TL;DR:

- Payroll tax in Finland obligates employers to withhold employee contributions and remit the total to pension providers and tax authorities.

- Compliance requires timely calculation, withholding, remittance, and reporting of statutory contributions, including TyEL, unemployment, and accident insurances.

Payroll tax is the compulsory obligation employers carry to withhold statutory contributions from employee wages and remit the combined total to pension providers and tax authorities. In Finland, this obligation centres primarily on TyEL, the earnings-related pension contribution governed by the Employees Pensions Act, alongside other social security contributions. Understanding how payroll tax works is not optional for Finnish business owners. It is a legal requirement that affects every pay period, every employee, and your company's standing with the Finnish Tax Administration and pension providers such as Työeläke.fi.

What is payroll tax in Finland and what does it cover?

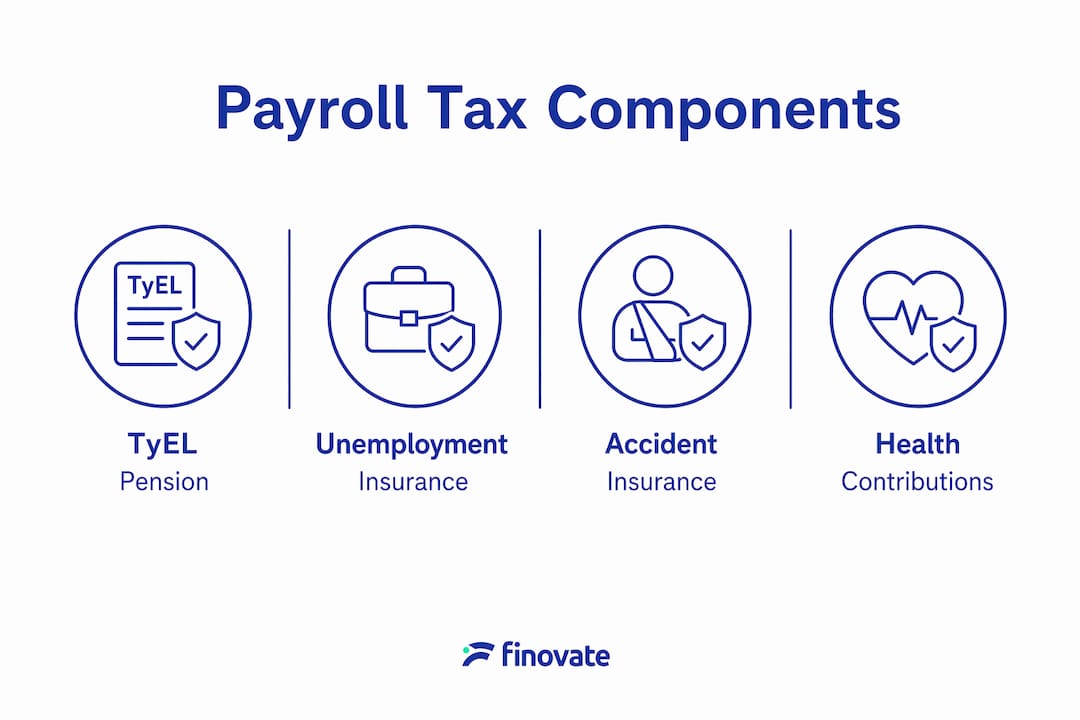

Payroll tax, in the Finnish context, is best understood through its statutory components rather than as a single flat charge. The payroll tax definition here covers a set of mandatory contributions that employers calculate, withhold, and remit on behalf of their employees every pay period.

The primary component is TyEL, the earnings-related pension contribution. Under TyEL, the employee contribution rate in 2026 stands at 7.3% of monthly wages, withheld directly from the employee's pay by the employer. The employer then adds its own share and posts the combined total to the chosen pension insurer. This means you are not simply deducting a figure from a payslip. You are legally responsible for the full remittance.

Beyond TyEL, Finnish employers are also responsible for other statutory social security contributions where applicable, including unemployment insurance contributions and accident insurance premiums. These sit alongside TyEL as part of the broader payroll tax picture.

Key components of Finnish payroll tax include:

- TyEL pension contribution: Employer and employee shares combined, remitted to the pension insurer each pay period.

- Employee withholding: The employer deducts the employee's share (7.3% in 2026) from gross wages before payment.

- Employer's own contribution: Added on top of the withheld employee share before remittance.

- Unemployment insurance contribution: A separate statutory charge calculated on the total wage sum.

- Accident and occupational disease insurance: Mandatory for most employers, calculated as a percentage of wages.

Pro Tip: Review the TyEL rate table published by Työeläke.fi at the start of each calendar year. Rates are confirmed annually, and applying the previous year's figures to your first payroll run is one of the most common and costly errors Finnish employers make.

How payroll tax works: withholding, remittance, and reporting

Managing payroll tax in practice is a withholding-and-remittance workflow that repeats with every pay cycle. Payroll tax compliance is an operational duty, not simply an accounting entry. Here is how the process works for a typical Finnish SME:

- Calculate gross wages for each employee for the pay period, including all taxable salary components.

- Withhold the employee's TyEL share (7.3% in 2026) from gross wages, along with any other applicable employee deductions such as income tax withholding based on the employee's tax card.

- Calculate the employer's TyEL contribution based on the applicable rate for your wage sum category and add it to the withheld employee share.

- Remit the total TyEL contribution to your chosen pension insurer by the agreed deadline. Missing this deadline triggers penalty interest and potential reconciliation failures at the pension provider.

- Report wage and withholding data to the Incomes Register (Tulorekisteri) no later than five calendar days after the payment date. The Finnish Tax Administration draws its data directly from this register.

- File and pay other social insurance contributions according to their respective schedules, including unemployment insurance through the Unemployment Insurance Fund (TVR).

Employers can use services like Palkka.fi to automate notifications to authorities and handle remittance of earnings-related pensions, which significantly reduces the risk of missed deadlines or calculation errors. For businesses with more complex payroll needs, dedicated payroll software or outsourced payroll services provide an additional layer of accuracy.

Pro Tip: Set a recurring calendar reminder two days before each Incomes Register reporting deadline. Late submissions attract automatic penalties from the Finnish Tax Administration, and the five-day window closes faster than most business owners expect.

For a detailed walkthrough of each step, the payroll management guide from Finovate covers the full process specific to Finnish employers.

What are the common payroll tax challenges for Finnish business owners?

Finnish payroll tax is not complicated in principle, but several practical nuances catch business owners off guard. Understanding these in advance protects you from reconciliation failures, penalty charges, and disputes with the Finnish Tax Administration.

Payment classification matters more than most owners realise. Social security contributions are payable only on wage payments. Non-wage payments, such as certain reimbursements or dividends, do not attract employer social security contributions. Misclassifying a payment as wages when it is not, or vice versa, creates either over-remittance or an underpayment that surfaces during audit.

The prepayment register changes your obligations. If the recipient of a payment is registered in the Finnish prepayment register (ennakkoperintärekisteri), you are not required to withhold income tax from that payment. This applies particularly when paying external service providers or contractors. Withholding obligations vary based on payment type and the recipient's registration status, so verifying this before each payment is a sound practice.

Annual rate changes require active management. TyEL contribution rates and the employer/employee split should be reviewed before the first payroll run of each year and payroll procedures updated accordingly. Rates are not static, and a payroll system running on last year's figures will produce incorrect contributions from January onwards.

A common compliance pitfall is treating payroll contributions only as payroll deductions without remitting the employer's portion to pension providers. Even when employee payslips show the correct deduction, missing employer posting causes pension reconciliation failures that can take months to resolve and may result in financial penalties.

For occasional employers, a fixed TyEL rate of 25.85% applies in 2026, rather than the standard split between employer and employee shares. This distinction matters if your business hires staff seasonally or on a one-off basis. Applying the wrong rate structure creates an immediate compliance gap.

The payroll compliance guide for Finnish SMEs from Finovate provides practical checklists for managing these annual transitions without disruption.

How does Finnish payroll tax compare with international systems?

Finnish business owners who operate internationally or hire across borders benefit from understanding how the Finnish payroll tax model differs from other systems. The comparison with the United States is particularly instructive.

| Feature | Finland (TyEL system) | United States (IRS system) |

|---|---|---|

| Primary pension contribution | TyEL: employer and employee shares remitted together to pension insurer | Social Security and Medicare taxes split between employer and employee, paid to IRS |

| Income tax withholding | Withheld based on employee's personal tax card; reported to Incomes Register | Withheld based on W-4 form; deposited with IRS on set schedule |

| Reporting authority | Finnish Tax Administration via Incomes Register (Tulorekisteri) | Internal Revenue Service (IRS) via Form 941 and annual W-2 |

| Unemployment contributions | Paid to Unemployment Insurance Fund (TVR) | Federal and state unemployment taxes (FUTA/SUTA) paid separately |

| Occasional employer rules | Fixed TyEL rate (25.85% in 2026) for irregular employers | No equivalent fixed rate; standard FICA applies regardless of frequency |

US employment taxes include employer deposits and employee withholding for federal income tax, Social Security, Medicare, and unemployment taxes. The structural logic is similar to Finland's, but the administration, rates, and reporting channels differ substantially. A Finnish employer expanding to the US, or a US-owned entity operating in Finland, must treat these as entirely separate compliance frameworks.

The Finnish system's defining feature is the direct relationship between the employer and the pension insurer, rather than routing all contributions through a single tax authority. This makes accurate payroll management in 2026 particularly important, as errors do not surface through a single reconciliation point but across multiple providers and registers.

Key takeaways

Finnish employers carry a dual obligation under payroll tax: withholding the employee's share and remitting the combined total to pension providers and tax authorities every pay period.

| Point | Details |

|---|---|

| TyEL is the core obligation | The employee share (7.3% in 2026) is withheld from wages; the employer adds its own share and remits the total. |

| Annual rate reviews are mandatory | TyEL rates change each year; update your payroll before the first January pay run without exception. |

| Payment classification affects liability | Only wage payments attract social security contributions; non-wage payments and contractor fees follow different rules. |

| Reporting goes to the Incomes Register | Wage and withholding data must reach Tulorekisteri within five calendar days of each payment date. |

| Employer posting is a separate duty | Correct employee deductions on payslips do not satisfy the obligation; the employer must also post its own contribution to the pension insurer. |

Why payroll tax compliance deserves more attention than most Finnish SMEs give it

From working with Finnish business owners across a range of industries, I have noticed a consistent pattern. Most founders understand that payroll tax exists. Far fewer understand that it operates as two distinct obligations running in parallel: the withholding side and the remittance side. These are not the same action, and conflating them is where compliance breaks down.

The most damaging errors I see are not from businesses that ignore payroll tax entirely. They come from businesses that handle the employee-facing side correctly, produce accurate payslips, and then fail to post the employer's TyEL contribution to the pension insurer on time. The employee sees nothing wrong. The payroll records look clean. But the pension reconciliation fails quietly in the background, and the liability compounds.

My honest view is that annual rate changes are underestimated as a compliance risk. Businesses that set up payroll correctly in one year often carry those settings forward without review. TyEL rates shift, the employer/employee split adjusts, and a payroll system running on stale figures produces incorrect contributions from the first pay run of the year. Checking the updated TyEL rates before January payroll is a ten-minute task that prevents months of correction work.

For SMEs without a dedicated finance function, outsourcing payroll to a specialist is not a luxury. It is the most cost-effective way to keep both the withholding and remittance obligations accurate, current, and documented. The cost of a payroll error, measured in penalty interest, correction filings, and management time, consistently exceeds the cost of professional support. That calculation rarely changes regardless of company size.

— Busayo

Let Finovate handle your payroll tax compliance

Managing payroll tax correctly takes time, attention to detail, and up-to-date knowledge of Finnish statutory rates. Finovate provides payroll accounting and invoicing services designed specifically for Finnish SMEs and entrepreneurs, covering TyEL remittance, Incomes Register reporting, and annual rate updates so nothing falls through the gaps.

Whether you are running payroll for the first time or reviewing an existing process that has grown more complex, Finovate's team handles the calculations, deadlines, and reporting on your behalf. Our monthly invoicing service gives you a fixed, predictable cost for payroll and invoicing support each month. If you prefer a percentage-based arrangement, the Invoicing Service Pro is built for businesses with higher transaction volumes. Contact Finovate to discuss which option fits your payroll structure.

FAQ

What is the payroll tax definition in Finland?

Payroll tax in Finland refers to the statutory employer obligation to withhold employee contributions from wages and remit the combined employer and employee total to pension insurers and tax authorities. The primary component is the TyEL earnings-related pension contribution under the Employees Pensions Act.

Do I have to pay payroll tax as a Finnish employer?

Yes. Any employer paying wages to private-sector employees in Finland is required to calculate, withhold, and remit TyEL contributions, along with other applicable social security contributions. Occasional employers apply a fixed TyEL rate of 25.85% in 2026.

What is the difference between payroll tax and income tax in Finland?

Payroll tax covers statutory pension and social security contributions remitted to pension insurers and the Unemployment Insurance Fund. Income tax is withheld from employee wages based on a personal tax card and reported to the Finnish Tax Administration via the Incomes Register. Both are withheld by the employer, but they go to different authorities and serve different purposes.

How are TyEL payroll tax rates set each year?

TyEL contribution rates are confirmed annually and depend on the employee's wage level and the employer's wage sum category. Employers must review and update their payroll settings before the first pay run of each new year to reflect the current rates.

What happens if I withhold correctly but forget to remit the employer's TyEL share?

Correct employee deductions on payslips do not fulfil the full TyEL obligation. If the employer's own contribution is not posted to the pension insurer, a reconciliation failure occurs at the insurer's end, which can result in penalty interest and a formal correction process with Työeläke.fi.