TL;DR:

- Effective SME financial management involves regular cash flow monitoring, accurate bookkeeping, and proactive financial reporting.

- Finnish SMEs should maintain at least three months of operating expenses in liquid reserves and automate receivables to improve cash flow.

SME financial management is defined as the structured process of planning, organising, directing, and controlling all financial activities within a small or medium-sized enterprise to sustain cash flow, profitability, and growth. For Finnish business owners, understanding SME finance is not optional. It is the operational backbone that determines whether your business survives a slow quarter, qualifies for a bank loan, or scales with confidence. This guide covers the core principles of financial management for SMEs, from budgeting and bookkeeping to funding options and key metrics, with practical guidance tailored to Finland's business environment.

What are the essential components of SME financial management?

Financial management for SMEs rests on five interconnected pillars. Each one feeds the others, and weakness in any single area creates risk across the whole business.

Cash flow management is the most immediate concern. A profitable business can go bankrupt without sufficient cash reserves. Managing the timing of inflows and outflows is critical, which is why the 13-week cash flow forecast updated every Monday is the gold standard for SME liquidity control. This rolling forecast gives you a clear, short-term view of your financial position before problems become crises.

Bookkeeping and accounting accuracy form the foundation of every other financial decision. Without clean, up-to-date records, you cannot produce reliable reports, plan taxes, or assess profitability. Tools like Xero and QuickBooks automate much of this work, reducing manual errors and saving hours each month. Consistent bookkeeping routines are particularly valuable for Finnish SMEs managing VAT reporting and payroll obligations.

Financial reporting translates raw data into decisions. The four critical monthly statements every SME needs are the profit and loss account, the balance sheet, the cash flow statement, and the budget versus actual report. Each serves a distinct purpose: the P&L shows trading performance, the balance sheet shows financial position, the cash flow statement tracks liquidity, and the budget comparison reveals where reality diverged from your plan.

Budgeting and forecasting are not the same thing. A budget is a fixed plan for the year. A forecast is a living document updated as conditions change. Monthly budget reviews with rolling quarterly forecasts and scenario planning are the standard practice for well-managed SMEs.

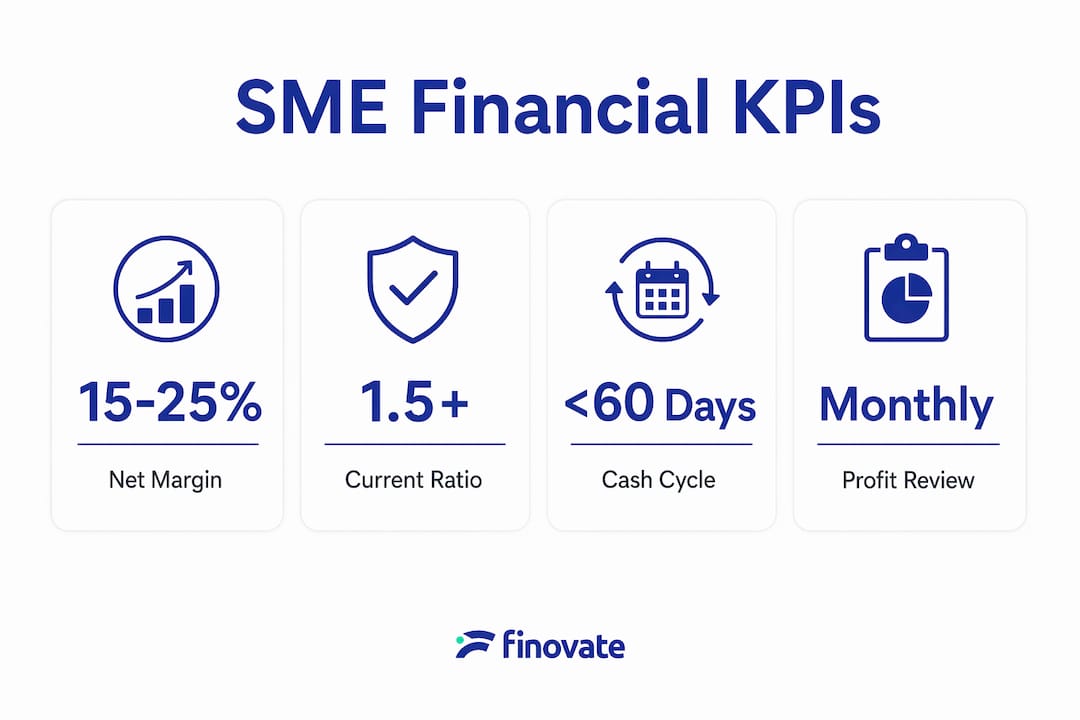

Key performance indicators (KPIs) give you a shorthand view of business health. The most relevant for SMEs include gross profit margin, net profit margin, debtor days, and current ratio.

| KPI | What it measures | Healthy benchmark |

|---|---|---|

| Net profit margin | Profit after all costs | 15-25% (services), 5-15% (product) |

| Debtor days | Average time to collect payment | Under 30 days |

| Current ratio | Short-term assets vs liabilities | Above 1.5 |

| Budget variance | Actual vs planned spend | Investigate if above 10% |

Pro Tip: A monthly variance above 10% in any budget line is a signal to investigate immediately, not at year end. Catching the cause early prevents small issues from compounding into significant losses.

How can Finnish SMEs implement effective financial management practices?

Translating financial principles into daily habits is where most SME owners struggle. The following steps create a practical framework you can apply from this month.

-

Separate personal and business finances from day one. Mixing accounts is one of the most common and costly mistakes Finnish SME owners make. Separation is essential for correct bookkeeping, tax compliance, and accurate profitability tracking. Open a dedicated business current account and use it exclusively for business transactions.

-

Choose and implement accounting software. Xero and QuickBooks both integrate with Finnish banking systems and support VAT reporting. Digital accounting tools reduce manual data entry, improve accuracy, and produce the financial reports you need without hiring a full-time accountant.

-

Establish a review cycle. Update your 13-week cash flow forecast weekly. Review management accounts monthly. Conduct a full profitability and tax review quarterly. This rhythm keeps you informed and prevents surprises at year end.

-

Build a cash reserve. Maintain at least 3 months of operating expenses in liquid reserves. This buffer protects you from late-paying clients, seasonal dips, or unexpected costs without forcing you into emergency borrowing.

-

Automate invoice reminders. Set automated reminders at 7, 14, and 30 days after invoice issue. Late payments are the single most common cause of SME cash flow problems in Finland, and automation removes the discomfort of chasing clients manually.

-

Plan your own compensation. Owner salary must be treated as a fixed operating expense, not whatever is left over at month end. Planned compensation gives you accurate profitability data and prevents erratic cash withdrawals that distort your financial picture.

-

Engage a professional adviser at growth stages. When you hire your first employee, register for VAT, or consider external financing, professional guidance prevents costly compliance errors and improves your financial decision-making.

Pro Tip: Shorten your standard payment terms to 14 days rather than 30. Combined with automated reminders, this single change can reduce average debtor days significantly and improve monthly cash flow without any additional cost.

Which financial tools and funding options should SMEs compare?

Understanding your financing options is a core part of small business financial planning. Each funding type carries different costs, speeds, and eligibility requirements.

- Bank loans offer lower interest rates and longer repayment terms but require strong credit history, collateral, and detailed financial documentation. Finnish banks such as OP and Nordea offer SME lending products, but approval timelines can extend to several weeks.

- Invoice financing converts outstanding invoices into immediate cash. It is faster than a bank loan and does not require collateral beyond the invoices themselves. The cost is typically a percentage of the invoice value, making it more expensive than traditional debt but far quicker.

- Equity financing involves selling a share of your business to investors in exchange for capital. Venture capital and angel investment are available to high-growth Finnish SMEs, particularly through networks like Business Finland and Slush. The trade-off is dilution of ownership and the expectation of significant returns.

- Fintech lenders such as Qred and Ferratum operate in Finland and offer faster credit decisions than traditional banks, often based on revenue data rather than credit scores. Interest rates are higher, but the speed and accessibility suit SMEs with short-term funding needs.

One critical barrier to financing is what the Bank of England describes as information asymmetry between SMEs and lenders. Unlike large corporations, most SMEs are not monitored by credit rating agencies. This means lenders rely entirely on the financial records you provide. Maintaining digital, audit-ready records is not just good practice. It is your primary tool for accessing capital on favourable terms.

| Funding type | Cost | Speed | Best suited for |

|---|---|---|---|

| Bank loan | Low to medium | Slow (weeks) | Established SMEs with assets |

| Invoice financing | Medium | Fast (days) | SMEs with B2B receivables |

| Equity investment | High (ownership) | Variable | High-growth startups |

| Fintech lending | High | Very fast | Short-term working capital |

Business Finland also administers grants and subsidised loans for qualifying SMEs, particularly those involved in innovation or internationalisation. These are worth investigating before taking on commercial debt.

What financial challenges do Finnish SMEs commonly face?

The most frequent financial management challenges Finnish SME owners encounter are predictable, and most are preventable with the right systems in place.

- Late payments and cash flow gaps. Finnish businesses operate under standard 30-day payment terms, but many invoices are paid late. A single large unpaid invoice can create a cash shortfall that forces you to delay supplier payments or miss payroll. Automated reminders and shorter payment terms are the most direct solution.

- Mixing personal and business finances. This creates confusion in bookkeeping, inflates apparent business costs, and complicates tax preparation. It is also a red flag for lenders reviewing your accounts.

- Unplanned owner withdrawals. Taking money from the business without a structured compensation plan distorts your profit figures and makes cash flow unpredictable. Treat your own salary as a fixed monthly cost.

- Reactive rather than proactive financial management. Many SME owners only review their finances when something goes wrong. Monthly management account reviews and quarterly scenario planning shift you from reactive to proactive, giving you time to respond to problems before they become critical.

- Poor documentation for financing. Without organised, up-to-date financial records, accessing bank loans or investor funding becomes significantly harder. Maintaining clean accounts year-round removes this barrier when you need capital quickly.

Pro Tip: Run at least two scenarios in your quarterly forecast: one where your largest client delays payment by 60 days, and one where a key cost increases by 15%. If either scenario creates a cash crisis, you need to adjust your reserves or credit facilities now, not when it happens.

How do financial metrics and reports guide SME decisions?

Financial reports are only useful if you act on what they tell you. The following metrics and reports directly inform the decisions Finnish SME owners face most often.

Gross profit margin reveals whether your core product or service is priced correctly relative to its direct costs. A declining gross margin signals either rising costs or pricing pressure, both of which require a response before they erode net profit.

Net profit margin shows what remains after all expenses. Service-based SMEs should target 15 to 25% net margin; product and e-commerce businesses typically achieve 5 to 15%. Knowing your benchmark tells you whether your business is performing in line with its sector.

Cash conversion cycle measures how quickly you turn sales into cash. A long cycle means you are funding your operations with your own capital while waiting for clients to pay. Shortening debtor days and managing stock levels are the two levers that reduce this cycle.

Liquidity ratios confirm whether you can meet short-term obligations. A current ratio above 1.5 means your short-term assets comfortably cover your liabilities. Below 1.0 signals a potential solvency risk.

The budget versus actual report is the most underused tool in SME financial management. Reviewed monthly, it shows exactly where your business is over or underspending relative to plan. This early warning system allows you to adjust hiring decisions, pricing, or marketing spend before a variance becomes a structural problem. For a practical approach to building business budgets, a step-by-step framework helps Finnish SME owners set realistic targets and track performance consistently.

| Report | Primary use | Review frequency |

|---|---|---|

| Profit and loss | Trading performance | Monthly |

| Balance sheet | Financial position | Monthly |

| Cash flow statement | Liquidity tracking | Weekly or monthly |

| Budget vs actual | Variance detection | Monthly |

Key takeaways

Effective SME financial management requires consistent cash flow monitoring, clean bookkeeping, structured budgeting, and proactive use of financial reports to guide every major business decision.

| Point | Details |

|---|---|

| Cash reserves are non-negotiable | Maintain at least 3 months of operating expenses in liquid reserves to protect against late payments and downturns. |

| Automate receivables management | Set invoice reminders at 7, 14, and 30 days to reduce late payments and improve monthly cash flow. |

| Separate finances from the start | Personal and business accounts must be kept separate for accurate bookkeeping and tax compliance. |

| Plan owner compensation as a fixed cost | Treating your salary as a planned expense gives you accurate profit data and prevents cash flow distortion. |

| Digital records unlock financing | Audit-ready financial documentation is your primary tool for overcoming lender information gaps and accessing capital. |

Why financial discipline matters more than financial knowledge

I have worked with Finnish SME owners who understand financial theory perfectly but still face cash crises every quarter. The gap is almost never knowledge. It is consistency. Reviewing your accounts once a year is not financial management. It is damage assessment.

The SME owners I see thrive financially are not necessarily the ones with the most sophisticated systems. They are the ones who review their cash flow every week, update their forecasts when conditions change, and treat their monthly management accounts as a decision-making tool rather than a compliance obligation. That discipline, applied consistently, produces better outcomes than any single piece of software or advice.

Digital tools like Xero have genuinely changed what is possible for small businesses. Automation removes the friction from bookkeeping, invoicing, and reporting, which means there is less excuse than ever for operating without current financial data. But the tool only works if you engage with what it produces.

My strongest recommendation for any Finnish SME owner is to engage a professional adviser before you think you need one. The cost of early advice is a fraction of the cost of correcting a tax compliance error, restructuring poorly managed debt, or losing a financing opportunity because your records were not in order. Good financial management builds confidence. It gives you the clarity to make decisions quickly and the evidence to back them up.

— Busayo

How Finovate supports Finnish SMEs with financial management

Managing your finances well requires the right support structure, particularly as your business grows and compliance obligations increase.

Finovate provides Finnish SMEs with expert accounting and tax services covering bookkeeping, VAT reporting, payroll processing, and tax planning. For business owners who invoice clients directly, Finovate's monthly invoicing service handles the administrative side of receivables management, freeing you to focus on running your business. For those who need a more flexible arrangement, the pro invoicing option offers a percentage-based model suited to variable income. Whether you need full bookkeeping support or targeted advice at a growth stage, Finovate's services are designed specifically for the Finnish SME context.

FAQ

What is SME financial management?

SME financial management is the process of planning, organising, directing, and controlling all financial activities within a small or medium-sized enterprise. It covers cash flow management, budgeting, financial reporting, tax planning, and access to financing.

How much cash reserve should a Finnish SME maintain?

A Finnish SME should maintain at least 3 months of operating expenses in liquid reserves. This buffer protects the business from late client payments, seasonal revenue dips, and unexpected costs without requiring emergency borrowing.

What financial reports does an SME need every month?

The four monthly reports every SME needs are the profit and loss account, the balance sheet, the cash flow statement, and the budget versus actual report. Together, these give a complete picture of trading performance, financial position, and spending discipline.

How does information asymmetry affect SME financing?

SMEs are not monitored by credit rating agencies, which means lenders rely entirely on the financial records the business provides. Maintaining digital, audit-ready accounts is the most effective way to overcome this barrier and access financing on competitive terms.

What is the best way to reduce late payments for Finnish SMEs?

Automated invoice reminders sent at 7, 14, and 30 days after invoice issue are the most direct tool for reducing late payments. Shortening standard payment terms from 30 to 14 days compounds this effect and improves monthly cash flow without additional cost.