TL;DR:

- Accrual accounting records revenues and expenses when they are earned or incurred, not when cash is received or paid. It provides a more accurate picture of business performance and is required for audited financial statements. Small businesses should adopt accrual accounting early to improve financial clarity and decision-making.

Accrual accounting is defined as the method of recording revenues and expenses when they are earned or incurred, regardless of when cash is received or paid. This approach, required under both GAAP and IFRS, gives your financial statements a far more accurate picture of business performance than cash accounting ever can. For entrepreneurs and small business owners, understanding this method is the foundation of sound financial management. Whether you are invoicing clients, managing payroll, or planning for growth, accrual accounting principles shape how your numbers tell your story.

What is accrual accounting and how does it work in practice?

Accrual accounting records revenue when it is earned and expenses when they are incurred. The timing of cash movement is irrelevant to when the transaction is recorded. This is the core distinction that separates accrual accounting from cash basis accounting, and it is what makes accrual the standard for audited financial statements worldwide.

Two principles drive the entire system.

The matching principle

The matching principle requires you to recognise expenses in the same reporting period as the revenues they help generate. If you pay a supplier in january for goods delivered in march, the expense belongs in march, not january. This avoids distortions caused by cash flow timing and ensures your profit figures reflect actual business activity.

Revenue recognition

Revenue is recognised when goods or services are delivered, not when payment arrives. Say you ship a product to a client in march but receive payment in may. Under accrual accounting, you record the revenue in march. Your accounts receivable balance captures the outstanding payment until it clears.

Journal entries in practice

The mechanics follow a consistent pattern. When you earn income, you debit accounts receivable and credit revenue. When you incur an expense, you debit the expense account and credit accounts payable. Cash receipts later clear receivables; payments clear payables. At month end, you record accrued income and expenses for any transactions not yet invoiced or paid. These entries are then reversed when the actual invoice or cash flow occurs, preventing double counting and keeping your income statement aligned to real economic events.

Here is a numbered summary of the core steps in an accrual accounting cycle:

- Record revenue when goods or services are delivered, creating an accounts receivable entry.

- Record expenses when incurred, creating an accounts payable entry.

- At period end, post adjusting entries for accrued but uninvoiced revenues and expenses.

- Reverse those adjusting entries in the next period when invoices or payments arrive.

- Reconcile subledgers for receivables and payables to confirm your balance sheet is accurate.

Pro Tip: Set a fixed month-end close date and run your accrual reversals on the first working day of the new period. This prevents the same transaction appearing twice and keeps your profit and loss statement clean.

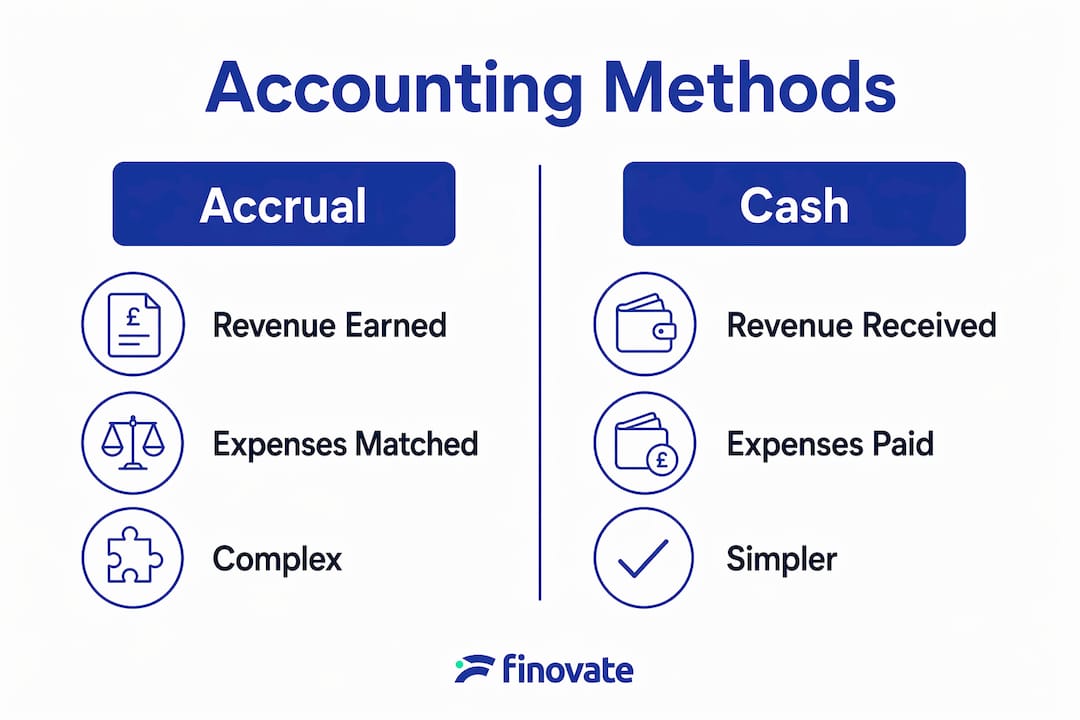

Accrual vs cash accounting: what is the difference?

Cash accounting records transactions only when money physically moves. You receive payment, you record income. You pay a bill, you record an expense. The simplicity appeals to many sole traders and very small businesses. The problem is that cash accounting can make a profitable month look poor if clients pay late, or make a loss-making month look healthy if you delay paying suppliers.

Accrual accounting removes that distortion. Your financial statements reflect what you have earned and what you owe, not just what has landed in your bank account. This matters enormously when you are seeking investment, applying for a loan, or preparing audited accounts.

Here are the key practical differences between the two methods:

- Timing of income: Accrual records income on delivery; cash records it on receipt.

- Timing of expenses: Accrual records expenses when incurred; cash records them when paid.

- Financial accuracy: Accrual reflects assets, liabilities, and true profitability; cash reflects only bank movements.

- Tax implications: Accrual accounting reduces your ability to shift taxable income between periods, since revenue is taxable when earned, not when received.

- Compliance: Accrual is required for audited statements under GAAP and IFRS; cash accounting is not accepted for external reporting.

- Suitability: Cash accounting suits very small businesses with simple transactions; accrual suits any business with credit sales, inventory, or growth ambitions.

| Feature | Accrual accounting | Cash accounting |

|---|---|---|

| Revenue recorded | When earned | When received |

| Expenses recorded | When incurred | When paid |

| Financial picture | Complete: assets, liabilities, profit | Partial: cash position only |

| Required for audits | Yes, under GAAP and IFRS | No |

| Complexity | Higher | Lower |

| Best suited to | Growing businesses, credit sales | Sole traders, simple cash transactions |

For a deeper look at how these methods compare in a Finnish context, Finovate has published a practical guide on cash accounting in Finland that is worth reading alongside this article.

What are the benefits and challenges of accrual accounting?

Accrual accounting provides a more accurate financial picture than cash accounting, capturing profitability alongside balance sheet details such as assets and liabilities. That accuracy is not just useful for compliance. It is the information you need to make sound decisions about hiring, investment, and pricing.

The key benefits for small businesses include:

- Accurate profit reporting: Your income statement reflects what you have genuinely earned in a period, not what happened to land in your account.

- Better planning: You can see outstanding receivables and payables clearly, which supports cash flow forecasting.

- Investor and lender confidence: Audited accrual accounts carry far more weight with banks and investors than cash basis records.

- Compliance readiness: Accrual accounting is required under GAAP and IFRS, so adopting it early avoids a disruptive switch later.

The challenges are real and worth acknowledging honestly.

- Complexity: Accrual accounting involves adjusting entries, deferrals, and accruals, which require accounting knowledge that many small business owners do not have in-house.

- Cash flow blind spots: A business can show strong accrual profits while struggling with cash. You need to monitor cash flow separately.

- Time and resource cost: Month-end close processes, subledger reconciliations, and reversing entries take time. Without the right support, errors accumulate.

A common misconception is that accrual accounting is simply about timing. The matching principle goes further than that. It requires you to align expenses with the revenues they support, which sometimes means spreading costs across multiple periods. Getting this wrong creates operational risks and distorts your financial reports.

Pro Tip: Never rely solely on your profit and loss statement if you use accrual accounting. Always review your cash flow statement alongside it. Profit and cash are two different things, and confusing them is one of the most common financial mistakes small business owners make.

How can small businesses implement accrual accounting effectively?

Setting up accrual accounting correctly from the start saves significant time and cost later. The process is manageable when broken into clear steps.

Track accounts receivable and payable from day one

Every credit sale creates an accounts receivable entry. Every unpaid bill creates an accounts payable entry. Maintaining detailed subledger data for both is non-negotiable. This includes tracking amounts that are accrued but not yet invoiced, which is where many small businesses fall short.

Use accounting software

Accounting software handles the repetitive journal entry work and reduces the risk of human error. Platforms such as Xero, QuickBooks, and Netvisor (widely used in Finland) automate recurring entries, flag unreconciled items, and generate period-end reports. Choosing software that supports accrual accounting natively is far preferable to adapting a cash-based tool.

Perform regular period-end close processes

Month-end close is where accrual accounting earns its value. Post adjusting entries for any revenue earned but not invoiced and any expenses incurred but not yet billed. Then reverse those entries at the start of the next period to prevent double counting. Skipping this step is the single most common cause of inaccurate financial statements in small businesses.

Avoid common pitfalls

- Do not record revenue when you raise an invoice if the goods or services have not yet been delivered. Revenue is earned on delivery, not on invoicing.

- Do not defer expenses simply because you have not yet paid them. If the obligation exists, record it.

- Do not mix personal and business transactions in the same accounts. This creates reconciliation problems that compound over time.

- Review your accounts receivable ageing report monthly. Unrecovered receivables distort your profit figures and mask cash flow problems.

For a step-by-step walkthrough of the full accounting cycle, Finovate's guide on the accounting cycle for Finnish SMEs provides practical context for entrepreneurs at every stage.

Key takeaways

Accrual accounting gives entrepreneurs an accurate, complete view of financial performance by recording revenues and expenses when they occur, not when cash moves.

| Point | Details |

|---|---|

| Core definition | Revenue and expenses are recorded when earned or incurred, not when cash is exchanged. |

| Matching principle | Expenses must align with the revenues they support within the same reporting period. |

| Accrual vs cash | Accrual reflects true profitability and liabilities; cash accounting only shows bank movements. |

| Key challenge | Complexity requires accounting expertise, regular adjusting entries, and subledger discipline. |

| Implementation priority | Use accounting software, perform month-end close consistently, and track receivables and payables in detail. |

Why accrual accounting matters more than most entrepreneurs realise

From working with entrepreneurs across Finland, the pattern I see most often is this: a business owner switches from cash to accrual accounting only when forced to, usually by a bank, an investor, or an auditor. By that point, they are looking back at months of records that need restating. The transition is painful and expensive.

What I find more interesting is how much accrual accounting changes the way you think about your business. When you can see your outstanding receivables, your accrued liabilities, and your true profit in one place, you stop making decisions based on your bank balance. That shift in perspective is genuinely valuable. It is not just a compliance exercise.

The misconception I push back on most firmly is the idea that accrual accounting is too complex for small businesses. The complexity is real, but it is manageable with the right support. The alternative, running a growing business on cash accounting, creates a false sense of security. You may show a healthy bank balance while sitting on unpaid obligations that will hit you in the next period.

My advice is straightforward. Adopt accrual accounting early, get proper bookkeeping support, and treat your month-end close as a non-negotiable discipline. The financial clarity it provides is worth every bit of the effort.

— Busayo

How Finovate supports your accrual accounting needs

Managing accrual accounting correctly takes consistent effort, particularly when you are running a business at the same time.

Finovate provides bookkeeping, invoicing, and accounting services designed specifically for entrepreneurs and small businesses in Finland. Our monthly invoicing service handles accounts receivable management and revenue recognition, so your records stay accurate without the administrative burden falling on you. We also offer business advisory support to help you interpret your accrual-based financial statements and make better decisions. If you are ready to move beyond cash accounting and build a financial reporting process you can rely on, we are here to help you do that.

FAQ

What is the accrual accounting definition in simple terms?

Accrual accounting records revenue when it is earned and expenses when they are incurred, regardless of when cash is received or paid. It gives a complete picture of financial performance within a given period.

What are accruals in accounting?

Accruals are entries made for revenues earned or expenses incurred that have not yet been invoiced or paid. They are recorded at period end and typically reversed when the actual invoice or payment arrives.

Is accrual accounting required for small businesses?

Accrual accounting is required under GAAP and IFRS for audited financial statements. Small businesses not subject to audit may use cash accounting, but accrual is strongly recommended for any business with credit sales or growth plans.

What is the difference between accrual and cash accounting?

Cash accounting records transactions when money moves; accrual accounting records them when they are earned or incurred. Accrual provides a more accurate financial picture, including assets, liabilities, and true profitability.

How does accrual accounting affect tax reporting?

Accrual accounting means revenue is taxable when earned, not when received. This reduces the ability to shift taxable income between periods compared with cash accounting, which can affect your tax planning strategy.