TL;DR:

- Finland's 2026 tax reforms increase personal deductions and expand tax-free employer benefits, requiring immediate documentation by entrepreneurs.

- Starting in 2027, the corporate income tax rate will decline to 18%, and loss carry-forward periods will extend to 25 years, encouraging long-term investments.

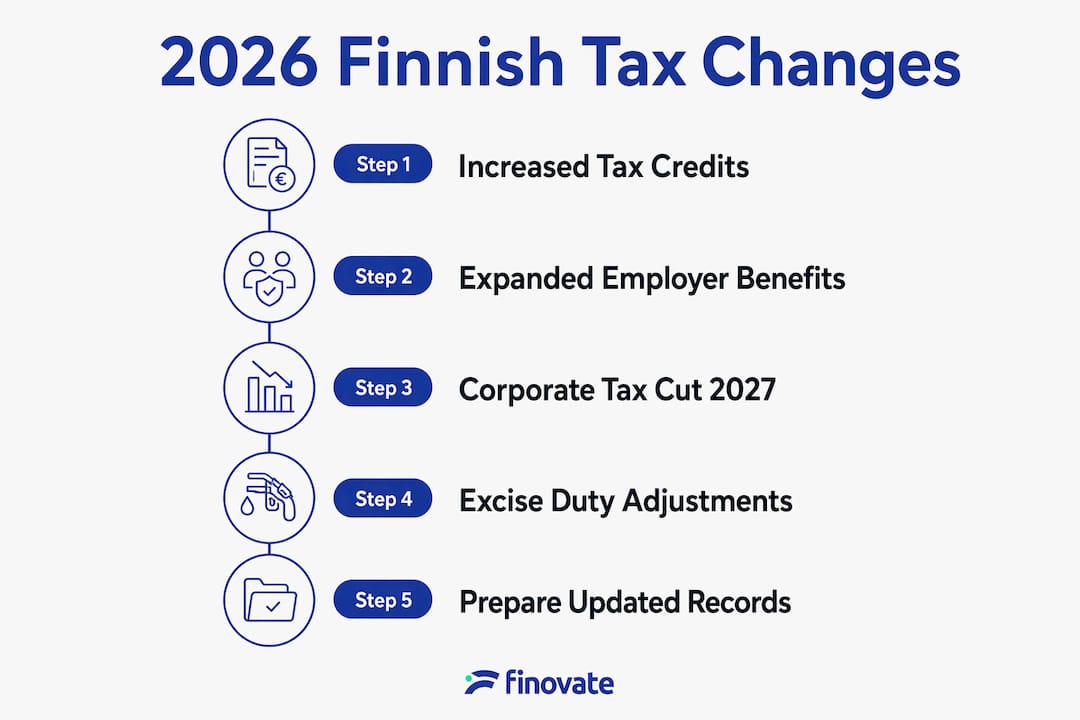

Finland's 2026 tax reforms introduce retroactive individual tax relief, a proposed cut to corporate income tax, and revised excise duties that directly affect how entrepreneurs plan, file, and manage their finances. The changes span personal deductions, employer benefits, and consumption taxes, with further reforms scheduled for 2027. For business owners, the window to act is already open. Understanding the new tax regulations in Finland for 2026 is not optional. It is the foundation of sound financial planning for the year ahead.

What are the main 2026 tax changes in Finland for individuals?

The household tax credit has been retroactively increased to EUR 2,100 from EUR 1,600, effective from 1 january 2026. That is a EUR 500 increase that applies to eligible household work such as cleaning, renovation, and care services. Entrepreneurs who use these services at home or at a business property should document every qualifying expense from the start of the year.

The deduction rates for labour costs have also risen. For work purchased from companies, the deduction percentage increases from 35% to 40%. For direct wages paid to workers, it rises from 13% to 15%. These higher rates reduce the net cost of hiring help, which matters directly to sole traders and small business owners managing their own properties.

Key individual tax relief changes for 2026 include:

- Household tax credit raised from EUR 1,600 to EUR 2,100 per person

- Labour cost deduction for company-purchased services increased from 35% to 40%

- Direct wage deduction increased from 13% to 15%

- Employer-provided benefits tax-free limit raised from EUR 400 to EUR 540, now covering fishing and hunting activities alongside sports and cultural events

- Tax card updates required to receive monthly benefit rather than waiting for a 2027 refund

The expansion of tax-free employer benefits is worth noting for any entrepreneur with staff. The new EUR 540 limit covers fishing licences and sports equipment rental, giving employers a wider range of perks to offer without triggering payroll tax obligations.

Pro Tip: Request an updated tax card from Vero.fi now. Without it, you will not see the benefit of the increased credits in your monthly withholding. You would have to wait until the 2027 tax assessment to receive any refund.

How will corporate taxation change from 2027 onwards?

The Finnish government has proposed reducing the corporate income tax rate from 20% to 18%, starting with the 2027 tax year. That two-percentage-point reduction is significant for any company with consistent taxable profits. A business earning EUR 500,000 in taxable income would pay EUR 10,000 less in tax annually under the new rate.

The proposed extension of the business loss carry-forward period is equally significant. Losses confirmed from 2026 onwards can now be carried forward for 25 years instead of 10. This change directly benefits capital-intensive sectors such as manufacturing, technology, and energy, where large upfront investments often generate losses in early years.

The extended loss carry-forward period and the proposed corporate tax rate cut together represent the most business-friendly structural reforms Finland has introduced in over a decade. For growth companies and capital-intensive businesses, the combination of lower rates and longer loss utilisation windows creates a materially stronger case for investing in Finland.

Strategic implications for business owners include:

- Tax planning horizon: You can now model losses over a 25-year window, which changes how you structure investment decisions

- Capital-intensive sectors: Manufacturing, renewable energy, and infrastructure businesses gain the most from the extended carry-forward

- International competitiveness: A rate of 18% brings Finland closer to the European average, making the country more attractive to foreign investors

- Loss utilisation: Only losses from business activities confirmed in 2026 or later qualify. Agricultural and individual losses remain on the 10-year limit

- Timing of investments: Entrepreneurs planning major capital expenditure should consider accelerating those decisions into 2026 to ensure losses fall within the new carry-forward window

The distinction between qualifying and non-qualifying losses is critical. Agricultural losses and losses attributed to individual taxpayers rather than corporate entities remain subject to the original 10-year limit. If your business spans multiple categories, you need to track losses separately by source.

For practical guidance on structuring your business taxes around these changes, the 2026 tax optimisation guide for Finnish SMEs covers the key planning strategies in detail.

What are the 2026 excise duty changes affecting businesses?

Finland's government is deliberately shifting the tax burden from earned income towards consumption taxes and excise duties. This is a structural policy choice, not a one-off adjustment. Entrepreneurs in retail, hospitality, and distribution need to factor ongoing excise duty increases into their pricing models.

The 2026 excise duty changes break down as follows:

| Product category | Change | Detail |

|---|---|---|

| Alcoholic beverages (over 2.8% ABV) | +9% | Applies to fermented products; affects hospitality and retail |

| Electronic cigarette liquids and nicotine pouches | +37% | Significant cost increase for specialist retailers |

| Gasoline | Small decrease | Average reduction of 2.7 cents per litre |

| Diesel | Small decrease | Average reduction of 2.4 cents per litre |

The fuel reductions are modest but real. A business running a fleet of vehicles will see a small improvement in operating costs. The alcohol and tobacco increases, however, are substantial. A 9% rise in alcohol excise duties and a 37% rise for e-cigarette liquids will push up wholesale costs for any business in those categories.

The government has also signalled that regular index-based adjustments to tobacco and alcohol duties are planned going forward. This means businesses in these sectors should build annual duty increases into their long-term pricing assumptions rather than treating each rise as an exception.

Pro Tip: If your business sells alcohol or tobacco products, review your supplier contracts now. Some contracts allow for price renegotiation when excise duties change. Locking in favourable terms before the next index adjustment could protect your margins.

For a full breakdown of how these duties interact with your VAT obligations, the tax compliance essentials guide covers the reporting requirements in practical terms.

Which legislative reforms after 2026 should entrepreneurs prepare for?

Several significant changes take effect from 2027, and preparation should begin now. These reforms affect business structure, payroll planning, and talent retention in ways that require advance action.

-

Permanent establishment taxation aligned with OECD standards. Finland is adopting the OECD's Authorised OECD Approach for taxing permanent establishments from 2027. Internal transactions between Finnish branches and foreign head offices will be recognised as taxable income or deductible expenses based on arm's length principles. Businesses with international structures must review how they document and price intra-company dealings.

-

Employee stock option taxation deferred until share disposal. From 2027, employees of unlisted companies will not pay tax on stock options until the shares are sold. No interest is charged on the deferred tax during the delay period. This is a material improvement for startups and growth companies using equity as a recruitment tool, as it removes the immediate cash burden on employees who receive options.

-

Entrepreneur deduction increased to 5.5%. The entrepreneur deduction, which reduces the taxable income of business owners operating through certain structures, rises to 5.5%. This directly lowers the effective tax rate for qualifying entrepreneurs and supports growth-stage companies.

-

Intra-company transaction documentation. Businesses operating international permanent establishments must adapt their compliance processes to treat internal corporate transactions as taxable income or deductible expenses according to OECD arm's length standards. This requires updated transfer pricing documentation and potentially new internal accounting procedures.

-

Payroll planning for stock option schemes. The deferral of stock option taxation changes the timing of payroll tax obligations. HR and finance teams need to update their payroll models to reflect when tax events actually occur under the new rules.

The stock option deferral is particularly relevant for Finnish technology companies and startups competing for talent against international employers. Removing the immediate tax liability on options makes equity compensation far more attractive to prospective employees. For entrepreneurs building teams in competitive sectors, this reform is worth communicating clearly during recruitment.

For a step-by-step overview of how these changes affect your filing obligations, the tax filing guide for Finnish entrepreneurs covers the practical process in full.

Key takeaways

The 2026 Finnish tax reforms deliver meaningful individual relief now, with corporate rate reductions and structural reforms arriving in 2027, requiring entrepreneurs to act on documentation and planning immediately.

| Point | Details |

|---|---|

| Household tax credit increase | Claim up to EUR 2,100 by keeping records of all eligible household work from 1 january 2026. |

| Update your tax card | Request a revised tax card from Vero.fi to receive monthly benefit rather than a delayed refund. |

| Corporate rate cut from 2027 | The proposed 18% rate and 25-year loss carry-forward apply from the 2027 tax year onwards. |

| Excise duty impact | Alcohol duties rose 9% and e-cigarette duties 37%; build ongoing index increases into pricing. |

| Stock option deferral | From 2027, employees pay tax on options only when shares are sold, improving startup talent retention. |

My view on navigating these reforms as an entrepreneur

The volume of changes arriving across 2026 and 2027 is genuinely significant. What concerns me most is not the complexity of any single reform. It is the retroactive nature of the 2026 individual tax relief. Retroactive legislation sounds like good news, and in this case it largely is. But it creates a documentation trap that many entrepreneurs will fall into.

The increased credits and deductions apply from 1 january 2026, but the legislation was confirmed later in the year. That means some business owners will have spent the first months of 2026 without keeping the records they now need to claim those benefits. If you have not been tracking eligible household and commuting expenses since january, start now and recover what you can.

On the corporate side, the proposed rate cut to 18% and the 25-year loss carry-forward are genuinely positive signals. Tax experts advise entrepreneurs to monitor upcoming amendments closely and update accounting practices promptly to fully leverage reliefs. The entrepreneurs who benefit most from these changes will be those who plan their investment timing and loss recognition deliberately, not those who simply wait and see what their accountant finds at year-end.

The excise duty shifts are the least visible but potentially the most persistent change for businesses in retail, hospitality, and distribution. A 9% alcohol duty increase and a 37% rise on e-cigarette products are not small adjustments. If your margins are tight, these changes require a pricing review now, not at the next annual budget cycle.

— Busayo

How Finovate can support your business through these changes

The 2026 and 2027 tax reforms require more than awareness. They require updated records, revised tax cards, and forward-looking financial planning that accounts for new rates and deduction rules.

Finovate provides monthly invoicing and tax services designed for Finnish entrepreneurs, covering everything from household credit claims to corporate tax planning under the new rules. Whether you need support managing excise duty impacts on your cost base or guidance on structuring your business ahead of the 2027 corporate rate change, Finovate's team works with you directly. Visit finovate.fi to speak with an adviser who understands the Finnish tax system and can help you act before the deadlines matter.

FAQ

What is the new household tax credit limit for 2026?

The maximum household tax credit for 2026 is EUR 2,100, increased retroactively from EUR 1,600 effective 1 january 2026. You must keep records of all eligible expenses from the start of the year to claim the full amount.

When does the proposed corporate tax rate cut take effect?

The proposed reduction from 20% to 18% applies from the 2027 tax year, not 2026. Entrepreneurs should plan now but will not see the lower rate in their 2026 tax assessment.

How does the extended loss carry-forward period work?

Business losses confirmed from 2026 onwards can be carried forward for 25 years instead of 10. Agricultural and individual losses remain on the original 10-year limit.

Will excise duty increases affect my business costs in 2026?

Alcohol excise duties rose by approximately 9% for products over 2.8% ABV, and duties on e-cigarette liquids and nicotine pouches increased by 37%. Fuel duties decreased slightly, with gasoline falling by around 2.7 cents per litre.

What should I do now to prepare for the 2027 stock option tax change?

From 2027, employees of unlisted companies will defer tax on stock options until the shares are disposed of. Update your payroll models and communicate the change to employees who hold or are being offered equity as part of their remuneration.