TL;DR:

- Account reconciliation compares internal financial records with external statements to verify accuracy and identify discrepancies.

- Most businesses should reconcile accounts monthly to ensure reliable reports, detect errors early, and prevent fraud.

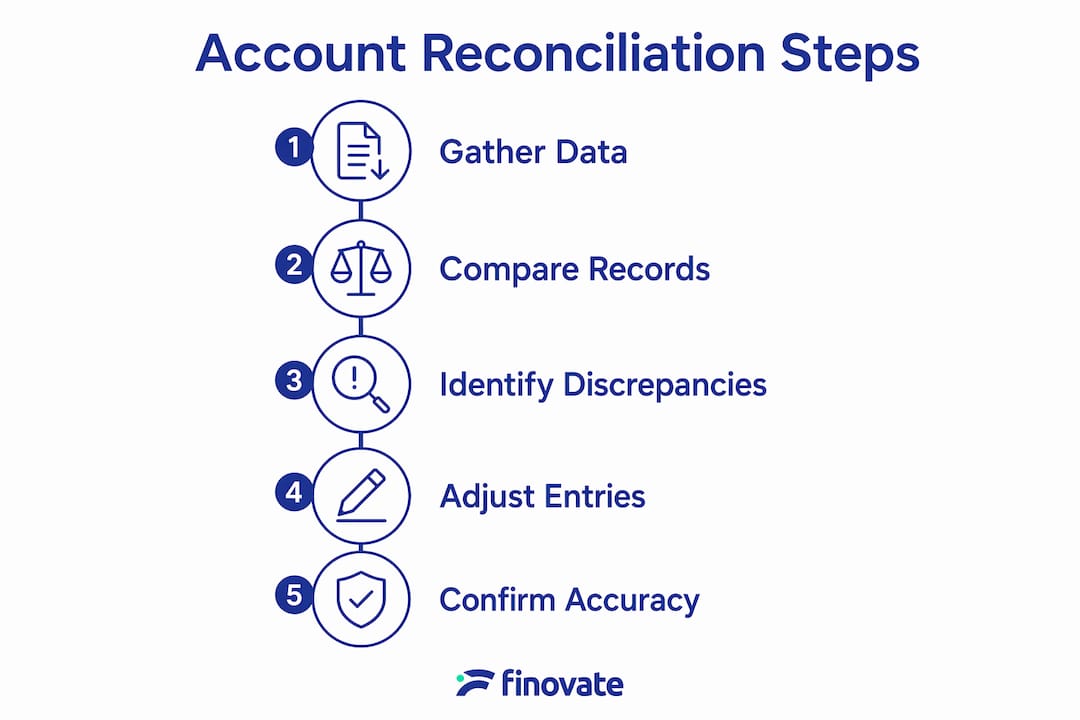

Account reconciliation is the process of comparing your internal financial records with external statements, such as bank statements, to confirm their accuracy and identify discrepancies. Every Finnish business owner and financial manager needs to reconcile accounts regularly. Without it, your profit and loss statements become unreliable, your tax filings carry risk, and your ability to make sound financial decisions is compromised. Unreconciled accounts make financial reports untrustworthy and risk regulatory non-compliance. The good news is that a consistent reconciliation process prevents most of these problems before they escalate.

Why reconcile accounts: the core reasons

Account reconciliation is defined as the systematic comparison of your bookkeeping records against external financial statements to verify that every transaction matches. The industry term is "account reconciliation," and it covers bank accounts, credit card accounts, supplier ledgers, and any other financial account your business holds. GAAP mandates reconciliation) to assure consistency and accuracy across financial statements. That mandate exists because reconciliation is the primary mechanism that keeps financial data trustworthy for stakeholders, tax authorities, and auditors alike.

The significance of account reconciliation goes beyond ticking a compliance box. When your records match your bank statements, you can trust your cash flow figures, your profit margins, and your tax position. When they do not match, you have a problem that will only grow more costly the longer it goes unaddressed. Reconciliation is the control that catches errors, flags fraud, and keeps your financial reporting on solid ground.

What are the key benefits of reconciling accounts?

Regular reconciliation delivers concrete advantages across financial control, compliance, and decision-making. The benefits are not theoretical. They show up directly in the quality of your financial reports and the health of your business.

- Financial accuracy. Reconciliation confirms that your profit and loss statements reflect real transactions. Accurate reconciliations give you confidence in your reports, tax filings, and business planning.

- Error detection. Data entry mistakes, duplicate transactions, and missed receipts are common in any business. Reconciliation catches these before they compound into larger problems. Correcting errors in the first month is quick; leaving them unresolved for months creates a major project.

- Fraud prevention. Reconciliation uncovers unauthorised transactions, ghost vendors, and duplicate payments. Neglecting cash shortfalls can even result in account closure by banks, making early detection critical.

- Audit readiness. Auditors review the final bank reconciliation as a standard testing procedure. Failing to reconcile makes audits longer and more expensive.

- Cash flow management. Reconciliation gives you an accurate picture of available funds. It also flags bank errors and timing issues before they affect your ability to pay suppliers or staff.

Pro Tip: Set a fixed date each month to complete your reconciliation. Treating it as a scheduled task, rather than something done when time allows, prevents backlogs from forming.

The importance of account reconciliation becomes clearest when something goes wrong. A single undetected duplicate payment or an unrecorded bank charge can distort your cash position for weeks. Catching it during reconciliation takes minutes. Catching it during an audit takes considerably longer.

How often should businesses reconcile accounts?

The frequency of reconciliation directly affects how quickly you detect problems and how much control you maintain over your finances.

| Frequency | Recommended for | Key benefit |

|---|---|---|

| Monthly | Most small and medium businesses | Meets GAAP standards; keeps year-end closing manageable |

| Weekly | Businesses with moderate transaction volumes | Reduces unresolved discrepancies; improves cash visibility |

| Daily | High transaction volume or fraud risk businesses | Enables prompt detection of suspicious activity |

Industry standards recommend monthly reconciliations for bank and credit card accounts as the baseline for full accuracy. Monthly reconciliation is the minimum that keeps your financial records credible and your year-end process manageable.

Businesses with high transaction volumes or minimal cash reserves need more frequent reviews. Daily reconciliation is critical for early fraud detection and cash control in these situations. A retail business processing hundreds of transactions per day, for example, cannot afford to wait until month-end to spot a discrepancy.

Reconciliation is the primary quality control in the monthly closing process. Businesses that reconcile monthly find that year-end closing becomes a routine review rather than a reconstruction exercise. Those that skip months face compounded errors and the risk of material misstatements.

Pro Tip: If you are unsure which frequency suits your business, start with monthly reconciliation and increase to weekly if you regularly find discrepancies or if your transaction volume grows.

What are common challenges in account reconciliation?

Reconciliation is straightforward in principle but presents real obstacles in practice. Understanding the most common challenges helps you address them before they cause serious problems.

-

Timing differences. Deposits in transit and outstanding cheques frequently cause mismatches between your records and your bank statement. Many businesses mistake timing differences for errors, but auditors always expect these to be clearly accounted for. The solution is to maintain a running list of outstanding items and clear them systematically each period.

-

Data entry errors. Transposed numbers, incorrect amounts, and miscategorised transactions are the most common source of discrepancies. These errors are easy to fix when caught immediately. Left unresolved, they distort every report that follows.

-

Misclassification. Posting a capital purchase as an operating expense, or vice versa, affects your profit figures and your tax position. A systematic review of account categories during reconciliation catches these before they reach your financial statements.

-

Lack of documentation. Reconciliation requires supporting documents: bank statements, invoices, receipts, and payment records. Businesses that do not maintain organised records spend far more time on reconciliation and are more likely to miss discrepancies.

"Reconcilers often mistakenly blame banks for mismatches rather than timing differences or internal errors. Thorough investigation of every discrepancy, rather than assuming bank error, is what produces a clean reconciliation."

Automation and bank synchronisation reduce manual work, improve accuracy, and enhance monitoring across multiple accounts. Modern accounting software connects directly to your bank feeds, which eliminates many manual entry errors and speeds up the matching process considerably. Businesses that rely on bank synchronisation gain real-time visibility into their account positions and spend less time on manual data entry.

What are best practices for effective account reconciliation in Finland?

A consistent process is the foundation of effective reconciliation. The following practices apply directly to Finnish businesses managing their own accounts or working with an accounting firm.

- Reconcile every account, every period. Bank accounts, credit card accounts, and supplier ledgers all require reconciliation. Focusing only on the main bank account leaves gaps that can hide errors or fraud.

- Integrate reconciliation into your monthly close. Treat reconciliation as a fixed step in your closing checklist, not an optional task. This keeps your records current and your reports reliable throughout the year.

- Maintain clear documentation. Keep bank statements, invoices, and supporting records organised and accessible. Auditors expect to see documentation that explains every reconciling item, and good records make that straightforward.

- Use accounting software with bank feeds. Automation improves reconciliation efficiency and reduces errors considerably. Software that pulls transactions directly from your bank eliminates a significant source of manual error.

- Review and sign off on completed reconciliations. A second review by a manager or accountant adds a control layer that catches errors the preparer may have missed.

Pro Tip: For Finnish businesses preparing for tax filings, reconciled accounts are the starting point for accurate VAT reporting and income tax calculations. Reconciling monthly means your tax return preparation requires far less effort and carries far less risk.

Skipping reconciliation results in compounded errors that require extensive cleanup and risk material misstatements. The businesses that find year-end accounting straightforward are almost always the ones that reconcile consistently throughout the year. Those that do not face reconstruction work that is time-consuming, costly, and stressful.

For businesses exploring how to structure their reconciliation process, Finovate's guidance on bank reconciliations for Finnish SMEs provides practical steps tailored to the Finnish business environment. Professional bookkeeping support, including services from AI-assisted bookkeeping platforms, can also help businesses maintain consistent reconciliation schedules without adding significant internal workload.

Key takeaways

Account reconciliation is the single most effective control for maintaining accurate financial records, detecting errors early, and keeping your business audit-ready throughout the year.

| Point | Details |

|---|---|

| Define reconciliation clearly | Reconciliation compares internal records with external statements to confirm accuracy and find discrepancies. |

| Reconcile at least monthly | Monthly reconciliation meets GAAP standards and keeps year-end closing manageable for most businesses. |

| Catch errors early | Fixing a data entry error in the same month takes minutes; leaving it unresolved for months creates a major project. |

| Fraud and audit protection | Regular reconciliation uncovers unauthorised transactions and ensures auditors find clean, documented records. |

| Use technology | Bank synchronisation and accounting software reduce manual errors and provide real-time account visibility. |

Reconciliation as a financial discipline, not just a task

Working with Finnish business owners over the years, I have seen the same pattern repeat itself. Businesses that treat reconciliation as a monthly discipline rarely face serious financial surprises. Those that treat it as something to do when time allows tend to discover problems at the worst possible moment, usually just before a tax deadline or an audit.

The most common mistake I see is not fraud or complex accounting errors. It is simply letting months pass without reconciling, then facing a backlog that distorts the picture of the business's financial health. By the time the cleanup is done, decisions have already been made on unreliable data.

Reconciliation is not glamorous work. But it is foundational. A business whose accounts are reconciled monthly has financial reports it can trust, tax filings it can defend, and a clear view of its cash position at all times. That clarity is worth considerably more than the time it takes to maintain it. My strong recommendation is to build reconciliation into your monthly close as a non-negotiable step, not an afterthought.

— Busayo

How Finovate supports accurate account reconciliation

Finovate works with Finnish businesses to keep their financial records accurate, compliant, and audit-ready throughout the year.

Our accounting services include bank reconciliation support, bookkeeping, VAT reporting, and payroll processing. Whether you run a limited company or operate as a light entrepreneur, we handle the reconciliation process so your financial reports reflect reality at all times. Businesses that work with us avoid the year-end cleanup that comes from months of unreconciled accounts. Our accounting package for limited companies and our service for light entrepreneurs are both structured to include regular reconciliation as a standard part of the service. Contact Finovate to discuss how we can support your financial management needs.

FAQ

What is account reconciliation?

Account reconciliation is the process of comparing your internal financial records with external statements, such as bank statements, to verify that every transaction is recorded accurately and to identify any discrepancies.

Why reconcile bank statements every month?

Monthly bank reconciliation meets GAAP standards and ensures your financial reports are accurate. It also catches errors and unauthorised transactions before they compound into larger problems.

What happens if you do not reconcile accounts?

Unreconciled accounts produce unreliable profit and loss statements, increase audit risk, and can result in regulatory non-compliance. Compounded errors from skipped reconciliations require extensive and costly cleanup.

How do timing differences affect reconciliation?

Timing differences, such as deposits in transit or outstanding cheques, cause temporary mismatches between your records and your bank statement. These are normal and expected, but they must be documented clearly to satisfy auditors.

Can accounting software replace manual reconciliation?

Accounting software with bank synchronisation automates transaction matching and reduces manual errors considerably. However, a human review of reconciled accounts remains necessary to catch misclassifications and approve the final result.