far more time-consuming than preventing it through disciplined reconciliation.

Pro Tip: Assign your review step to someone who did not prepare the report. Independent review focuses on the defensibility and narrative of the financial story rather than recalculating figures. This catches errors that preparers miss through familiarity.

What best practices improve financial reporting quality and speed?

Workflow management in finance has shifted from manual effort to structured automation over the past decade. The most effective teams treat their close process as a repeatable system, not a monthly scramble. Automation and standardisation remain the primary levers for reducing month-end close times and maintaining high accuracy.

The best practices that consistently deliver results include:

- Standardise every recurring task. Use templates for journals, reconciliations, and commentary. Consistency reduces review time and makes training new staff faster.

- Automate data feeds. Connect your ERP directly to source systems so transaction data flows without manual extraction.

- Use AI for variance commentary. AI tools can draft initial explanations for period-over-period movements, freeing finance staff to focus on interpretation rather than description.

- Implement period locking. Lock closed periods in your accounting system immediately. Retrospective changes are a compliance risk and an audit concern.

- Maintain a close calendar. Publish deadlines for every phase at the start of each period. All stakeholders, including operational teams supplying data, should know their cut-off dates.

- Review your process quarterly. Identify which phases consistently run late and address the root cause, whether that is a data supplier, a system limitation, or a staffing gap.

Finance teams are shifting from manual data generation to financial intelligence by explaining period-over-period variances to operational leaders for strategic insight. That shift requires the workflow to produce not just accurate numbers but meaningful commentary. The close process is no longer just a compliance exercise. It is a communication tool.

Common bottlenecks and their solutions:

- Late data from operations: Set automated reminders and escalation paths for missed cut-offs.

- Reconciliation backlogs: Implement automated matching tools and daily reconciliation habits rather than leaving everything to month-end.

- Review delays: Schedule the review slot in advance and provide the reviewer with a summary pack, not just raw statements.

How do different financial reports serve different stakeholder needs?

Effective financial reporting requires integration of supporting schedules, variance commentary, and management dashboards tailored to specific audiences. Producing a single report format for all stakeholders is a common mistake. A board member needs a one-page KPI summary. An auditor needs full disclosure with supporting schedules. A lender needs cash flow projections and covenant compliance data.

The four core report types and their audiences are:

| Report type | Primary audience | Key purpose |

|---|---|---|

| Income statement | Management, board | Assess profitability and cost control |

| Balance sheet | Lenders, auditors, board | Evaluate financial position and solvency |

| Cash flow statement | Management, lenders | Monitor liquidity and cash generation |

| KPI dashboard | Management, operational leads | Track performance against targets |

Each report type draws from the same underlying ledger but presents data at a different level of detail. The income statement and balance sheet feed directly into the cash flow statement through the indirect method. That interdependency is why the tie-out step in execution matters so much. A financial report that is internally inconsistent will raise questions from every audience it reaches.

Management commentary transforms numbers into decisions. A revenue variance of 12% means nothing without context. With a clear explanation referencing a specific client delay or a seasonal pattern, it becomes information that operational leaders can act on. Tailoring that commentary to the audience's level of financial literacy is part of the workflow, not an afterthought.

Key takeaways

A well-executed financial reporting process workflow depends on sequential discipline, the right tools, and audience-appropriate outputs at every stage.

| Point | Details |

|---|---|

| Follow the sequence strictly | Each phase must be complete before the next begins; skipping steps causes compounding errors. |

| Automate high-volume tasks | Use ERP feeds and automated reconciliation tools to reduce manual effort and close faster. |

| Assign independent review | A reviewer who did not prepare the report catches narrative errors that preparers overlook. |

| Archive and lock immediately | Locking periods after close preserves audit trails and prevents retrospective changes. |

| Tailor reports to each audience | Boards need KPI summaries; auditors need full disclosure; lenders need cash flow detail. |

Why workflow discipline matters more than most finance teams admit

Working with business owners and finance managers across different sectors, I have noticed a consistent pattern. Teams that struggle with their close cycle almost never have a technology problem. They have a process problem. The ERP is fine. The data is available. But nobody documented who does what, in what order, and by when.

The transition from manual reporting to intelligence-driven reporting is real, and it is accelerating. AI tools now draft variance commentary in seconds. Automated reconciliation tools match thousands of transactions overnight. But none of that technology delivers value if the underlying workflow is undisciplined. Automation applied to a broken process produces wrong answers faster.

The teams I have seen succeed treat their bookkeeping foundations and their reporting workflow as one connected system. Clean daily bookkeeping makes month-end close shorter. A shorter close means reports reach stakeholders sooner. Sooner reports mean better decisions. That chain of cause and effect is why workflow discipline is not a finance department concern. It is a business performance concern.

My advice to any finance manager reading this: document your current process before you change it. You cannot improve what you have not mapped. Start with a simple close calendar, assign owners to each phase, and measure how long each phase actually takes. The gaps between your plan and your reality will tell you exactly where to focus.

— Busayo

How Finovate supports your financial reporting workflow

Finovate provides bookkeeping, payroll processing, VAT management, and business advisory services designed to support accurate, timely financial reporting for businesses in Finland. Our team handles the foundational data work that feeds your reporting cycle, so your close process starts with clean, reconciled records rather than a backlog of corrections. We also support digital accounting workflows that reduce manual effort and improve close times. Whether you need ongoing bookkeeping support or expert guidance on structuring your reporting process, Finovate's accounting and tax services are built to help your business report with confidence and meet every compliance deadline.

FAQ

What is the financial reporting process workflow?

The financial reporting process workflow is the structured sequence of steps that converts raw transaction data into compliant financial reports. It covers data collection, journal posting, reconciliation, consolidation, review, and distribution.

How many steps are in a typical financial reporting workflow?

A typical workflow contains 5–8 phases, from data collection through to archiving. The core close phases usually run across days 1–3 of a month-end cycle, with reporting and distribution on days 4–5.

What causes delays in the financial reporting workflow?

Delays most commonly stem from manual handoffs and poor communication between departments, not technical failures. Setting clear cut-off deadlines and automating data feeds removes the most frequent bottlenecks.

Why is independent review important in financial reporting?

An independent reviewer focuses on the narrative coherence and reasonableness of the report rather than recalculating figures. This catches errors and inconsistencies that the preparer misses through familiarity with the data.

How do SOPs improve the financial reporting process?

Standard operating procedures reduce manual extraction time and errors by replacing individual memory with documented, repeatable steps. They also make training new staff faster and ensure consistency across every close cycle.