TL;DR:

- Finnish entrepreneurs do not have a single "entrepreneurship tax" but face a combination of income tax, VAT, and YEL pension contributions based on their business structure. Misunderstandings about these obligations—such as automatic pension coverage or VAT thresholds—can lead to costly errors, so understanding the actual components is essential for compliance and tax optimization. Proper planning involves choosing the right business structure, tracking deductible expenses, and setting YEL contributions accurately to secure future benefits and reduce tax liabilities.

Many Finnish entrepreneurs search for information about "entrepreneurship tax" only to discover that no single tax by that name exists. There is no single Finnish tax called 'entrepreneurship tax'; instead, you face a combination of income tax, value added tax (VAT), and statutory pension insurance payments depending on how you operate. Confusing these obligations is extremely common, and it can lead to missed registrations, unexpected bills, and compliance errors. This guide breaks down each obligation clearly, so you can plan with confidence and avoid costly surprises.

Table of Contents

- What does entrepreneurship tax mean in Finland?

- Types of taxes and payments entrepreneurs face

- Light entrepreneurship and invoicing services

- Deducting YEL contributions and optimising your earned income

- Practical tax strategies for Finnish entrepreneurs

- Why mastering Finnish entrepreneurship taxes means focusing on structure and small optimisations

- Expert support for Finnish entrepreneur taxes

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| No single entrepreneurship tax | Finnish entrepreneurs face several taxes and statutory payments, not one unified tax. |

| YEL is crucial | YEL pension insurance is mandatory and tax-deductible if conditions are met. |

| VAT triggers matter | Exceeding €20,000 annual trade income requires VAT registration for entrepreneurs. |

| Optimisation pays off | Smart handling of deductions, YEL income, and business form can reduce costs and boost benefits. |

| Light entrepreneur rules | Light entrepreneurs must manage invoicing, VAT, and YEL obligations carefully to remain compliant. |

What does entrepreneurship tax mean in Finland?

The term "entrepreneurship tax" is widely used in casual conversation and online searches, but it is not an official category in Finnish tax law. When people use the phrase, they usually mean one or more of the following: income tax on business profits, VAT collected from customers, or YEL (Yrittäjän eläkevakuutus) pension insurance contributions. Each of these operates under different rules, different thresholds, and different administrative processes.

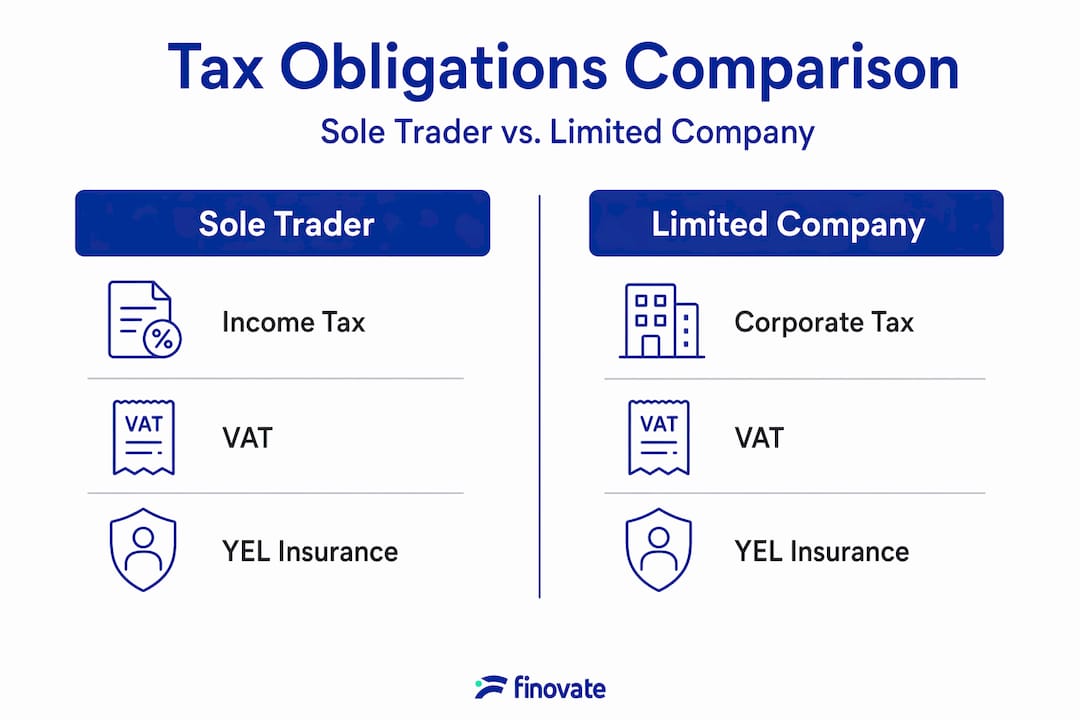

Finnish entrepreneurs face multiple taxes and statutory payments depending on business structure and activity. A sole trader (toiminimi) pays income tax on net business income, which is split between earned income and capital income. A limited liability company (osakeyhtiö, or Oy) pays corporate income tax at a flat rate of 20% on its profits, separately from any salary the owner draws personally.

"Entrepreneurship tax" is a shorthand term, not a legal one. Understanding the real components behind the phrase is the first step to getting your obligations right.

This distinction matters because the compliance steps for each obligation differ significantly. Missing the VAT registration threshold, for example, can result in back payments and penalties. Misunderstanding YEL can leave you underinsured and facing a gap in your social security entitlements later in life. For practical entrepreneur tax tips that address these specifics, it is worth building a solid foundation of knowledge first.

Common misunderstandings in this area include:

- Assuming that paying income tax also covers pension contributions automatically

- Believing that a micro business below the VAT threshold never needs to register at all

- Thinking that YEL is optional or insignificant for smaller operations

- Conflating corporate income tax with personal income tax when operating through an Oy

Each misunderstanding carries real financial risk, which is why clarity on this topic is essential for every entrepreneur operating in Finland.

Types of taxes and payments entrepreneurs face

Having established what areas "entrepreneurship tax" covers, let's see how obligations vary based on business type and activity. The three main categories are income tax, VAT, and YEL pension insurance.

Income tax works differently depending on your chosen business structure. Sole traders report their business income directly on their personal tax return. The income is then divided into earned income (taxed progressively up to around 51.5% at higher brackets in 2026, including municipal tax) and capital income (taxed at 30% up to €30,000 and 34% above that). For an Oy, corporate tax is profit-based and calculated after deductible expenses, with losses carried forward to future years.

VAT must be charged on most goods and services sold in Finland. If your annual turnover exceeds €20,000, VAT registration is mandatory. The standard rate is 25.5%, with reduced rates applying to specific categories such as food, books, and accommodation.

YEL pension insurance is a statutory cost that many entrepreneurs overlook or underestimate. YEL is mandatory for self-employed individuals who meet conditions such as working regularly in their own business, being between 18 and 68 years old, and earning above the minimum YEL income threshold. The contributions are calculated as a percentage of your confirmed YEL earned income (työtulo), which you set yourself within certain bounds.

Here is a comparison of key obligations by business structure:

| Obligation | Sole trader (toiminimi) | Limited company (Oy) |

|---|---|---|

| Income tax | Progressive personal income tax | 20% corporate income tax |

| VAT | Required above €20,000 turnover | Required above €20,000 turnover |

| YEL | Required if conditions met | Required for owner-operators if conditions met |

| Salary taxation | N/A (draws from business income) | PAYE on salary drawn from company |

| Dividend taxation | N/A | 25.5% or 85% taxable at personal rate |

Deductible expenses are a critical tool for reducing your taxable profit. These include office costs, professional services, equipment, travel for business purposes, and marketing expenses. Our small business tax guide covers the full list in detail. Understanding YEL insurance importance is equally critical, as it affects not just current costs but also your future pension, parental leave, and sickness benefit entitlements.

Pro Tip: Review your YEL earned income level at least once a year. Setting it too low saves money short term but reduces your future social security benefits significantly.

Light entrepreneurship and invoicing services

Income, VAT, and YEL apply differently for light entrepreneurs, which is a popular approach for side hustles and freelancing in Finland. A light entrepreneur (kevytyrittäjä) does not establish their own company. Instead, they use an invoicing service platform to bill clients, and the platform handles employer contributions and tax withholdings on their behalf.

Operating as a light entrepreneur affects how tax prepayments are handled, and VAT liability may arise once income crosses the relevant threshold. This is a detail that catches many people off guard. Because the invoicing service is technically the employer for payroll purposes, the light entrepreneur receives a net salary. However, VAT registration responsibility and income tracking still fall to the individual in certain situations.

Here are the key steps light entrepreneurs should follow to stay compliant:

- Track your annual trade income carefully. If your gross invoiced income through the platform exceeds €20,000 in a calendar year, you must register for VAT independently or ensure your invoicing service handles it on your behalf.

- Assess your YEL obligation annually. If your entrepreneurial activity is regular and your confirmed earned income from self-employment crosses the minimum threshold, YEL registration is required even for light entrepreneurs.

- Keep records of all income sources. If you have multiple clients through the same or different platforms, combine the figures. The VAT threshold applies to total business income, not per-client income.

- Understand what the platform covers and what it does not. Most invoicing services handle income tax prepayments and social insurance contributions for the work processed through them. They do not automatically manage your YEL registration.

Pro Tip: Before choosing an invoicing service, ask explicitly which taxes and contributions they handle and which ones remain your responsibility. Not all platforms offer the same level of coverage. For those considering a more formal setup, reading about private trader registration can help you decide whether a sole trader structure might be more efficient for your situation.

Light entrepreneurship suits those who invoice irregularly or want to test a business idea without committing to a formal legal structure. However, as your income grows, transitioning to a sole trader or Oy structure often becomes more tax-efficient and administratively cleaner.

Deducting YEL contributions and optimising your earned income

Optimising tax deductions and social security entitlements starts with YEL. Many entrepreneurs pay their YEL contributions throughout the year but forget to claim the deduction on their tax return. This is money left on the table unnecessarily.

YEL contributions are fully tax-deductible, and you can claim the deduction in personal taxation or company taxation depending on your business structure. For a sole trader, the deduction is made on the personal tax return. For an Oy owner who pays their own YEL, the deduction is typically claimed personally, not through the company.

Your YEL earned income, the työtulo figure, is the foundation of the entire system. It determines how much you pay in contributions and what level of social security benefits you are entitled to receive. Setting it accurately is therefore a financial decision with consequences that extend years into the future.

| YEL earned income (€/year) | Approx. contribution (2026, ~24.1% for under 53 years) | Effect on pension accrual |

|---|---|---|

| €15,000 | ~€3,615 | Minimum basic accrual |

| €30,000 | ~€7,230 | Moderate accrual |

| €50,000 | ~€12,050 | Strong accrual and better sickness benefit base |

| €80,000 | ~€19,280 | High accrual, maximum benefit base |

The figures above are approximate and serve as a planning reference. Actual rates vary based on age and the year you started your YEL insurance. You should also review YEL insurance tax deduction options regularly to ensure you are claiming correctly. Practical finance tips for entrepreneurs can further support sound financial planning around these contributions.

Pro Tip: If you cannot afford high YEL contributions right now, it is still better to register at the minimum threshold and increase the level later than to delay registration entirely. Late registration can trigger back payments and interest.

Practical tax strategies for Finnish entrepreneurs

All these obligations can be managed and optimised. Here are practical strategies every Finnish entrepreneur should know in 2026.

Choose the right business structure from the start. The tax implications of operating as a sole trader versus an Oy are substantial. At lower income levels, a sole trader structure is simpler and avoids double taxation. At higher income levels, salary and dividend planning through an Oy often leads to a more favourable overall tax burden. This is one of the most impactful decisions you will make.

Track deductible expenses meticulously. Every legitimate business expense that reduces your taxable profit is worth claiming. Common deductions include:

- Home office expenses (if your home is your primary place of work)

- Business travel, mileage, and accommodation

- Professional subscriptions, software, and tools

- Marketing costs and website fees

- Accounting and legal advisory costs

Our guide to deductible expense strategies provides a structured approach to capturing all eligible costs.

Monitor VAT and YEL triggers throughout the year. Do not wait until year-end to check whether you have crossed the €20,000 VAT threshold. Set a simple monthly income tracker and review it regularly. Similarly, if your self-employment activity grows, assess your YEL obligation promptly.

Foreign entrepreneurs operating in Finland must understand local tax residency rules. Tax residence and liability depend on place of effective management and permanent establishment. A company managed from Finland is generally taxable in Finland, even if incorporated elsewhere. This is a critical consideration for international founders setting up Finnish operations.

Avoid the most common compliance mistakes:

- Failing to register for YEL when conditions are met

- Missing the VAT registration threshold and receiving a retroactive bill

- Not entering YEL contributions on the tax return as a deduction

- Misclassifying personal expenses as business expenses

For additional support on meeting your obligations efficiently, our tax preparation guide and guidance on capital income tax optimisation are valuable resources.

Pro Tip: Schedule a quarterly tax review in your calendar. A 30-minute check on VAT, YEL status, and deductible expenses can prevent significant year-end surprises.

Why mastering Finnish entrepreneurship taxes means focusing on structure and small optimisations

From our experience working with Finnish entrepreneurs across many different industries and business stages, the biggest cost differences almost never come from the tax rates themselves. They come from the structure you choose and the small, consistent decisions you make throughout the year.

Many new entrepreneurs focus intensely on finding the lowest tax rate or the best deduction category. That attention is understandable. But the compounding effect of choosing the wrong business form, setting YEL income too low for too long, or missing a VAT registration can far outweigh any rate optimisation.

We have seen sole traders who should have transitioned to an Oy structure two years earlier, paying tens of thousands of euros more in income tax than necessary. We have also seen Oy owners drawing all their compensation as salary when a mixed salary and dividend model would have been considerably more efficient. These are not exotic tax planning strategies. They are practical, well-established approaches that require only accurate information and timely decisions.

The YEL earned income question is particularly underappreciated. Setting it correctly is not just about current cash flow. It shapes your future pension, your entitlement to sickness benefit, and your parental leave payments. An entrepreneur who sets their työtulo thoughtfully today is investing in their future financial security.

Our view is this: compliance and optimisation are not separate activities. When you track your obligations carefully, claim every deduction you are entitled to, and review your business structure as your income grows, you are simultaneously staying compliant and reducing your tax burden. The two go together. Reviewing essential tax tips regularly is a habit that pays genuine dividends.

Expert support for Finnish entrepreneur taxes

Navigating VAT registration, YEL obligations, income tax planning, and deduction tracking is manageable, but it takes time and ongoing attention. For many entrepreneurs, the most effective use of their resources is to focus on running their business while working with an expert who handles the financial compliance side.

We at Finovate specialise in supporting Finnish entrepreneurs and small business owners with exactly these obligations. Whether you need help with accounting for light entrepreneurs, VAT registration, YEL coordination, or broader business tax planning, we provide tailored services that fit your specific situation. Our accounting and tax services are designed to give you clarity, reduce administrative burden, and help you make financially sound decisions at every stage of your business. Contact us to discuss how we can support your compliance and financial goals.

Frequently asked questions

Is YEL insurance mandatory for all Finnish entrepreneurs?

YEL insurance is mandatory for self-employed individuals who work regularly in their own business, are aged 18 to 68, and earn above the minimum income threshold. It does not apply automatically to every person who invoices occasionally.

How can I claim YEL contributions as a tax deduction?

YEL contributions are tax-deductible and must be entered manually on your tax return, either in personal taxation or company taxation depending on your business structure. The deduction is not applied automatically.

When do I need to register for VAT as a light entrepreneur?

You must apply for VAT registration when your trade income exceeds €20,000 in a calendar year, regardless of whether you operate through an invoicing service platform.

Can losses be carried forward in Finnish company taxation?

Yes. If deductible expenses exceed taxable income, losses can be carried forward to subsequent tax years under Finnish company taxation rules, reducing future tax liability.

Does tax liability change for foreign business owners in Finland?

Yes. Tax liability depends on effective management location and permanent establishment. If your business is managed from Finland, it is generally subject to Finnish taxation regardless of where it was incorporated.