TL;DR:

- Self-employed individuals pay a federal tax rate of 15.3% on 92.35% of their net earnings, covering Social Security and Medicare. Finnish freelancers managing international clients must understand both US and Finnish tax obligations, including record-keeping and possible deductions. Proper planning and disciplined savings help freelancers meet their tax obligations and avoid surprises during filing seasons.

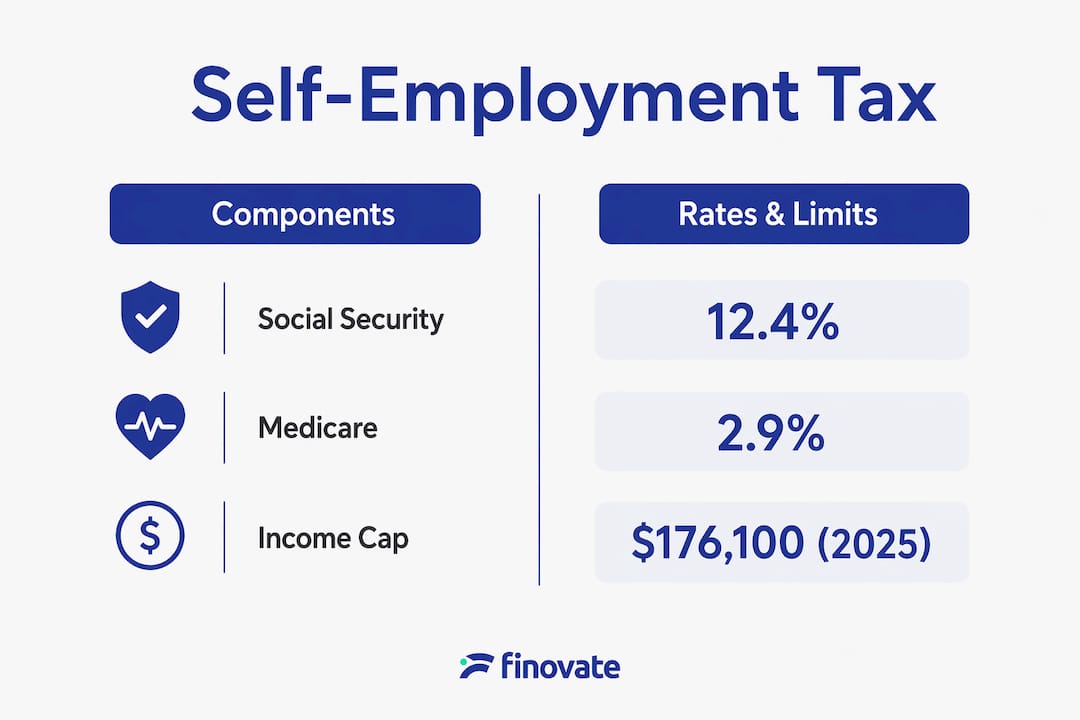

Self-employed tax is defined as a federal levy requiring individuals who work for themselves to pay both the employer and employee portions of Social Security and Medicare contributions on their net earnings. In Finland, freelancers and sole traders encounter this concept most often when researching their obligations under international tax frameworks or when working with clients abroad. The self-employment tax rate stands at 15.3%, split into 12.4% for Social Security and 2.9% for Medicare. Understanding what self-employed tax means, how it differs from income tax, and how it applies to your situation as a Finnish freelancer gives you a firm foundation for managing your finances responsibly.

What is self-employed tax and how is it calculated?

Self-employment tax is a mandatory federal tax that applies when your net earnings from self-employment reach £400 or more in a given year. The £400 threshold is the point at which the obligation begins. Below that level, no self-employment tax is due.

The calculation does not apply to your full gross income. Instead, it applies to 92.35% of your net earnings. Net earnings are what remain after you subtract allowable business expenses from your total income. This distinction matters because it means your tax base is lower than your gross revenue.

The 15.3% rate breaks down as follows:

- 12.4% covers Social Security contributions

- 2.9% covers Medicare contributions

- An additional 0.9% Medicare tax applies once earned income exceeds $200,000 for single filers or $250,000 for joint filers

For 2025, Social Security tax applies to income up to $176,100. Medicare tax has no income cap and applies to all net earnings without limit.

The standard tool for reporting self-employment tax in the US system is IRS Schedule SE. This form requires your Social Security number or Individual Taxpayer Identification Number, along with accurate records of your net earnings. Finnish freelancers working within the US tax framework, or advising clients who do, will encounter this form regularly.

| Component | Rate | Income cap |

|---|---|---|

| Social Security | 12.4% | $176,100 (2025) |

| Medicare | 2.9% | No cap |

| Additional Medicare | 0.9% | Above $200K / $250K |

| Total standard rate | 15.3% | Varies |

Pro Tip: Set aside at least 25–30% of every invoice payment into a separate account. This covers both self-employment tax and income tax, so you are never caught short at filing time.

What is the difference between self-employed tax and income tax?

Self-employment tax and income tax are two separate federal obligations. Confusing them is one of the most common mistakes new freelancers make. Self-employment tax funds Social Security and Medicare specifically. Income tax funds general government revenue across a much broader range of public services.

They are calculated on different bases and reported separately. Self-employment tax uses net earnings via Schedule SE. Income tax uses adjusted gross income, which is a broader figure that includes all sources of income minus certain deductions.

Self-employed individuals can deduct 50% of the self-employment tax they pay when calculating their adjusted gross income for income tax purposes. This deduction does not reduce the self-employment tax itself. It simply mirrors the tax relief that employed workers receive, because employers deduct their share of payroll taxes as a business expense.

The 50% deduction is designed to create parity between employed and self-employed workers. An employee never sees the employer's 7.65% payroll contribution. A self-employed person pays the full 15.3% visibly and directly, so the deduction compensates for that asymmetry.

Key distinctions to keep in mind:

- Self-employment tax is paid in addition to income tax, not instead of it

- The two taxes use different forms and different calculation methods

- The additional 0.9% Medicare surcharge applies above defined income thresholds and is separate from the standard 15.3%

- Deducting half of self-employment tax reduces your income tax bill, but your self-employment tax liability stays fixed

For Finnish freelancers, understanding this separation is particularly useful when comparing obligations under the Finnish tax system with those that apply when earning income from US-based clients or platforms.

Are there special considerations or exceptions for self-employed tax?

Several rules modify the standard self-employment tax picture. Knowing them helps you plan accurately and avoid unexpected bills.

- The £400 threshold. Self-employment tax is only due when net earnings reach £400 or more in a tax year. Earnings below this level are exempt. This threshold applies per individual, not per client or project.

- The additional Medicare surcharge. An extra 0.9% Medicare tax applies once your earned income exceeds $200,000 as a single filer or $250,000 as a married couple filing jointly. This surcharge is on top of the standard 2.9% Medicare rate.

- Quarterly estimated payments. Self-employed individuals do not have tax withheld at source. You are responsible for making estimated tax payments four times a year. Missing these payments can result in penalties, even if you pay the full amount at year end.

- S-Corporation election. High-earning service providers sometimes elect S-Corporation status to manage their payroll tax liability. Under this structure, only the salary portion of income is subject to self-employment tax, not distributions. This approach requires careful legal and accounting advice before implementation.

- Church employee exemptions. Specific rules apply to church employees and members of certain religious orders. These are narrow exceptions and do not affect the majority of freelancers.

Pro Tip: Review your estimated tax deadlines at the start of each quarter. Missing a payment date costs more than the inconvenience of scheduling it in advance.

How do Finnish freelancers handle filing and record-keeping?

Accurate record-keeping is the foundation of correct self-employment tax filing. Revenue Ruling 56-407 from the IRS makes clear that self-employed individuals must report all income and claim all allowable expenses. Selective reporting is not permitted. You cannot choose only the deductions that benefit you while ignoring others.

For Finnish freelancers, the practical record-keeping requirements look like this:

- Income records. Keep invoices, bank statements, and payment confirmations for every client payment received during the tax year.

- Expense records. Document every business expense with receipts or digital records. Allowable expenses reduce your net earnings and therefore reduce your tax base.

- Mileage and travel logs. If you travel for business, maintain a log with dates, destinations, and purposes. These deductions are commonly missed.

- Equipment and software costs. Computers, subscriptions, and professional tools used for work are deductible. Keep purchase receipts and note the business purpose.

- Professional fees. Accounting fees, legal advice, and professional memberships are allowable expenses in most jurisdictions.

Finland's own tax authority, the Finnish Tax Administration (Vero), operates separately from the IRS framework. Finnish freelancers pay income tax and self-employed pension contributions (YEL) under Finnish law. The YEL contribution functions similarly to the Social Security portion of US self-employment tax: it funds your pension and social security coverage. Understanding how freelancers handle accounting in Finland helps you see where these two systems overlap and where they diverge.

Penalties for underreporting income or failing to pay are real in both systems. In Finland, late payment interest and tax surcharges apply when returns are filed incorrectly or after the deadline. The best defence is accurate, timely bookkeeping throughout the year, not a rushed effort before the filing deadline.

| Record type | Why it matters | Retention period |

|---|---|---|

| Sales invoices | Proves income reported | At least 6 years |

| Expense receipts | Supports deduction claims | At least 6 years |

| Bank statements | Reconciles income and payments | At least 6 years |

| Contracts | Confirms business relationship | Duration plus 6 years |

For Finnish freelancers looking to reduce their tax burden legally, understanding deductible expenses in Finland is one of the most direct ways to lower your net taxable income.

Key takeaways

Self-employment tax is a mandatory levy on net earnings that self-employed individuals pay in full, covering both employer and employee portions of Social Security and Medicare at a combined rate of 15.3%.

| Point | Details |

|---|---|

| Self-employment tax definition | A federal tax on net earnings funding Social Security and Medicare, paid entirely by the self-employed individual. |

| Standard rate | 15.3% applies to 92.35% of net earnings; Social Security is capped, Medicare is not. |

| Separate from income tax | Both taxes are due independently; deducting 50% of self-employment tax reduces income tax, not the levy itself. |

| Filing threshold | Net earnings of £400 or more trigger the obligation; below this, no self-employment tax is due. |

| Record-keeping duty | All income and allowable expenses must be reported accurately; selective reporting is not permitted under IRS rules. |

The mindset shift that catches most freelancers off guard

When I speak with new freelancers, the same issue comes up repeatedly. They see their first large invoice payment land in their account and feel financially comfortable. What they have not accounted for is that the full 15.3% self-employment tax is sitting inside that figure, waiting to be paid. Employed workers never see the employer's share of payroll tax because it never appears in their pay slip. Self-employed individuals pay both sides directly, and that visibility can be a shock.

The freelancers I have seen manage this well share one habit: they treat tax as a cost of sale, not an afterthought. The moment an invoice is paid, a fixed percentage moves to a dedicated tax account. It never feels like money they have. That discipline removes the anxiety that builds up when a quarterly payment is due and the funds are not there.

The other mistake I see consistently is assuming that self-employment tax and income tax cancel each other out or overlap. They do not. You owe both, calculated separately, and the combined liability is higher than most people expect in their first year of freelancing. Getting professional advice early, before the first filing deadline, saves far more than the cost of the advice itself.

For Finnish freelancers specifically, the YEL pension contribution adds another layer to the picture. It is not optional above the income threshold, and it affects your social security coverage directly. Planning for all three obligations together, income tax, YEL, and any applicable self-employment tax on foreign earnings, gives you a complete and accurate picture of your real take-home income.

— Busayo

Tax and accounting support for Finnish freelancers

Managing self-employment tax, income tax, and Finnish pension contributions simultaneously is a significant administrative responsibility.

Finovate provides expert accounting and tax services tailored specifically for Finnish freelancers and self-employed individuals. From bookkeeping and VAT reporting to quarterly payment planning and annual filings, Finovate handles the detail so you can focus on your work. The team understands both Finnish tax regulations and the international frameworks that affect freelancers earning from clients abroad. If you want clear, accurate support without the guesswork, Finovate is ready to help.

FAQ

What is the self-employment tax rate?

The standard self-employment tax rate is 15.3%, comprising 12.4% for Social Security and 2.9% for Medicare, applied to 92.35% of net earnings.

Is self-employment tax mandatory?

Self-employment tax is mandatory once your net earnings reach £400 or more in a tax year. Below that threshold, no self-employment tax is owed.

Can I deduct self-employment tax from my income tax?

You can deduct 50% of the self-employment tax you pay when calculating your adjusted gross income for income tax purposes. This reduces your income tax bill but does not reduce the self-employment tax itself.

How do Finnish freelancers file self-employment tax?

Finnish freelancers report income and expenses through the Finnish Tax Administration (Vero). Those with US-sourced income may also need to file using IRS Schedule SE alongside their Finnish returns.

What records do I need to keep as a self-employed person?

You must keep invoices, expense receipts, bank statements, and contracts for at least six years. Accurate records support your deduction claims and protect you in the event of a tax audit.