TL;DR:

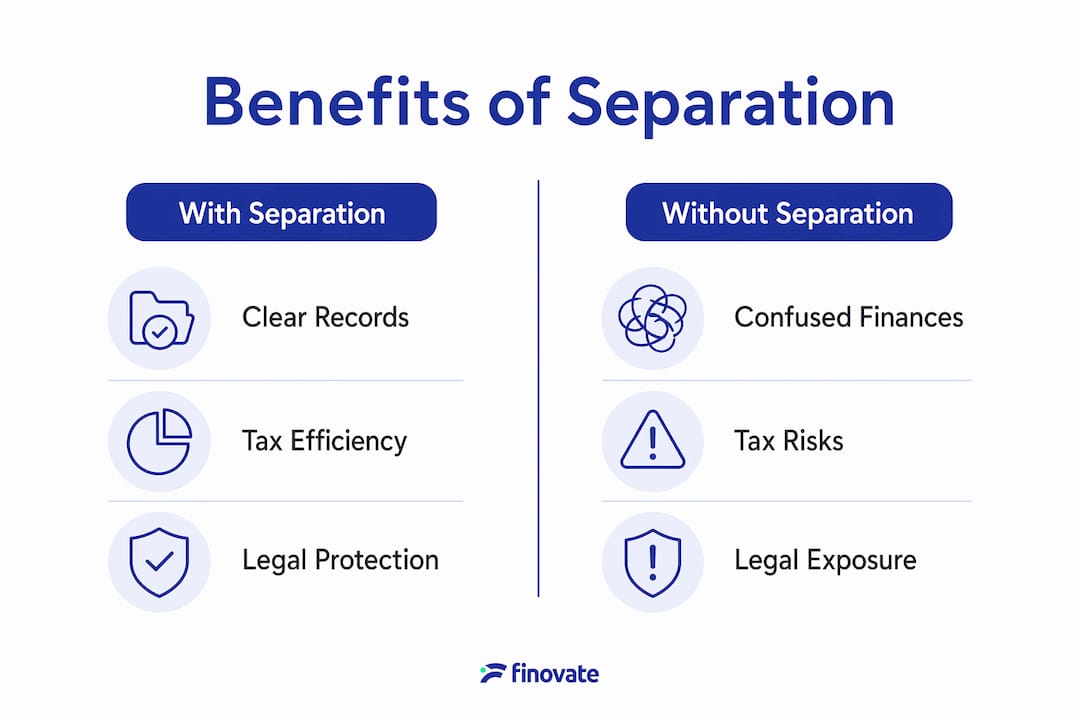

- Separating business finances from personal money protects assets, simplifies taxes, and improves financial clarity. It ensures legal protection, enhances credibility, and streamlines cash flow management for small businesses. Consistent discipline and early setup are essential to maintaining clear financial boundaries.

Separating business finances is defined as the practice of keeping all business income, expenses, and accounts entirely distinct from your personal money. This single discipline protects your personal assets, simplifies tax filing, and gives you an accurate picture of your business's true financial health. Cash flow problems cause 82% of small business failures, which makes financial clarity not a nice-to-have but a survival requirement. Understanding why separate business finances matter is the first step towards building a business that lasts.

What are the main reasons to separate business finances?

Financial separation, the formal practice of maintaining distinct accounts for business and personal use, delivers benefits across legal, tax, and operational areas. Entrepreneurs who treat this as a priority from day one avoid the most common and costly mistakes in business finances.

The core reasons to separate your finances include:

- Legal protection. Mixing personal and business funds can expose your personal assets to business debts. For LLCs and corporations, courts can pierce the corporate veil when finances are commingled, removing the liability shield your business structure provides.

- Tax accuracy. Mixing personal and business accounts complicates the identification of deductible expenses. A dedicated business account means every transaction is clearly business-related, reducing errors and missed deductions.

- Cash flow visibility. Separate accounts let you see exactly how much money your business earns and spends. Without that clarity, you cannot make sound decisions about hiring, investment, or growth.

- Credibility with lenders and clients. Separate business accounts signal professionalism and financial stability. Banks, investors, and clients all respond more favourably to businesses with clear financial boundaries.

- Simpler bookkeeping. Every transaction sits in the right place from the start. Your accountant spends less time untangling records and more time advising you.

Each of these benefits compounds over time. The longer you maintain separation, the cleaner your financial history becomes, and the easier every future decision gets.

How does separating finances impact cash flow and financial management?

Cash flow is the single most critical measure of a business's day-to-day health. When personal and business money share the same account, you lose the ability to track either accurately.

Consider a common scenario: you pay a supplier from your personal account one week, then cover a personal bill from the business account the next. By the end of the month, you cannot tell whether your business is profitable or whether you are subsidising it from your own savings. This confusion is not just inconvenient. 82% of small business failures trace back to cash flow problems rather than product or market failures. That statistic means most businesses that close do so because their owners lost sight of the numbers, not because their idea was wrong.

A dedicated business account resolves this directly. Every pound that enters or leaves the business is recorded in one place, making cash flow management straightforward rather than a monthly reconstruction exercise.

| Scenario | With separation | Without separation |

|---|---|---|

| Monthly profit visibility | Clear and immediate | Requires manual reconciliation |

| Tax preparation time | Minimal | Lengthy and error-prone |

| Audit readiness | Records are clean | High risk of errors and penalties |

| Cash flow forecasting | Reliable | Unreliable due to mixed transactions |

| Bookkeeping cost | Lower | Higher due to extra accountant time |

Pro Tip: Schedule a 15-minute financial review every week. Check your business account balance, outstanding invoices, and upcoming expenses. This habit catches problems early and keeps your cash flow picture accurate at all times.

Using a dedicated business debit card reinforces this discipline further. A separate business debit card creates a clean paper trail for every purchase, which removes all guesswork during tax audits and year-end reviews.

What are the legal implications of not separating business and personal finances?

The legal consequences of commingling funds are serious and often irreversible. Business structures such as limited liability companies and corporations exist specifically to protect your personal assets from business liabilities. That protection disappears the moment you treat business and personal money as interchangeable.

The legal concept at the centre of this risk is "piercing the corporate veil." When a court pierces the veil, it disregards the legal separation between you and your business. Your personal savings, property, and other assets become fair game for business creditors. Courts apply this doctrine when they find that the business was not operated as a genuinely separate entity. Commingled finances are one of the most common triggers.

Business structure dictates the legal necessity of separation, with LLCs and corporations requiring clear financial boundaries to preserve personal asset protection. Sole traders face a different situation: they have no corporate veil to pierce, so their personal assets are always at risk. For sole traders, separation is still critical for tax accuracy and financial clarity, even if the legal stakes differ.

A practical example illustrates the risk clearly. Suppose your limited company faces a lawsuit from a supplier. If your company bank account regularly received personal deposits and paid personal bills, a court may rule that the company was never truly separate from you. The supplier could then pursue your personal bank account or home to satisfy the debt.

Pro Tip: Maintaining separate records goes beyond opening a business bank account. Keep separate receipts, invoices, and expense logs. Consistent record-keeping is what courts and tax authorities examine, not just which account you used.

What practical steps should entrepreneurs take to separate their finances?

Effective financial separation requires deliberate action, not good intentions. The steps below apply whether you are starting a new business or correcting years of mixed finances.

- Open a dedicated business bank account within your first week of trading. Business owners are recommended to separate finances within the first week of operation. Early separation prevents bad habits from forming and keeps your records clean from the start.

- Apply for a business debit or credit card. Use it exclusively for business purchases. Never use it for personal spending, even once. A single personal transaction on a business card creates a record you will need to explain later.

- Set up a formal owner draw or payroll process. Pay yourself a set amount on a regular schedule, transferred from the business account to your personal account. This keeps your personal income clearly recorded and prevents the habit of dipping into business funds informally.

- Record every transaction at the time it occurs. Do not rely on memory or end-of-month reconstruction. Use accounting software or work with a bookkeeper to log income and expenses as they happen.

- If you pay a business expense personally, record it immediately. Owner contributions and draws must be clearly documented to preserve separation. A payment from your personal account for a business cost is a contribution to the business, not a grey area.

- Review your business expense tracking process quarterly. Check that no personal expenses have crept into business records and vice versa.

These steps are not complicated. They require consistency rather than expertise. The entrepreneurs who manage their finances well are those who build these habits early and maintain them without exception.

How does financial separation support tax efficiency and credibility?

Clean financial separation makes tax preparation faster, more accurate, and less stressful. Tax authorities, including the Finnish Tax Administration, require businesses to substantiate every deduction they claim. A dedicated business account provides that substantiation automatically.

When all business transactions flow through a single account, your accountant can identify every deductible expense without cross-referencing personal statements. Missed deductions are one of the most common and costly mistakes in business finances. A sole trader who mixes accounts may overlook legitimate deductions for equipment, software, or professional services simply because those purchases are buried among personal transactions.

The audit risk reduction is equally significant. A business with clean, separate records presents a straightforward picture to tax authorities. A business with commingled accounts invites scrutiny because every transaction requires explanation.

| Area | With separated finances | With commingled finances |

|---|---|---|

| Deduction identification | Automatic and complete | Manual and prone to omissions |

| Audit trail quality | Clear and verifiable | Unclear and time-consuming |

| Tax preparation time | Short | Long and costly |

| Lender confidence | High | Low |

| Investor credibility | Strong | Weak |

Credibility with lenders deserves particular attention. When you apply for a business loan or seek investment, the first thing any lender examines is your business financial history. A business account with consistent, clearly recorded transactions demonstrates that you manage money responsibly. A mixed account raises immediate doubts. For financial management tips that go beyond separation, Finovate publishes practical guidance tailored to Finnish entrepreneurs.

Key takeaways

Separating business and personal finances protects your personal assets, reduces tax errors, and gives you the cash flow clarity needed to make sound business decisions.

| Point | Details |

|---|---|

| Cash flow clarity | Separate accounts let you see exactly what your business earns and spends each month. |

| Legal protection | Commingled funds risk piercing the corporate veil, exposing personal assets to business debts. |

| Tax efficiency | Dedicated accounts make every deductible expense easy to identify and substantiate. |

| Credibility with lenders | Clean business records signal professionalism and improve your chances of securing finance. |

| Act within week one | Opening a business account in your first week of trading prevents costly habits from forming. |

The discipline nobody tells you about

Most articles on this topic focus on the mechanics: open an account, get a card, hire a bookkeeper. That advice is correct, but it misses the harder part.

The real challenge is behavioural. Most small business owners avoid financial management because it feels complicated. So they delay, improvise, and tell themselves they will sort it out later. Later becomes never, and by the time they seek help, months of mixed transactions need untangling at considerable cost.

The pattern I see most often is what I call the personal ATM problem. An owner needs £200 for a personal bill, the business account has funds, and the transfer takes 30 seconds. Treating business funds as a personal ATM is the single fastest way to destroy your financial records and, in the case of a limited company, your liability protection. The fix is not willpower. It is structure. Pay yourself a regular draw, keep a small personal emergency fund separate from both accounts, and remove the temptation entirely.

The entrepreneurs I have seen manage this well share one trait: they treat their finances as a system, not a task. They do not sit down once a year and try to make sense of everything. They maintain the system weekly, and the annual accounts practically write themselves. If you are organising your business finances for the first time, start with the system, not the spreadsheet.

— Busayo

Finovate accounting services for Finnish entrepreneurs

Keeping business and personal finances separate is straightforward when you have the right support in place. Finovate provides bookkeeping, VAT reporting, payroll processing, and tax planning services designed specifically for small businesses and entrepreneurs in Finland.

For entrepreneurs who invoice clients regularly, Finovate's monthly invoicing service handles the administrative side so you can focus on the work. If you need broader accounting and tax support, Finovate's full accounting services cover everything from business registration to annual tax filing. Clean financial separation becomes significantly easier when a professional team manages the records on your behalf.

FAQ

Why should I separate business and personal finances?

Separation protects your personal assets from business liabilities, simplifies tax filing, and gives you an accurate view of your business's cash flow. Without it, both your legal protection and your financial clarity are at risk.

When should I open a business bank account?

Open a dedicated business bank account within your first week of trading. Early separation prevents mixed records from forming and keeps your bookkeeping clean from the start.

What is piercing the corporate veil?

Piercing the corporate veil is a legal ruling that removes the liability protection of an LLC or corporation. Courts apply it when business and personal finances are commingled, exposing the owner's personal assets to business debts.

How does financial separation help with taxes?

Separate accounts ensure every transaction is clearly business-related, making deductible expenses easy to identify and substantiate. This reduces tax errors, shortens preparation time, and lowers the risk of an audit.

Can sole traders benefit from separating their finances?

Yes. Sole traders do not have a corporate veil to protect, but separate accounts still simplify tax filing, improve cash flow visibility, and make bookkeeping significantly less time-consuming.