TL;DR:

- Taxable income is the net amount used to calculate Finnish tax after allowable deductions and exemptions. It differs from gross income, with deductions like tulonhankkimisvähennys reducing taxable income and leading to a lower tax bill. For small business owners, understanding how net assets influence business income taxation can lead to significant tax planning advantages.

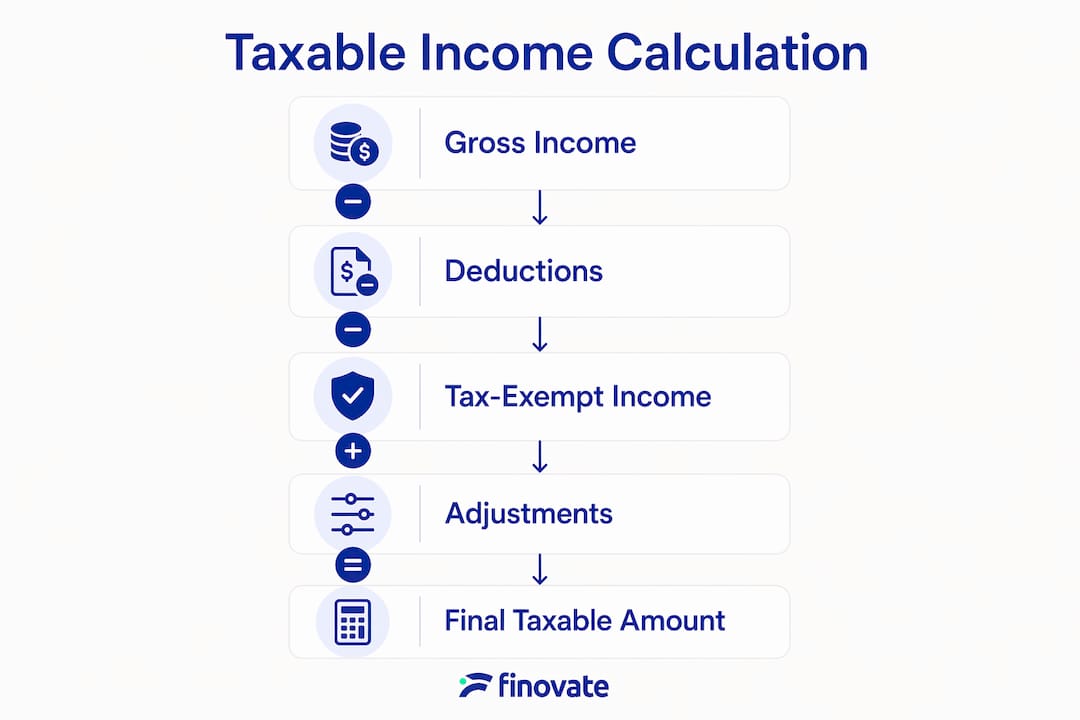

Taxable income (verotettava tulo) is defined as the portion of your total earnings on which Finnish tax is actually calculated, after allowable deductions and exemptions have been applied. This figure is not the same as your gross income, and confusing the two is one of the most common and costly mistakes Finnish taxpayers make. Whether you are an employee, a sole trader, or a limited company owner, understanding taxable income is the foundation of accurate tax filing and sound financial planning. This guide covers what counts as taxable, how deductions reduce your tax base, and what small business owners in Finland need to know before submitting their annual declaration.

Taxable income explained: what it means in Finland

Taxable income is the net figure remaining after you subtract allowable deductions and tax-exempt amounts from your gross earnings. For individuals, it covers both earned income and capital income after permitted adjustments. For businesses, it reflects the net result of operations under elinkeinoverolaki (Finland's business taxation law), minus deductible expenses. The Finnish Tax Administration (Vero) uses this adjusted figure, not your gross pay, to determine how much tax you owe.

The distinction between gross income and taxable income matters enormously in practice. A salaried employee earning €45,000 per year does not pay tax on the full €45,000. Automatic deductions, social contributions, and specific allowances reduce that figure before the tax rate is applied. The gap between gross and taxable income can be several thousand euros, which translates directly into a lower tax bill.

What income types count as taxable in Finland?

Finnish tax law divides income into two main categories: earned income (ansiotulo) and capital income (pääomatulo). Each is taxed differently, and knowing which category your income falls into affects both your rate and your available deductions.

Earned income includes:

- Wages and salaries from employment

- Self-employment and business profits for sole traders

- Pensions and certain social benefits

- Benefits in kind, such as a company car or meal vouchers

Capital income includes:

- Rental income from property

- Dividends (subject to specific rules)

- Capital gains from selling assets

- Interest income above the tax-free threshold

Certain income sources are entirely tax-exempt and must be excluded from your taxable base. Scholarships from public funds, certain social benefits such as child benefit (lapsilisä), and some compensation payments fall outside the tax base. Tax-exempt income does not count towards your taxable income, but it must still be reported separately on your tax return. Failing to report it correctly can trigger queries from Vero even if no tax is owed.

Pro Tip: If you receive rental income alongside a salary, these are both taxable but treated differently. Rental income is capital income taxed at 30% (or 34% above €30,000), while your salary is subject to progressive earned income tax. Keep these streams clearly separated in your records.

How to calculate taxable income: deductions and adjustments

Reducing your taxable income legally depends on claiming every deduction you are entitled to. Finnish tax law provides several categories of allowable deductions, and missing even one can mean overpaying tax.

The main steps in calculating taxable income for an individual are:

- Start with gross earned income. Include all wages, benefits in kind, and pension income for the tax year.

- Subtract the income acquisition deduction (tulonhankkimisvähennys). This automatic deduction is a minimum of €750 for employees but can be claimed at the actual amount if your work-related expenses exceed this figure. Costs such as tools, professional subscriptions, or a home office used exclusively for work qualify.

- Deduct work-related travel costs. Commuting expenses between home and work are deductible above a set annual threshold, using the cheapest available mode of transport as the reference.

- Apply personal allowances. These include the basic deduction (perusvähennys) and the earned income deduction (ansiotulovähennys), which are calculated automatically by Vero based on your income level.

- Account for social insurance contributions. Mandatory TyEL (pension) and TVM (health insurance) contributions are factored into the tax card calculation, though they are technically separate from income tax itself.

- Subtract any other allowable deductions. These include certain education costs, interest on a first home loan, and voluntary pension contributions up to the annual limit.

For businesses, the process differs. Accurate taxable income requires a clear understanding of which costs are deductible under elinkeinoverolaki and which are not. VAT is excluded from business taxable income entirely. Non-deductible costs include fines, personal expenses passed through the business, and entertainment costs above the permitted limit.

Pro Tip: Keep receipts and records for every expense you intend to deduct. Vero can request documentation up to five years after the tax year in question. A simple folder system, whether physical or digital, saves significant stress at filing time.

How does taxable income affect your tax rate and net earnings?

Finland operates a progressive income tax system, meaning the more you earn, the higher the rate applied to each additional euro. Understanding this relationship helps you estimate your real tax burden and plan your finances accordingly.

Finnish income tax comprises four components:

- State income tax (valtionvero): Progressive rates applied to earned income above a threshold

- Municipal tax (kunnallisvero): A flat rate set by your municipality, typically between 4.4% and 10.8% in 2026

- Church tax (kirkollisvero): Applies to members of the Evangelical Lutheran or Orthodox churches

- YLE tax: A flat contribution to public broadcasting, capped at €163 per year

The concept of the marginal tax rate is particularly useful for planning. Finnish progressive taxation means your marginal rate indicates the tax applied to each additional euro earned, not your average rate across all income. A taxpayer with €40,000 in taxable earned income may have an effective rate of around 25%, but their marginal rate on the top slice of income could be closer to 40% when municipal and state taxes are combined.

| Gross income (€) | Approximate taxable income (€) | Estimated effective tax rate |

|---|---|---|

| 25,000 | 21,500 | ~18% |

| 40,000 | 35,000 | ~25% |

| 60,000 | 54,000 | ~32% |

| 80,000 | 72,000 | ~38% |

Note: Figures are illustrative estimates. Actual rates depend on municipality, deductions claimed, and individual circumstances.

The tax card withholding percentage shown on your verokortti is only an estimate. It does not account for mandatory TyEL and TVM contributions, which together amount to approximately 8.2% of gross pay. This means your actual take-home pay is lower than the tax card alone suggests. Using Vero's veroprosenttilaskuri (tax percentage calculator) gives a more accurate picture of your real net income.

Special considerations for small business owners in Finland

For small business owners, the taxable income calculation is more complex than for employees, and the stakes are higher. The structure of your business determines how income is taxed and what planning options are available to you.

Sole traders (toiminimi) report business income directly on their personal tax return. Revenue minus allowable business expenses produces the net business profit, which is then split between earned income and capital income based on the business's net assets (nettovarallisuus). Up to 20% of net assets can be treated as capital income, taxed at 30% or 34%, rather than as earned income subject to progressive rates. This choice is made annually in the tax declaration and can produce meaningful savings when net assets are substantial.

Limited companies (osakeyhtiö) are taxed as separate legal entities at a flat corporate tax rate of 20%. The owner then pays personal tax on any salary drawn from the company and on dividends received. Dividend taxation from a non-listed company is partially tax-exempt depending on the dividend amount relative to the company's net assets, making the salary-versus-dividend balance a central tax planning decision.

Key points for small business owners to keep in mind:

- Business expenses must be directly connected to income generation to qualify as deductible under elinkeinoverolaki

- VAT collected from customers is not part of taxable business income and must be reported separately

- Bookkeeping must be maintained throughout the year, not assembled retrospectively at filing time

- The tax preparation process for small businesses involves separate VAT declarations, income tax returns, and potentially payroll reporting

For partnerships (avoin yhtiö and kommandiittiyhtiö), profits are allocated to partners and taxed as their personal income, again split between earned and capital income based on net assets. The rules for Finnish entrepreneurs across all structures reward those who understand the mechanics and plan accordingly.

Key takeaways

Taxable income in Finland is always lower than gross income, and the gap is determined by the deductions, exemptions, and structural choices available under Finnish tax law.

| Point | Details |

|---|---|

| Taxable income vs gross income | Taxable income is gross income minus allowable deductions, exemptions, and adjustments. |

| Two income categories | Earned income and capital income are taxed at different rates and have separate deduction rules. |

| Deductions reduce your tax base | Claiming tulonhankkimisvähennys and other allowances directly lowers the income on which tax is calculated. |

| Business structure matters | Sole traders, limited companies, and partnerships each face different taxable income rules and planning options. |

| Net assets affect business taxation | For sole traders, up to 20% of net assets can be treated as lower-taxed capital income annually. |

Why getting taxable income right is worth the effort

Most people I work with arrive with a vague sense that their tax card percentage is "their tax rate." It is not, and that misunderstanding costs them money in two directions. Some overpay because they never claim deductions they are entitled to. Others underpay because they have not accounted for social contributions sitting outside the tax card, and then face a supplementary tax demand in the autumn.

The detail that surprises people most is how much the municipal tax rate varies. Moving from a municipality with a 5% rate to one with a 9% rate on the same taxable income is a difference of thousands of euros per year. That is not a technicality. It is a real financial consideration for anyone with flexibility over where they register.

For small business owners, the nettovarallisuus calculation is the most underused planning tool I encounter. Many sole traders default to treating all business profit as earned income simply because they do not know the capital income option exists, or they do not maintain the records needed to support the claim. The annual choice to elect capital income treatment on up to 20% of net assets is worth modelling every year, not just once.

My honest advice: review your tax return before the pre-filled deadline, not after. Vero's pre-filled return is a starting point, not a finished document. It rarely includes all the deductions you are entitled to, and correcting it after the deadline is more work than checking it beforehand. Plan once a year, update your records continuously, and the process becomes straightforward.

— Busayo

Let Finovate handle your taxable income calculations

Calculating taxable income accurately takes time, and the rules change each year. Finovate provides tax preparation, bookkeeping, payroll processing, and business advisory services to individuals and small business owners across Finland.

Whether you are filing as an employee, a sole trader, or a limited company, our team ensures your deductions are correctly applied, your income is properly categorised, and your return is submitted on time. We also support light entrepreneurs through our invoicing and accounting service, making tax compliance straightforward regardless of how you work. Visit Finovate to explore our services and speak with an adviser who understands Finnish tax law in detail.

FAQ

What is taxable income in Finland?

Taxable income (verotettava tulo) is the amount of income on which Finnish tax is calculated, after deducting allowable expenses and exemptions from gross earnings. It includes both earned income and capital income, adjusted according to Finnish tax law.

How is taxable income different from gross income?

Gross income is your total earnings before any adjustments. Taxable income is the lower figure that remains after subtracting deductions such as tulonhankkimisvähennys, travel costs, and personal allowances. The difference between the two directly reduces your tax liability.

Which income is tax-exempt in Finland?

Scholarships from public funds, child benefit (lapsilisä), and certain social compensation payments are tax-exempt and excluded from the taxable base. These amounts must still be reported separately on your tax return even though no tax is owed on them.

How do small business owners calculate taxable income?

Sole traders calculate taxable income by subtracting allowable business expenses from total revenue. Part of the resulting profit can be treated as capital income based on the business's net assets, with up to 20% of net assets eligible for the lower capital income tax rate annually.

Does my tax card percentage reflect my actual tax burden?

No. The verokortti withholding percentage is an estimate and does not include mandatory TyEL and TVM social contributions, which amount to approximately 8.2% of gross pay. Your actual deductions from gross income are higher than the tax card figure alone suggests.